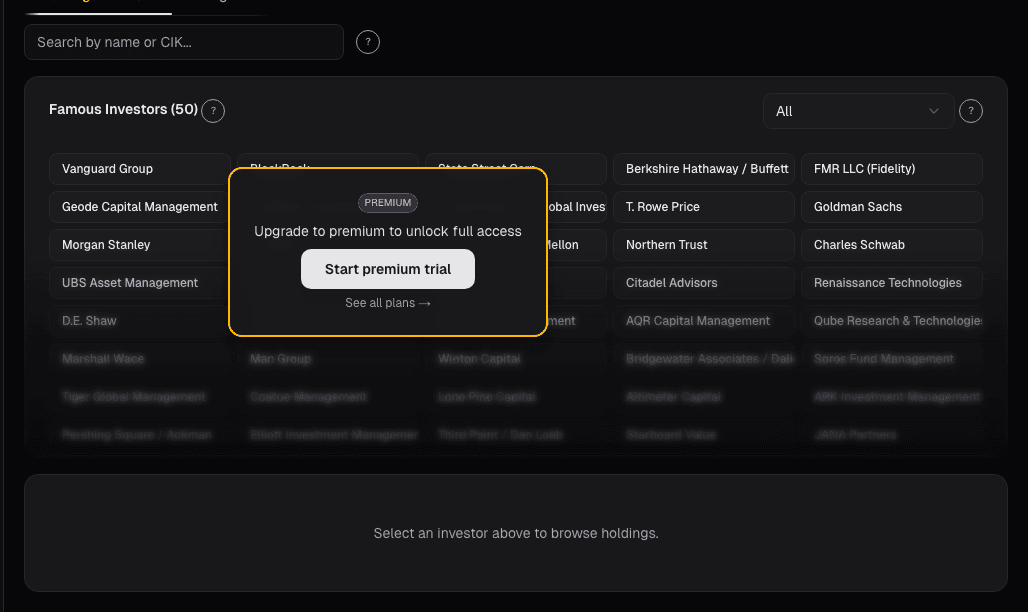

Investor Holdings

Studying a single manager's full book is pedagogy for portfolio construction. Concentration, position sizing, sector expression, how convictions survive…

Marcus Chen7 min read

Marcus Chen7 min readFive years ago I started a habit of reading one concentrated fund's 13F end-to-end each month, and I still do it. Not cherry-picking the interesting names, not scanning for the ticker I already own, reading the full book the way you'd read a portfolio you were inheriting. The first month I did this was Appaloosa's: 42 positions, top 10 about 55% of AUM, heavy cyclicals-and-financials tilt, and a set of "survivor" positions that had been in the book for 10+ quarters. What I learned wasn't which names to buy, it was how a concentrated long/short manager actually builds conviction. The survivors weren't there because they were "good companies" in the abstract; they were there because the thesis had been validated across multiple earnings cycles. The new positions were almost all sized conservatively at first and only grown to conviction size after 2-4 quarters of confirmation. The exits were swift and complete, not gradual trims. That's a style guide for portfolio construction, and reading it directly from the 13F was more educational than any book on position sizing I'd read. The Investor Holdings card is built for exactly that investor-first view: pull up any 13F filer, see their whole book, study how they express views.

This post is about the Investor Holdings card, why investor-first reading is under-rated compared to ticker-first scans, and the three reads that turn a single fund's book into a lesson in portfolio construction.

TL;DR

- Investor-first reading teaches portfolio construction; ticker-first reading chases signals.

- Concentration ratio (top-10 / AUM) reveals style. Under 20% = diversified; 30-50% = concentrated; 70%+ = single-bet shop.

- Conviction positions (>3% of AUM, held 4+ quarters) are where the thesis lives. Experimental trades are noise.

- New 2%+ day-one positions are high-signal. Someone did the work before committing.

- Exits of former convictions are cheap research prompts. Something changed; figure out what.

Why investor-first reading is different

Most 13F consumption is ticker-first: "who bought NVDA this quarter?" That surfaces any fund that owns the name and asks whether their ownership is bullish signal. It's a useful question for a single-name decision but a bad question for learning how portfolios are actually built.

Investor-first reading inverts the direction. Instead of asking "who owns this?" you ask "what does Baupost's entire book look like today?", and then you read the whole thing. Every position, every weight, every quarter-over-quarter change. You're not fishing for a trade; you're studying portfolio construction as practiced by someone whose money is in the game.

What this teaches:

- How diversified to be: a manager with 40 positions is expressing a different conviction level than one with 12

- When to concentrate: survivors (multi-quarter conviction positions) show you which kinds of theses justify size

- How to express a sector view: through multiple names or one concentrated bet, small weights or large

- How to use options: some concentrated managers use options as primary exposure; others only for hedging

- How to exit: all-at-once vs. gradual trim; what usually precedes a full exit

Tepper's book reads very differently from Baupost's, and Baupost's reads differently from Pershing Square's. The contrast is the lesson.

