Correlation: The Number Behind Real Diversification

How correlation coefficients reveal whether your portfolio is truly diversified or just a collection of stocks that move in lockstep.

Marcus Chen4 min read

Marcus Chen4 min readThe Diversification Illusion

Most investors think diversification means owning lots of different stocks. It does not. You can hold 30 positions and still have a portfolio that behaves like a single bet. The difference between real diversification and the illusion of it comes down to one number: correlation.

Correlation measures how two assets move relative to each other, on a scale from -1 to +1. A correlation of +1 means they move in perfect lockstep. A correlation of -1 means they move in exactly opposite directions. A correlation of 0 means their movements are unrelated.

Think of it like passengers on a bus. If everyone leans the same direction in every turn, the bus tips over. If passengers lean in different directions, the bus stays balanced. Your portfolio works the same way.

What the Numbers Actually Mean

In practice, you will rarely see correlations at the extremes. Here is what real-world ranges look like:

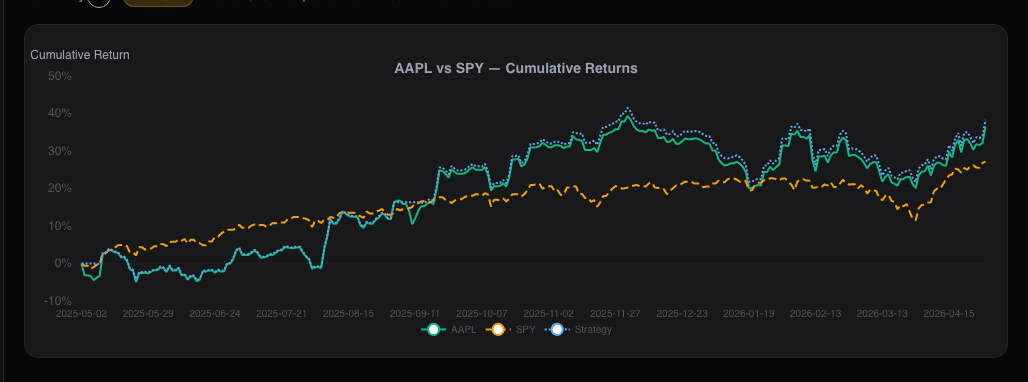

+0.7 to +1.0: Highly correlated. These positions move together. Holding Apple and Microsoft gives you two names but one bet on big-cap tech. During the 2022 sell-off, mega-cap tech stocks declined as a group because they share the same sensitivity to interest rates and growth expectations.

+0.3 to +0.7: Moderately correlated. Some overlap, but meaningful independent movement. A bank stock and a consumer staples stock might land here. They both respond to the broad economy, but their specific drivers differ enough to provide partial diversification.

-0.3 to +0.3: Low correlation. This is the sweet spot for diversification. Energy stocks and long-duration Treasury bonds historically land in this range. When one zigs, the other does not necessarily zag, but it is doing its own thing.

-1.0 to -0.3: Negatively correlated. Rare in equity portfolios but powerful when found. Gold and the U.S. dollar often exhibit moderate negative correlation. Adding a small allocation of negatively correlated assets can reduce portfolio volatility more than removing your worst-performing stock.

Why Correlations Break When You Need Them Most

Here is the uncomfortable truth: correlations are not stable. They shift over time, and they tend to spike during market stress. The phenomenon is called "correlation convergence," and it is one of the most important dynamics in portfolio management.

During the calm markets of 2017, the average pairwise correlation among S&P 500 stocks was around 0.25. During the March 2020 crash, it jumped above 0.70. Assets that looked diversified in normal times suddenly moved in unison.

This has a direct implication for portfolio construction. If you build a portfolio assuming correlations stay at their five-year average, you are underestimating the risk of simultaneous losses across your holdings. The portfolio that looks like it has a 12% maximum drawdown on paper might experience 20% when correlations spike.

Building a Correlation-Aware Portfolio

Start by measuring what you actually own. Pull the trailing 12-month correlation matrix for your holdings. If your average pairwise correlation is above 0.50, you have a concentration problem regardless of how many positions you hold.

Step 1: Identify your clusters. Group holdings that have correlations above 0.60. You will likely find clusters around themes: rate-sensitive stocks, commodity-linked names, high-beta growth. Treat each cluster as a single effective position for sizing purposes.

Step 2: Set a correlation budget. A reasonable target for a 15-20 stock equity portfolio is an average pairwise correlation between 0.25 and 0.40. Below 0.25 is difficult to achieve in an all-equity portfolio. Above 0.40 means your diversification is doing less work than it should.

Step 3: Add structural diversifiers. If your equity holdings are inherently correlated (most are), consider assets outside the equity universe. Treasury bonds, commodity ETFs, and REITs have historically provided lower correlation to broad equities, though each comes with its own risk profile.

Step 4: Stress-test under adverse conditions. Alphactor's portfolio dashboard simulation tools let you model how your portfolio behaves when correlations increase. Running a stress test with correlations shifted 0.2 higher across the board reveals the portfolio's behavior in a crisis, when diversification matters most.

A Practical Example

Consider a portfolio with these five holdings, each at 20%: NVIDIA, AMD, Microsoft, Salesforce, and ServiceNow. Sector-diverse? Not really. These are all technology or technology-adjacent names with high sensitivity to interest rates and growth expectations. The average pairwise correlation is likely above 0.65.

Now swap AMD and ServiceNow for Johnson & Johnson and Exxon Mobil. The average pairwise correlation drops meaningfully, perhaps to 0.35. The expected return may be similar, but the range of outcomes narrows. You sleep better during drawdowns, and sleeping better means you stick with your plan.

The Takeaway

Diversification is not a count of positions. It is a measure of how independently those positions behave. A 10-stock portfolio with low average correlation can be more diversified than a 30-stock portfolio where everything moves together. Check the number, either manually or through Alphactor's stock comparison tool. It is the difference between a portfolio that bends under pressure and one that breaks.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Choosing the Right Benchmark (Hint

Why benchmarking against the wrong index distorts your performance assessment and how to select a benchmark that matches your actual portfolio.

Concentrated vs Diversified: The Portfolio Sizing Debate

The tradeoffs between concentrated and diversified portfolios, with practical guidance on how many stocks you actually need.

Alt-Data Sentiment at the Portfolio Level

Per-ticker alt-data breaks down past 10 positions. A roll-up of WSB, news, MSPR, and options lets a 90-second scan replace 100 minutes of manual checking.

Portfolio Attribution: Where Your Returns Actually Come From

Beating the benchmark by 400bps feels good until attribution tells you it was all allocation luck on one sector call. Selection vs. allocation vs.

Portfolio Audit Trail: Every Decision

Regulated managers need an audit trail. The Audit Trail card on alphactor.ai records every trade, rebalance, alert, and note into one timestamped log you…

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free