Blog /

#portfolio

31 posts tagged portfolio.

31 posts

Alt-Data Sentiment at the Portfolio Level

Per-ticker alt-data breaks down past 10 positions. A roll-up of WSB, news, MSPR, and options lets a 90-second scan replace 100 minutes of manual checking.

Portfolio Attribution: Where Your Returns Actually Come From

Beating the benchmark by 400bps feels good until attribution tells you it was all allocation luck on one sector call. Selection vs. allocation vs.

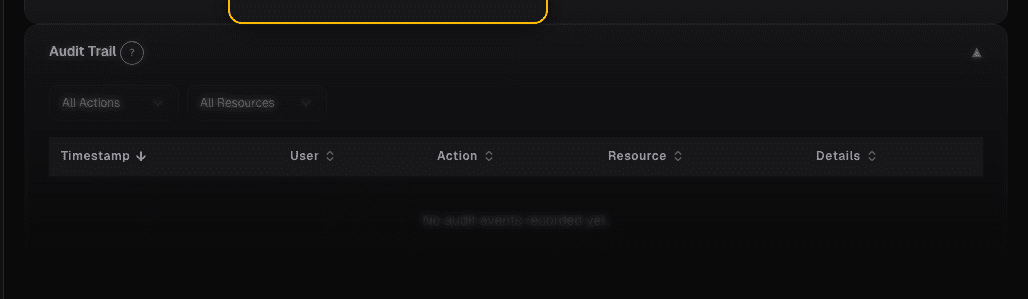

Portfolio Audit Trail: Every Decision

Regulated managers need an audit trail. The Audit Trail card on alphactor.ai records every trade, rebalance, alert, and note into one timestamped log you…