What the Investor Holdings card shows

The Investor Holdings card lists every position in a filer's most recent 13F:

- Position size: shares and market value

- % of reported AUM: the position's weight in the book

- QoQ change: new / add / trim / exit, with magnitude

- Sector for each position

- Cost basis estimate: blended average of transaction ranges since initial purchase (where available)

- Sector-weight donut: the book's sector distribution at a glance

- Top-10 concentration bar: fast read on diversification level

- Conviction filter: positions sized > 3% of AUM held for 4+ quarters

- New-position filter: positions initiated this quarter at > 2% weight

- Exit filter: former holdings fully sold this quarter

Three reads that translate books into lessons

Top-10 / AUM concentration reveals style. Under 20% is a highly diversified manager, typically long-short funds with dozens of names, each sized to hedge portfolio risk rather than to express conviction. 30-50% is a concentrated long-biased book, Appaloosa, Baupost, Third Point, where position size correlates with thesis confidence. 70%+ is a single-bet shop, Pershing Square, Scion, where one or two names drive most returns. Match your study to managers whose style matches the one you're trying to practice; learning concentration from a diversifier is confusing, and vice versa.

New positions sized > 2% on day one = high-signal conviction. Most new positions in concentrated books are starter sizes, 0.5-1.5% of AUM, that may or may not grow. A new position that lands at > 2% in the filing quarter is a manager saying "I've done the work, I'm confident enough to size into the thesis immediately." These positions are often the most studyable because they represent a fully-formed view. Watch what happens to them over the next 1-2 quarters; if they grow, the thesis is validating; if they shrink, something in the work didn't hold up.

Exits of former convictions = cheap research prompts. When a name that was top-10 for 8 quarters leaves the book entirely, something changed. Either the thesis played out (good outcome, time to move on) or the thesis broke (bad outcome, exit while you can). Either way, reading the exit is research: pull up the name, read what happened operationally in the last 2-4 quarters, see what the fund likely saw. This is one of the most consistent ways I've found to generate "new name to study" ideas.

Example: two contrasting books

Read as a comparative study:

| Dimension | Fund A (concentrated value) | Fund B (long-short multi-strat) |

|---|---|---|

| Total positions | 28 | 180 |

| Top-10 concentration | 58% of AUM | 19% of AUM |

| Average position weight | 3.5% | 0.55% |

| Largest single position | 12% of AUM | 1.9% of AUM |

| Conviction holdings (4+ quarters, > 3%) | 9 | 2 |

| New positions at > 2% | 2 | 0 |

| Full exits this quarter | 3 | 44 |

Fund A is expressing views, every position is sized deliberately; exits are rare and meaningful. Fund B is running a process, positions are small, turnover is high, concentration is deliberately low. Studying Fund A teaches you how to size a conviction; studying Fund B teaches you how to run diversified exposure. Neither is better; they're different styles for different goals.

What the card can miss

- Shorts and derivatives. 13Fs show longs; the rest of the book is invisible.

- Non-US and private holdings. International listings and private-equity exposures aren't in 13F.

- Cost basis estimates. Blended averages may not reflect actual purchase prices accurately.

- Style-drift reporting. Some funds change style between filings; older quarters may not represent current approach.

- Confidential treatment. Certain positions can be delayed from disclosure.

Common mistakes

- Cherry-picking names from a book. Reading only the famous names misses the portfolio-construction lesson.

- Copying positions without understanding style. A 4%-of-AUM position for a concentrated fund sizes differently than for a diversified one.

- Chasing exits as sell signals. Some exits are thesis-complete, not thesis-broken; read the why.

- Treating quarterly data as timely. 45-day lag means the book you're studying is already old.

- Studying managers whose style doesn't match yours. Concentrated managers teach concentration; diversifiers teach diversification.

Where it fits

Pair with Investor Diff for the quarter-over-quarter change view across filers, with Institutional Holders for the per-ticker cross-filer read, and with source filings at the SEC's EDGAR for raw disclosure documents.

FAQ

How fresh is the data?

Updated within 24 hours of each new 13F filing. The filing deadline is 45 days after quarter-end, so Q1 positions are fully visible mid-May.

Can I compare a fund's book over time?

Yes, the trailing-quarters view shows each position's weight history over 4-8 quarters.

What's the minimum AUM for inclusion?

All 13F filers with > $100M in reportable US equity AUM are included (that's the SEC threshold for filing).

Are fund-of-funds filings useful?

Less so, the holdings are typically other funds, not underlying stocks. The card flags these.

Can I see activist positions separately?

Yes, activist filings (13D/13G for > 5% ownership) are cross-referenced with the 13F data where applicable.

Related reading

Open the Investor Holdings card → /app/investors

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

How to Read 13F Filings Without Falling Asleep

A plain-language guide to understanding 13F filings, what they reveal about institutional investors, and how to use Alphactor's 13F explorer to spot…

13F Holders: Who Owns This Stock

Raw ownership is already in the price. What isn't is portfolio-weight change, when a concentrated fund lifts a position from 1% to 4% of its book, that's a…

Investor Diff: Turning Quarterly 13Fs Into Signal

A 13F snapshot is a photograph; the diff is the motion picture. Knowing what Klarman or Marks held last quarter is weakly useful, knowing what they added…

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free