Part of: Risk Management

Portfolio Rebalance: Turning Drift Into Scheduled

Portfolios rebalanced on a schedule beat portfolios rebalanced 'when it feels right.' Feel-right under-rebalances winners, over-rebalances losers, and stops…

Marcus Chen7 min read

Marcus Chen7 min readI spent most of 2021 watching my own portfolio's risk profile drift quietly upward without doing anything about it. My target was 50% US equity, 20% international, 20% fixed income, 10% alts. By December the actual mix was 72% US equity, 14% international, 8% fixed income, 6% alts, because the US growth stocks had quietly doubled and I hadn't trimmed. The "balance" existed on paper; the actual portfolio was a tech-growth bet with vestigial diversification. When 2022 hit I took the full drawdown on that undisciplined mix; if I'd been rebalancing quarterly to the 50/20/20/10 target, I'd have trimmed into the 2021 rally and bought into the 2022 drawdown. The math would have produced roughly 4-5% of additional return over those two years. That's approximately 6 months of salary for me. The cost of the laziness was concrete; the fix was mechanical rebalancing, which I've done on a quarterly schedule ever since.

This post is about the Portfolio Rebalance card, the evidence on scheduled vs. discretionary rebalancing, and the three practices that keep the mechanics from creating their own problems (tax drag, transaction cost, earnings-week noise).

TL;DR

- Scheduled rebalancing beats discretionary. Discretionary under-rebalances winners, over-rebalances losers, and quits during drawdowns.

- Monthly with ±3% drift threshold is a reasonable default. Too often = churn; too rarely = risk drift.

- Tax-aware rebalancing in taxable accounts is non-negotiable. A 40% short-term gain on a 1% weight adjustment is a tax disaster.

- Don't rebalance during earnings weeks. Earnings drift dominates any ±3% weighting adjustment.

- Threshold-based is better than date-based in volatile markets. Trigger on drift, not calendar.

Why scheduled rebalancing beats discretionary

The evidence is unambiguous across decades of portfolio-management research: portfolios rebalanced on a schedule to a predefined target mix outperform portfolios rebalanced "when it feels right." The feel-right version has three specific failure modes:

- Under-rebalances winners. The winners feel good; trimming them feels like selling strength. So you don't, and risk creeps up.

- Over-rebalances losers. The losers feel bad; adding to them feels like averaging into a problem. Sometimes you do (with poor timing, at interim bottoms that aren't actually bottoms); sometimes you bail instead (locking in losses).

- Stops entirely during drawdowns. When rebalancing would add the most value, buying the assets that just fell, is exactly when emotional-rebalancing paralysis sets in.

A mechanical rule eliminates all three. Rebalance monthly to target, or whenever position drift exceeds ±3%, executed without emotion. Over a decade of market environments that simple discipline produces measurably better risk-adjusted returns than any discretionary variant, not because the math is sophisticated but because the mechanics don't flinch.