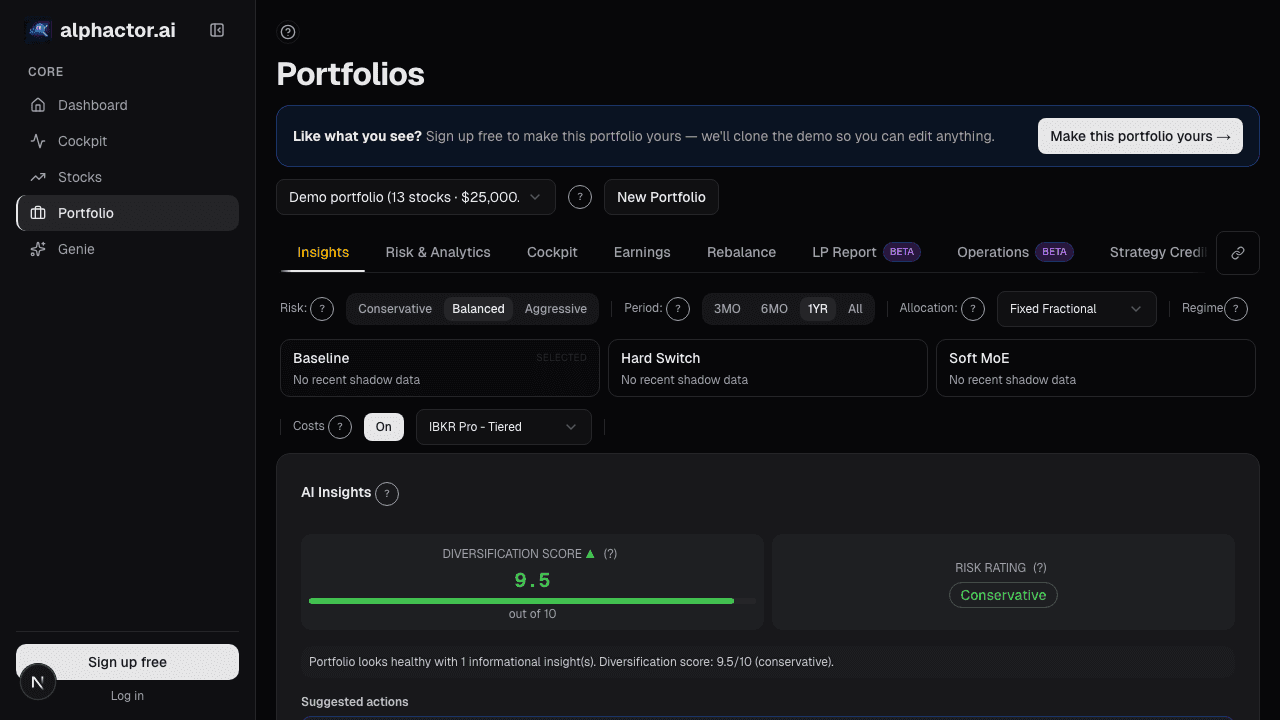

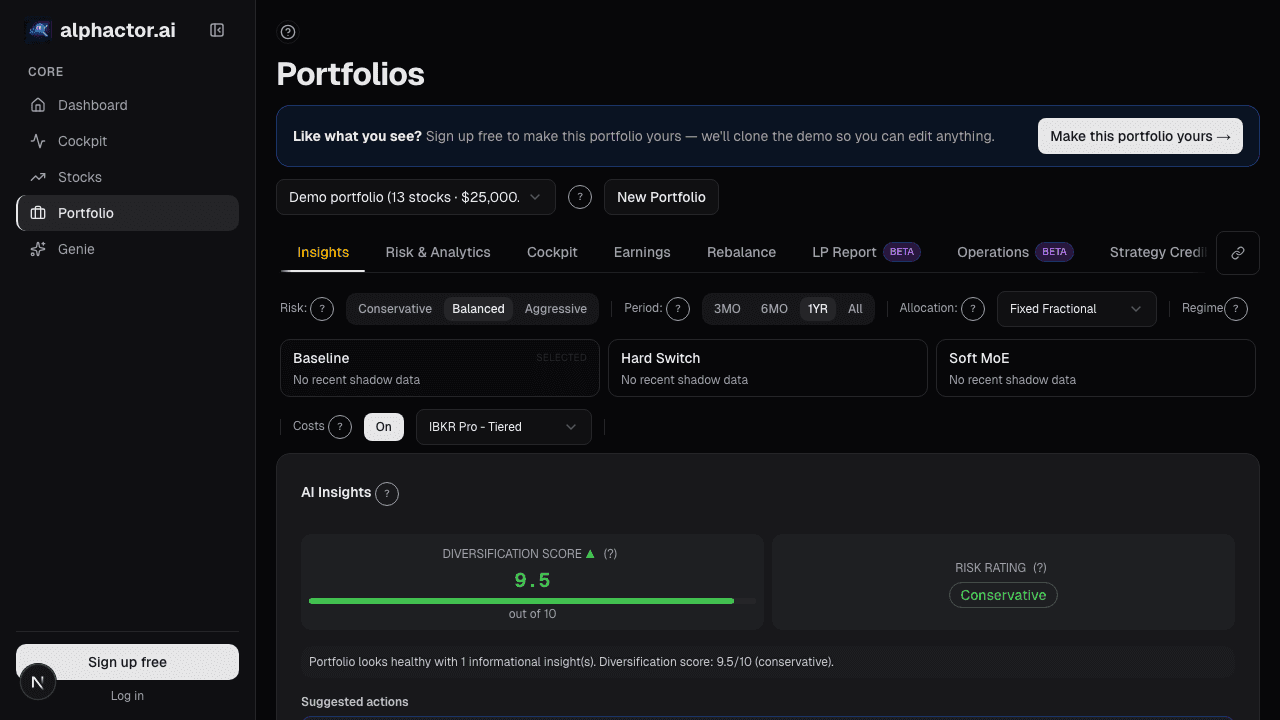

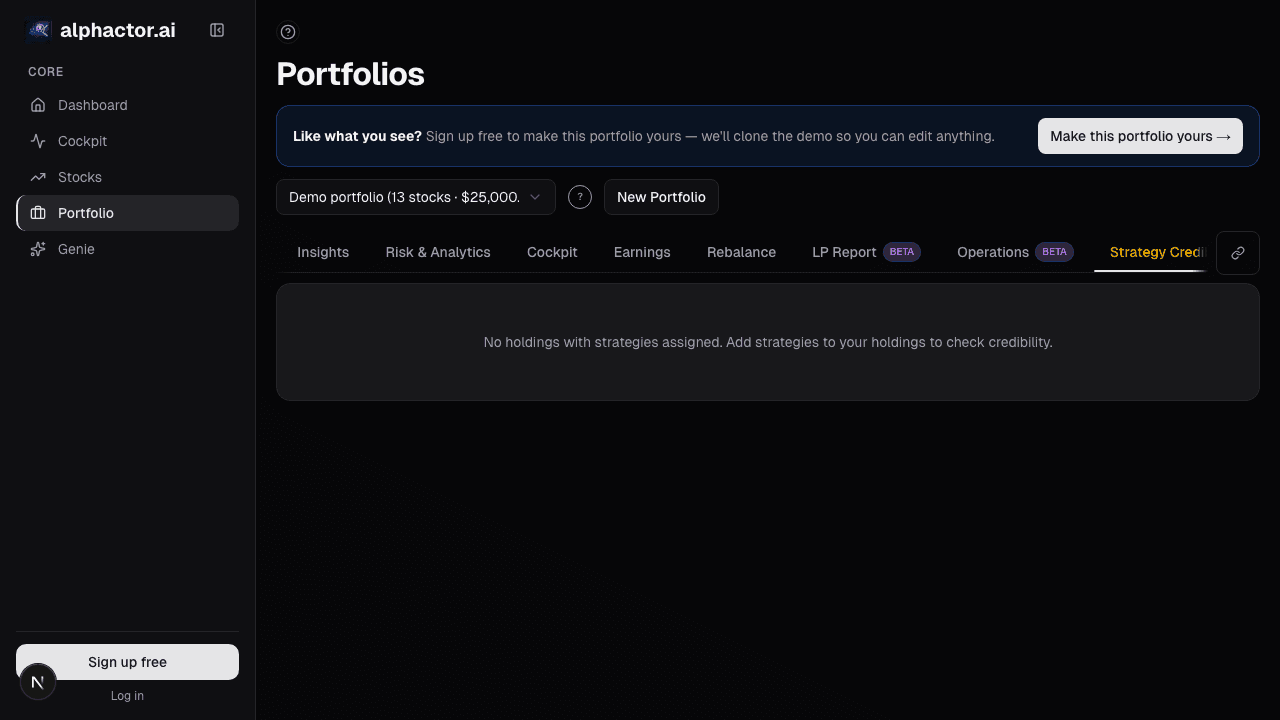

Portfolio Credibility

Conviction is self-reported; credibility is externally anchored. The two diverge exactly where mistakes live, an 8% position in a name you love with a…

