Bank Stocks and Interest Rates

Why the simplistic 'higher rates help banks' narrative breaks down, and how to analyze financial stocks through net interest margin, credit quality, and the…

Sarah Patel4 min read

Sarah Patel4 min readThe Conventional Wisdom Is Half Right

Ask any casual investor what happens to bank stocks when interest rates rise, and you will get the same answer: banks benefit because they earn more on loans. This is technically true and practically incomplete. The full picture is significantly more nuanced, and getting it wrong has cost investors real money during every rate cycle of the past two decades.

Banks do not simply benefit from higher rates. They benefit from a specific rate environment: moderately rising short-term rates, a positively sloped yield curve, stable credit conditions, and gradual enough increases that deposit costs lag asset repricing. When any of those conditions break down, the "higher rates help banks" thesis falls apart.

Net Interest Margin: The Engine of Bank Profitability

Net interest margin (NIM) is the spread between what a bank earns on its assets (loans, securities) and what it pays on its liabilities (deposits, borrowings). NIM is the single most important profitability metric for traditional banks and the primary channel through which interest rates affect earnings.

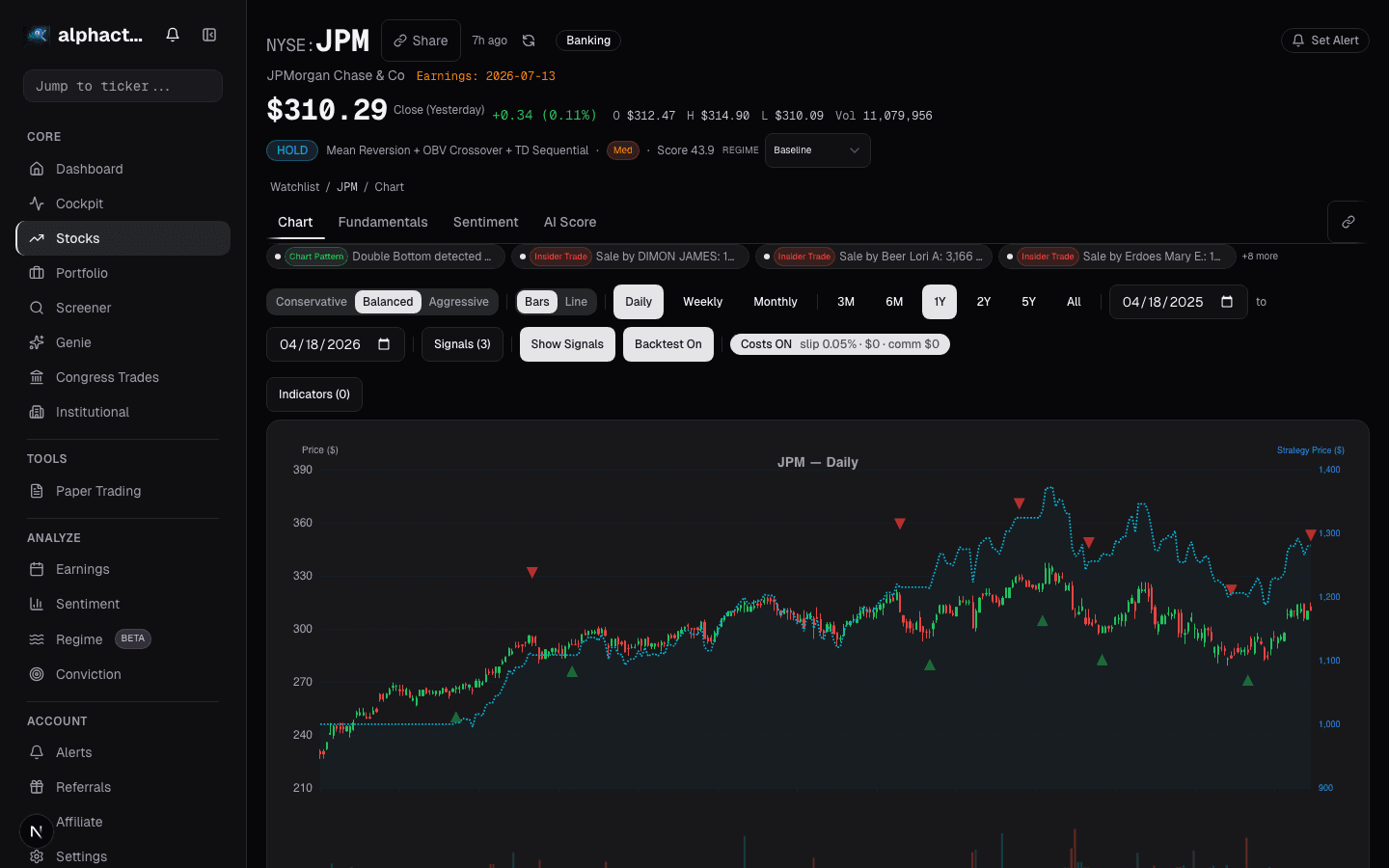

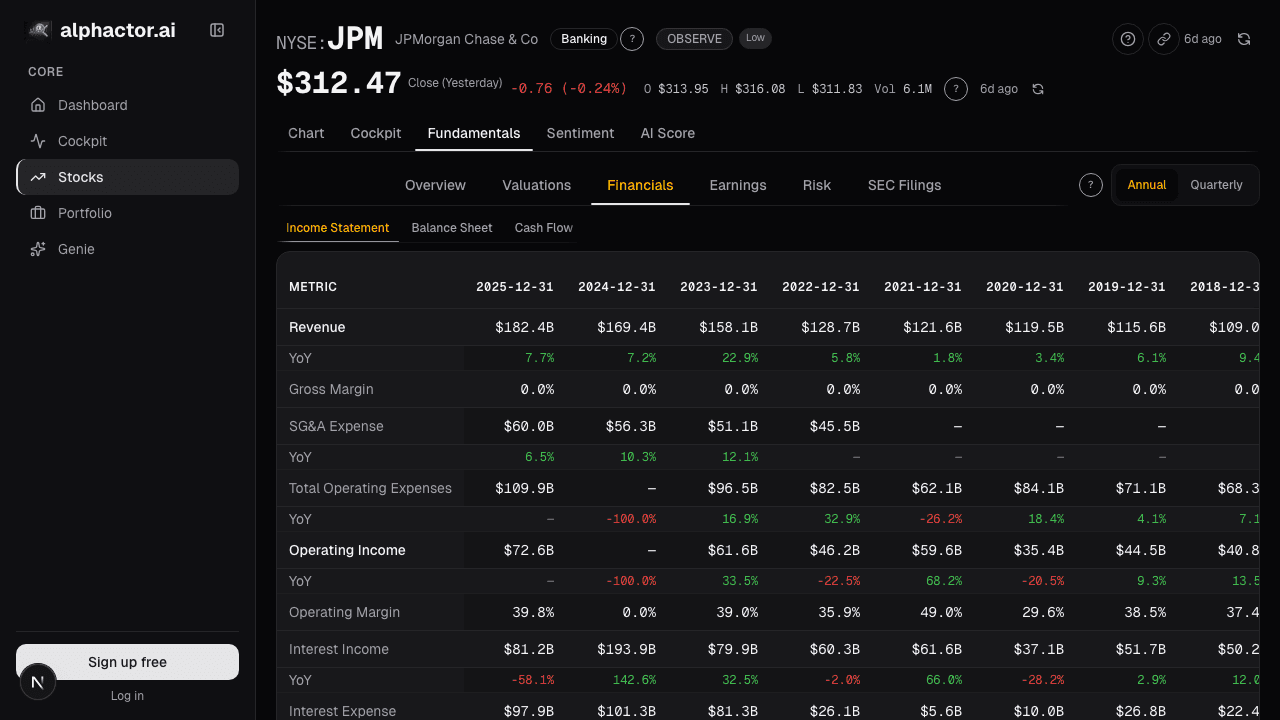

In theory, rising rates widen NIM because loan yields reprice faster than deposit costs. This worked in 2022-2023 for banks with strong deposit franchises. JPMorgan Chase's NIM expanded from 1.67% to over 2.60% as the Fed hiked from zero to 5.25%. But the benefit was not uniform. Banks relying on wholesale funding or rate-sensitive depositors saw funding costs rise nearly as fast as asset yields, compressing the spread.