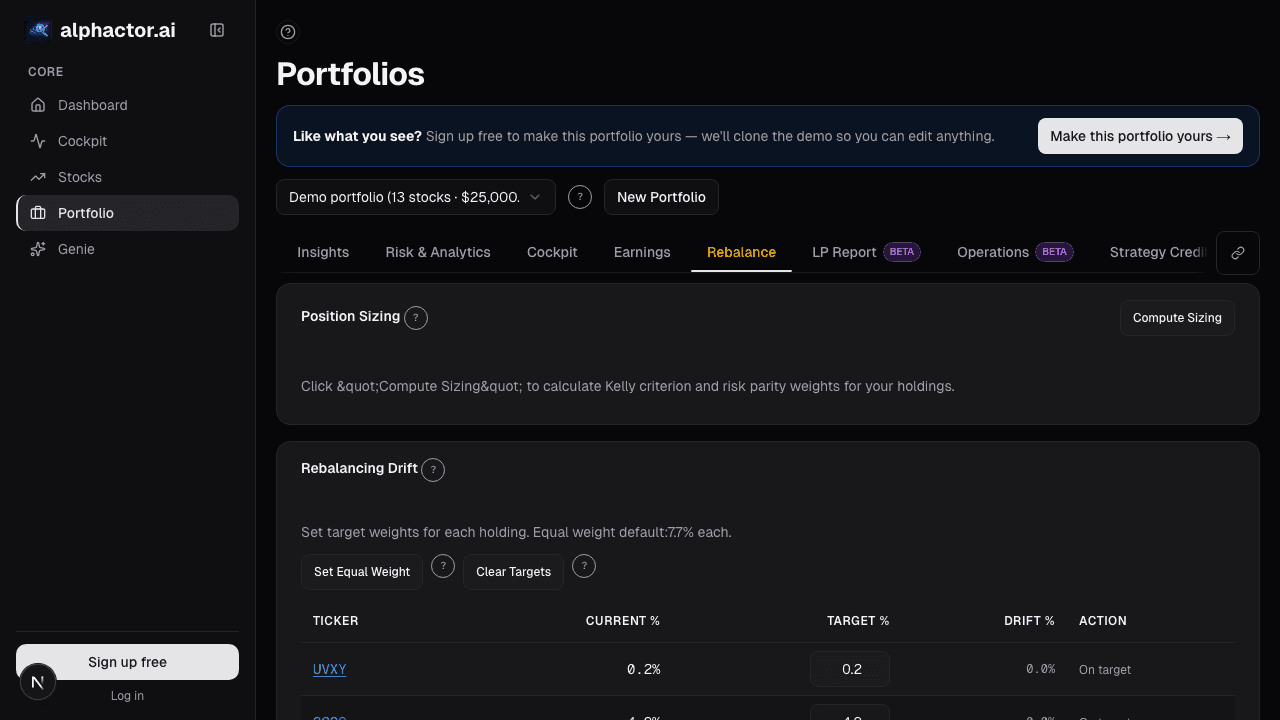

What the Portfolio Rebalance card shows

The Portfolio Rebalance card takes your target weights (defined in Portfolio Overview or imported from an optimizer output) and computes a concrete buy/sell list to move current weights back to targets:

- Per-position row: ticker, current weight, target weight, drift, recommended share change, estimated tax impact (based on available lots), estimated transaction cost

- "Minimize turnover" toggle: skips names within ±0.5% of target (no point rebalancing trivial drift and paying commissions for it)

- "Tax-aware" toggle: prefers lots with long-term gains, avoids lots within 30 days of wash-sale risk, shows the tax cost of each alternative

- Earnings-week filter: grays out names within their earnings disclosure window so you don't accidentally rebalance into a volatility event

- Scheduling: set the card to auto-compute a rebalance recommendation on the 1st of each month, or when aggregate portfolio drift exceeds threshold

- Export-to-broker integrations: preformatted order lists for Fidelity, Schwab, IBKR, and direct-entry via paper-trading

Three practices for rebalancing without breaking things

Monthly schedule with ±3% drift threshold. Too frequent (weekly) churns transaction costs without meaningfully improving risk; too rare (annually) lets risk drift materially. The monthly-with-threshold combination captures most of the benefit with minimal turnover. The threshold matters: 3% is enough to avoid chasing noise, tight enough to prevent the kind of structural drift I walked into in 2021. Some investors prefer semi-monthly with 2% threshold for slightly smoother tracking.

Tax-aware in taxable accounts. Retirement accounts (IRA, 401k) have no tax friction; rebalance freely. Taxable accounts require care. A naive rebalance that sells the short-term lots from your highest-appreciated position to correct a 1% weight drift can realize 30–40% short-term gains for relatively minor rebalancing benefit. The tax-aware algorithm selects long-term lots preferentially, uses loss lots when available, and can hit 80% of the rebalance goal with 20% of the tax cost. Always toggle it on for taxable.

Avoid earnings weeks. The position drift in earnings weeks is dominated by the earnings-announcement move, which is typically 5–15%, far more than a ±3% rebalance threshold. Rebalancing a position the day before earnings, only to see it move 10% overnight and need rebalancing again three days later, is double-transaction-cost for no benefit. The card's earnings-week filter grays out affected names. Wait for the week after earnings and the trades are both cheaper and cleaner.