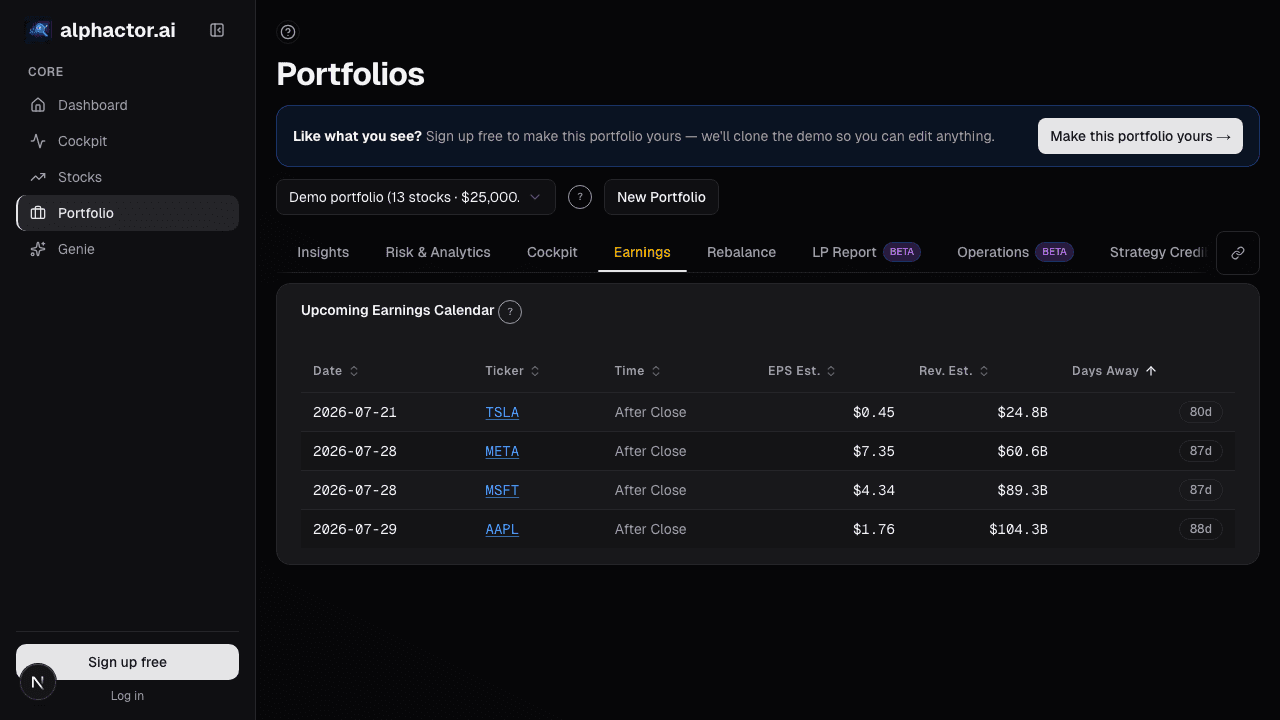

Portfolio Earnings: Calendar, Exposure

Earnings risk is about the whole book into the week, not each position. When 40% of NAV reports in one week, and 60% of that is in a single sector, you're…

