Choosing the Right Benchmark (Hint

Why benchmarking against the wrong index distorts your performance assessment and how to select a benchmark that matches your actual portfolio.

Marcus Chen4 min read

Marcus Chen4 min readThe Benchmark Trap

Every investor compares their returns to something. For most retail investors, that something is the S&P 500. It is the number on the evening news, the line on every brokerage homepage, and the default answer to "how did the market do?"

The problem is that the S&P 500 is a very specific bet: 500 large-cap U.S. companies, market-cap weighted, with roughly 35% in technology and communication services. If your portfolio holds small caps, international stocks, or any fixed income, comparing yourself to the S&P 500 is like comparing your commuter sedan to a sports car and concluding you are a bad driver.

A wrong benchmark changes your behavior. Investors who trail the S&P 500 because they hold a diversified portfolio often abandon their strategy and pile into large-cap tech to "keep up," arriving just in time for the next rotation.

What Makes a Good Benchmark

A valid benchmark has three properties.

Investable. You could actually hold it. A theoretical index that cannot be replicated with real securities is useless for comparison. The S&P 500 is investable (via SPY or VOO). A custom index you build to flatter your returns is not.

Representative. It reflects the asset classes, geographies, and risk profile of your actual portfolio. If you hold 20% international stocks, your benchmark should include international stocks. If you hold 30% small caps, a large-cap-only benchmark will mislead you.

Defined in advance. The benchmark must be set before you look at results. Choosing a benchmark after the fact, picking whichever index your portfolio happens to beat, is not benchmarking. It is rationalization.

Matching Benchmark to Portfolio

Here are benchmark suggestions based on common portfolio types.

U.S. large-cap focused (80%+ in S&P 500-type names): The S&P 500 (SPX) works. This is the one case where the default benchmark is appropriate. If you are trying to beat the large-cap market with large-cap stocks, measure yourself against it honestly.

U.S. all-cap (mix of large, mid, and small): Use the Russell 3000 or the total U.S. stock market index (VTI). The S&P 500 misses the small and mid-cap portion of your portfolio, which can diverge significantly from large caps over multi-year periods.

Global equity (U.S. and international): Use the MSCI ACWI (All Country World Index) or a blend of VTI and VXUS weighted to match your domestic/international split. From 2010 to 2020, the S&P 500 crushed international markets. An investor holding 30% international stocks would look like a failure against the S&P 500 but might be performing well against a global benchmark.

Balanced portfolio (stocks and bonds): Use a blended benchmark that matches your target allocation. For a 70/30 stock/bond portfolio, blend 70% S&P 500 with 30% Bloomberg Aggregate Bond Index. Comparing a 70/30 portfolio to an all-equity index during a bull market will always make you look bad, which defeats the purpose of benchmarking.

Value-tilted portfolio: Use the Russell 1000 Value or S&P 500 Value index. From 2017 to 2020, value dramatically underperformed growth. A value investor who benchmarked against the S&P 500 would have felt terrible. Benchmarked against a value index, they might have been in line or even ahead.

Blended Benchmarks in Practice

Most real portfolios do not match any single index. The solution is a blended benchmark. Here is an example.

Portfolio allocation: 50% U.S. large cap, 15% U.S. small cap, 15% international developed, 10% bonds, 10% cash.

Blended benchmark: 50% S&P 500 + 15% Russell 2000 + 15% MSCI EAFE + 10% Bloomberg Aggregate + 10% 3-month T-bills.

This benchmark has the same structural profile as your portfolio. When you outperform it, you can attribute the outperformance to your stock selection and timing, not to holding a different asset mix. When you underperform, you know the issue is your picks, not your allocation.

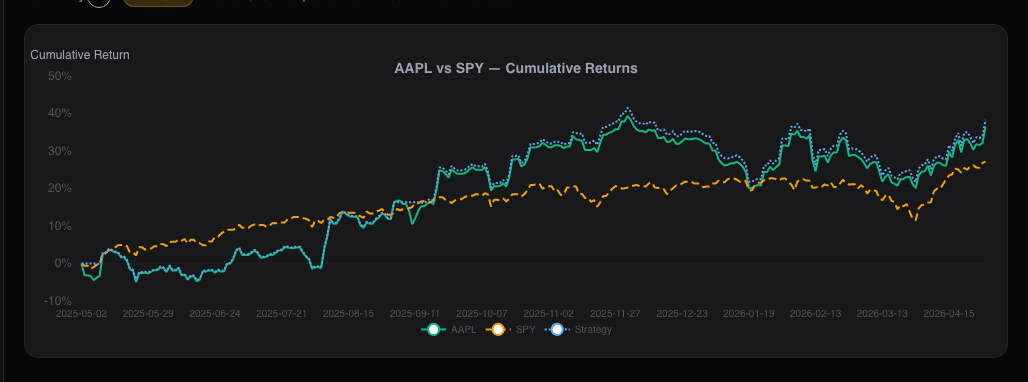

Alphactor's portfolio dashboard lets you define custom benchmarks against your portfolio, so your performance attribution reflects actual skill rather than structural differences between your holdings and a mismatched index.

The Attribution Question

Once you have the right benchmark, decompose your excess return (or shortfall) into two components.

Allocation effect: Did overweighting or underweighting sectors help or hurt? If you were overweight energy and energy outperformed, that is positive allocation effect.

Selection effect: Within each sector, did your specific picks beat the benchmark holdings? If your healthcare stocks outperformed the healthcare slice of your benchmark, that is positive selection.

This decomposition is the only way to know what you are good at. Many investors believe they are great stock pickers when they are really making one macro bet (like overweighting tech in the 2010s). A proper benchmark reveals the difference.

When You Should Change Your Benchmark

Change your benchmark when your portfolio strategy changes, not when your performance looks bad. If you shift from a U.S.-focused portfolio to a global one, update the benchmark. If you add a permanent fixed-income allocation, update the benchmark.

Do not change it because you underperformed. The entire purpose of a benchmark is to hold yourself accountable. If the accountability is uncomfortable, the answer is usually to improve your process, not to find an easier yardstick. You can also use Alphactor backtesting to test whether your strategy consistently outperforms the benchmark you have chosen.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Brinson Attribution: Did You Pick Good Stocks

Brinson-Fachler splits active return into allocation, selection, and interaction so you can tell whether outperformance came from sector bets or stock-picking.

Chart Benchmark: Relative Strength Is Where the Alpha Lives

Absolute price charts hide what's tradeable. Plotting a stock as a ratio against SPY, its sector, or a peer group reveals the idiosyncratic alpha that…

Concentrated vs Diversified: The Portfolio Sizing Debate

The tradeoffs between concentrated and diversified portfolios, with practical guidance on how many stocks you actually need.

Correlation: The Number Behind Real Diversification

How correlation coefficients reveal whether your portfolio is truly diversified or just a collection of stocks that move in lockstep.

How to Build Your First Portfolio: A Step-by-Step Guide

A practical walkthrough of creating and managing your first portfolio in Alphactor, from adding positions to tracking performance.

Monte Carlo Simulation

How Monte Carlo simulations model thousands of possible portfolio outcomes and why they are more useful than single-point forecasts.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free