Example: a rebalancing cycle

October 1, 2025, my own book. Target vs. current:

| Position | Target | Current | Drift | Action |

|---|---|---|---|---|

| Core US equity ETF | 40% | 46% | +6% | Trim 6% (LT lots available) |

| International ETF | 20% | 17% | -3% | Add 3% |

| Fixed income | 25% | 22% | -3% | Add 3% |

| Single names (5) | 10% | 11% | +1% | Skip (< threshold) |

| Cash | 5% | 4% | -1% | Skip |

Three trades needed. Tax-aware flagged that the US equity ETF trim could use only long-term lots (no short-term realization). Earnings filter was empty (no single-name earnings that week). Execution: trim US ETF 6% (realized LT gain, ~$4,800 at 15% = $720 tax cost), add to international and fixed income. Total transaction cost ~$15 across the three orders. Total tax cost $720. The rebalance realigned the book to target with minimal friction; my portfolio spent the next month tracking the benchmark weights rather than drifting further from them.

What rebalancing doesn't fix

- Wrong target weights. Mechanical rebalancing to a wrong target just enforces the wrong allocation. Target-setting is a separate strategic decision, not a rebalancing mechanic.

- Illiquid positions. You can't rebalance a position you can't trade. Small-cap illiquid names should be constrained to their current weight in the target, not treated as rebalanceable.

- Concentrated single-stock exposure in taxable accounts. A 30% position in one employer stock with massive embedded gains can't be rebalanced without huge tax cost. The strategic decision (diversification over time vs. tax deferral) is separate from mechanical rebalancing.

- Strategic allocation shifts. If you're moving from 60/40 to 70/30, that's a strategic change, not a rebalance. Execute it separately, slowly, with tax planning.

Common mistakes

- Rebalancing too often. Weekly rebalancing in a portfolio with > 10 positions churns transaction costs for negligible improvement.

- Ignoring the tax-aware toggle. In taxable accounts, not using it is a concrete dollar loss per rebalance.

- Rebalancing during a drawdown bottom. A bit counterintuitive, the schedule says rebalance, the emotion says wait. The schedule is usually right; the emotion is the thing I was trying to automate around.

- Setting drift threshold too tight. ±1% threshold captures noise and triples turnover without meaningful benefit.

- Rebalancing to last year's targets. Target review is separate from rebalancing; make sure targets still reflect your current strategic intent.

Where it fits

Pair with Portfolio Optimizer which defines target weights, Portfolio Holdings for the source-of-truth positions, and TCA to understand the implementation cost after-the-fact. Post-rebalance, Attribution shows whether the rebalanced allocation is delivering the expected risk/return.

FAQ

Monthly or quarterly?

Both work. Monthly captures drift faster, quarterly has lower turnover. I use monthly with threshold because it auto-skips no-action months anyway.

What about dividends and cash inflows?

The card treats dividends and cash inflows as natural rebalancing opportunities, deploy them into underweight positions before triggering any sales elsewhere. "Reinvest into weakness" is free rebalancing without tax cost.

How does this interact with tax-loss harvesting?

Tax-aware rebalancing can double as tax-loss harvesting if you explicitly tell it to prefer loss lots. The card has a TLH toggle that weights loss-selection more heavily.

What if I want to tactical-tilt (e.g., overweight energy)?

Express the tilt in the target weights themselves, not by skipping rebalances. If your tactical view is "overweight energy by 3% for the next 2 quarters," set the target accordingly and rebalance to it.

Does this work with fractional shares?

Yes. For small-AUM portfolios, fractional-share brokers reduce the minimum-rebalance problem materially. The trade list uses whole or fractional depending on broker capability.

Related reading

- Portfolio Alt Sentiment Integration

- Portfolio Attribution

- Portfolio Audit Trail

- Portfolio Credibility Scoring

Open the Portfolio Rebalance card → /app/portfolio

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Related reading

Alt-Data Sentiment at the Portfolio Level

Per-ticker alt-data breaks down past 10 positions. A roll-up of WSB, news, MSPR, and options lets a 90-second scan replace 100 minutes of manual checking.

Portfolio Attribution: Where Your Returns Actually Come From

Beating the benchmark by 400bps feels good until attribution tells you it was all allocation luck on one sector call. Selection vs. allocation vs.

Portfolio Audit Trail: Every Decision

Regulated managers need an audit trail. The Audit Trail card on alphactor.ai records every trade, rebalance, alert, and note into one timestamped log you…

Portfolio Credibility

Conviction is self-reported; credibility is externally anchored. The two diverge exactly where mistakes live, an 8% position in a name you love with a…

Portfolio Earnings: Calendar, Exposure

Earnings risk is about the whole book into the week, not each position. When 40% of NAV reports in one week, and 60% of that is in a single sector, you're…

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free