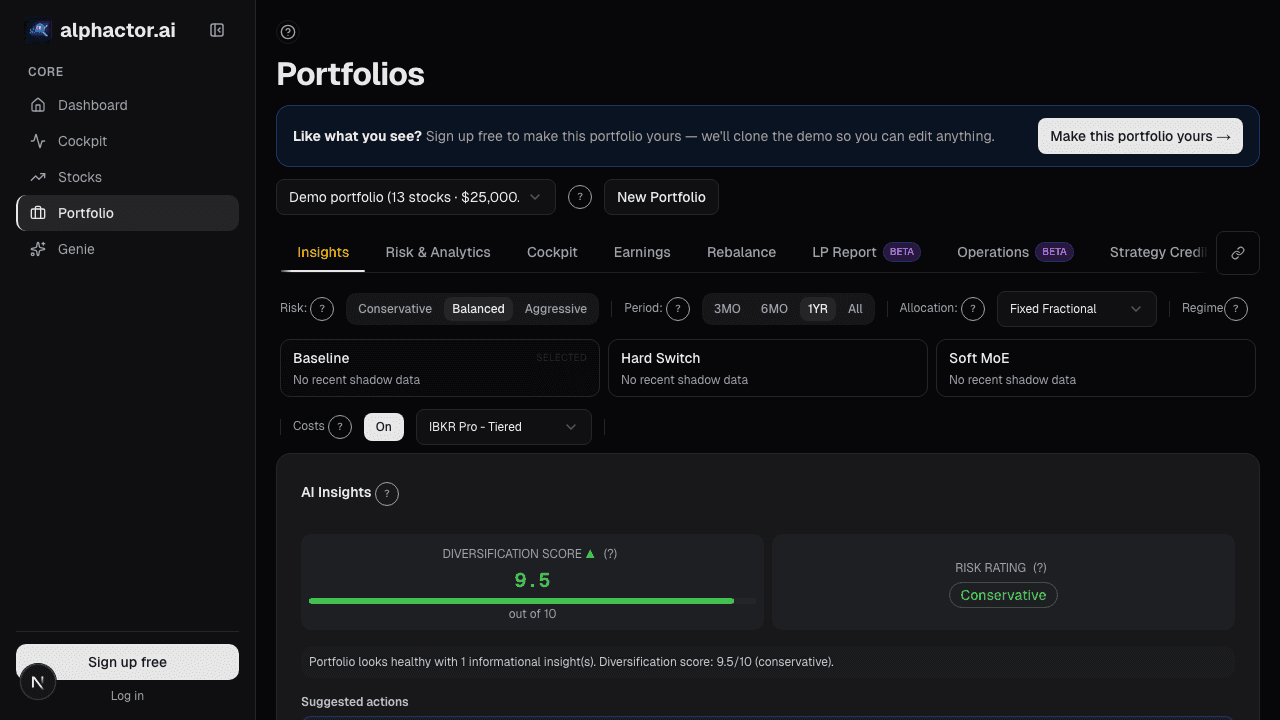

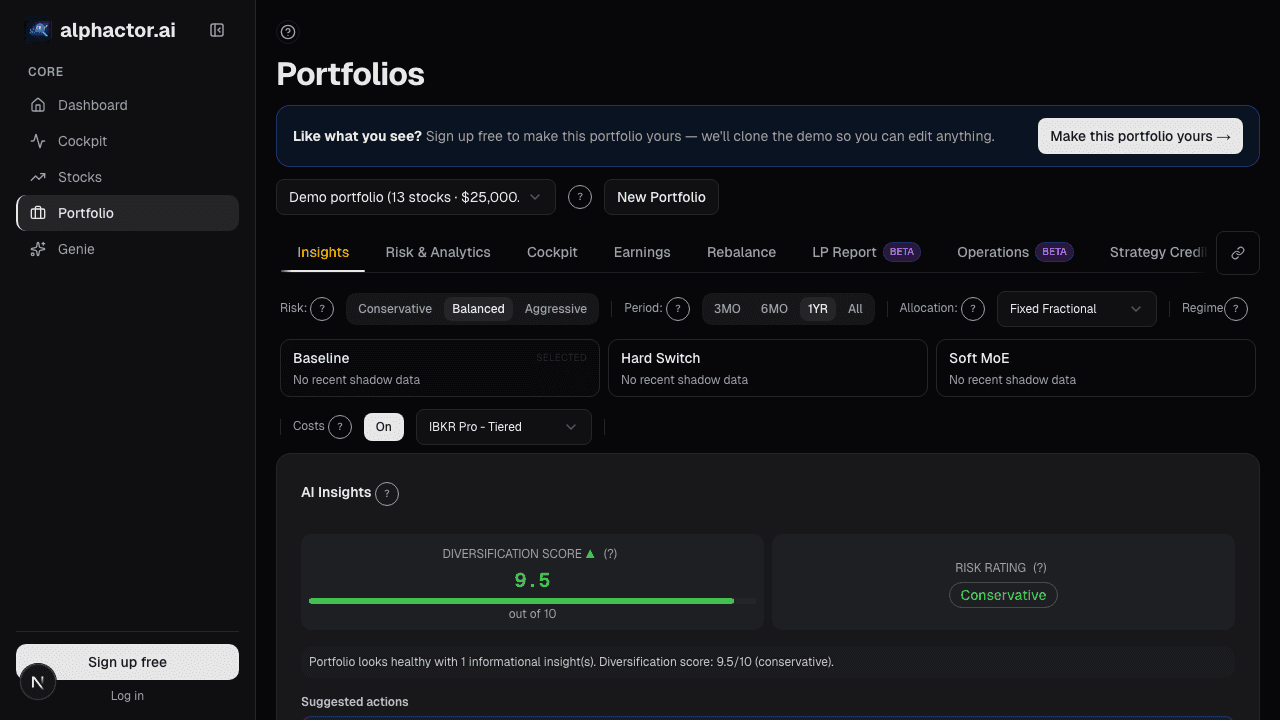

Factor Exposure

Factor exposures are bets whether or not you chose them. Decomposition surfaces unintentional tilts before a rotation exposes them as underperformance.

FX Exposure: The Currency Risk Hiding in Your USD Portfolio

You bought US stocks in dollars, so you have no FX risk, right? Wrong. US large-cap multinationals earn 40-60% of revenue abroad.