The Yield Curve Matters More Than the Rate Level

The shape of the yield curve, specifically the spread between short-term and long-term rates, is more predictive of bank profitability than the absolute level of rates. Banks borrow short (deposits and short-term funding) and lend long (mortgages, commercial real estate, long-term bonds). A steep yield curve means wide spreads. A flat or inverted curve compresses that margin.

The 2023-2024 yield curve inversion was punishing for banks. Even with short-term rates at 5%, the 10-year Treasury yielded less than 4% for extended periods, meaning banks could not earn a spread on new long-duration lending. This is why bank stocks underperformed during parts of the rate hiking cycle despite rates moving higher.

The practical takeaway: when analyzing banks in the context of rate changes, look at the 2-year/10-year Treasury spread, not just the fed funds rate. A steepening curve is the strongest tailwind for the sector.

Credit Quality: The Risk That Rates Create

Here is where the "higher rates help banks" narrative completely breaks down. Sharply higher rates increase the probability of loan defaults. Borrowers with floating-rate debt see their payments rise. Businesses that relied on cheap financing face refinancing risk. Commercial real estate owners with maturing loans discover their properties no longer support the necessary debt service coverage ratios.

Loan loss provisions, the expense banks set aside for expected defaults, are a direct hit to earnings. In 2023, several regional banks saw provision expenses triple or quadruple as commercial real estate stress emerged. Silicon Valley Bank's collapse was an extreme case of interest rate risk materializing on the asset side of the balance sheet, but the underlying dynamic, rising rates devaluing existing assets, affected the entire sector.

The best bank stocks to own during rising rate environments are those with conservative underwriting standards, diversified loan books, and low exposure to rate-sensitive segments like office CRE. Alphactor's stock comparison tool helps isolate these factors by comparing provision expense ratios, loan-to-deposit ratios, and CET1 capital ratios across bank peers.

Deposit Betas: The Hidden Variable

Deposit beta measures how much of a rate increase gets passed through to depositors. A beta of 0.30 means that for every 100 basis point Fed hike, the bank raises deposit rates by 30 basis points, keeping the other 70 as margin.

Large money-center banks like JPMorgan and Bank of America run low betas because their branch networks create deposit stickiness. Smaller banks and online-only banks compete on rate and run betas of 0.60-0.80. In the 2022-2023 cycle, betas started low then accelerated as customers moved cash to money market funds. The banks that suffered most projected permanently low betas into their models. Deposit flight post-SVB accelerated this repricing.

How to Position Around Rate Cycles

Rather than making binary bets on rate direction, a more productive framework for bank investing considers four variables simultaneously:

Rate direction and speed. Gradual increases are positive; rapid hikes create credit stress. Cuts are negative for NIM but can relieve credit pressure.

Curve shape. Steepening is bullish. Flattening or inversion is a headwind regardless of rate levels.

Credit cycle position. Early in a credit deterioration cycle, provisions rise and earnings fall even if rates are supportive. Late in a recovery, credit tailwinds can offset rate headwinds.

Bank-specific fundamentals. Deposit franchise strength, loan book composition, capital levels, and fee income diversification all determine how a specific bank translates the macro environment into earnings.

Use the universe scanner to track whether financials are leading or lagging the broader market, which often reflects the market's collective read on these four variables. When the heatmap shows financials diverging from rate expectations, it is worth investigating whether the market is mispricing the nuance.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

How to Analyze Tech Stocks

The financial metrics that separate winning tech investments from hype-driven traps, with frameworks for evaluating SaaS, hardware, and platform businesses.

Defense Stocks: Government Contracts as a Revenue Moat

How defense contractors generate durable revenue through government contracts, and the metrics that matter for analyzing Lockheed Martin, RTX, and their peers.

Industrial Stocks: Betting on the Real Economy

How industrial stocks track economic growth, the leading indicators that predict their performance, and a framework for investing across the industrial…

Semiconductor Stocks: Cyclical, Essential

How to invest in semiconductor stocks by understanding the chip cycle, supply chain structure, and competitive moats that define the industry.

Utility Stocks for Income: Yield, Safety

How to evaluate utility stocks for income portfolios, including the regulatory framework, rate sensitivity dynamics, and metrics that identify quality…

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free