LP Report: Institutional-Grade Portfolio Summaries

Reporting is the tax on managing other people's money. A good LP report system takes a 12-hour manual job and turns it into a 90-minute review-and-polish…

Portfolio Optimizer: From Holdings to an Efficient Frontier

Naive mean-variance overweights recent winners. Running MVO, risk parity, and Black-Litterman in parallel shows which allocation choices are robust vs. fragile.

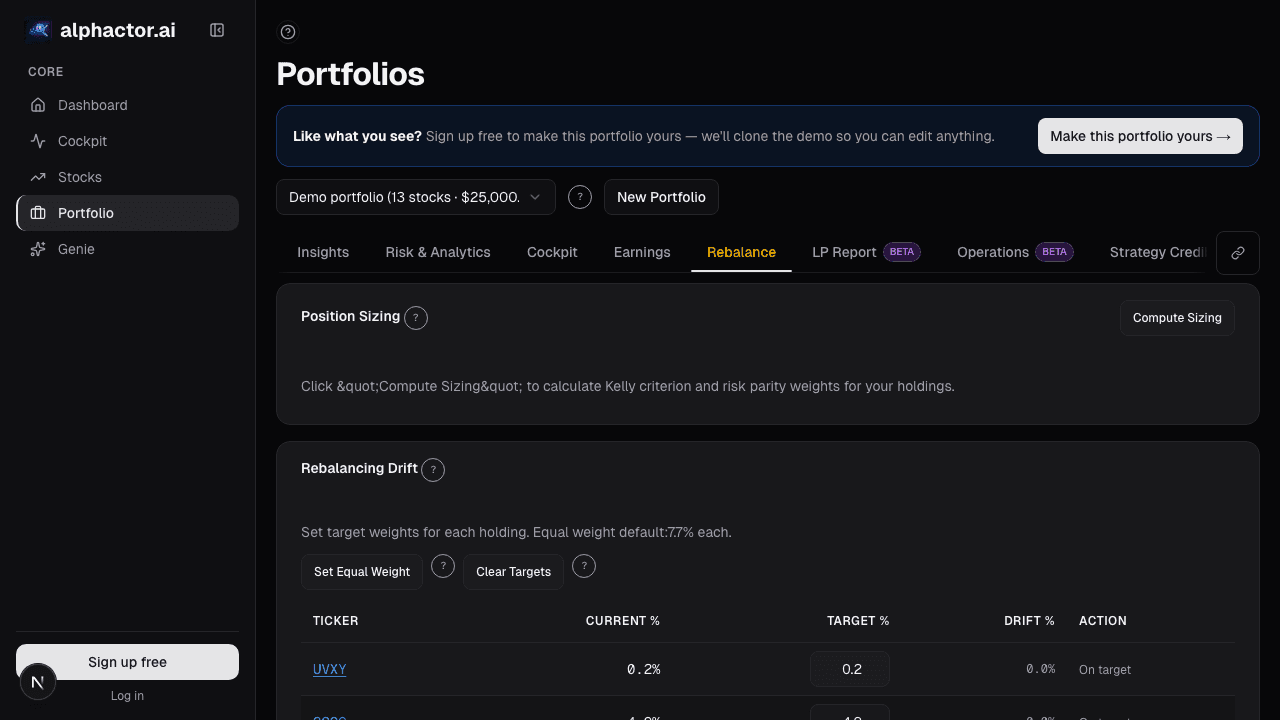

Portfolio Rebalance: Turning Drift Into Scheduled

Portfolios rebalanced on a schedule beat portfolios rebalanced 'when it feels right.' Feel-right under-rebalances winners, over-rebalances losers, and stops…

Transaction Cost Analysis

Implicit costs run 10-50 bps per trade; at 2x annual turnover that erodes 40-200 bps of alpha. Slippage breakdowns show which venue or size is responsible.

Brinson Attribution: Did You Pick Good Stocks

Brinson-Fachler splits active return into allocation, selection, and interaction so you can tell whether outperformance came from sector bets or stock-picking.