Industrial Stocks: Betting on the Real Economy

How industrial stocks track economic growth, the leading indicators that predict their performance, and a framework for investing across the industrial…

Marcus Chen4 min read

Marcus Chen4 min readThe Economy Made Tangible

Industrial stocks are the closest thing the equity market has to a direct bet on the real economy. These companies build, transport, and maintain the physical infrastructure of commerce: factories, railroads, aircraft, electrical equipment, HVAC systems, water treatment facilities. When economic activity expands, industrials benefit. When it contracts, they feel it immediately.

This macro sensitivity is both the sector's greatest advantage and its primary risk. Industrials give you leveraged exposure to GDP growth without the binary outcomes of biotech or the valuation compression risk of high-multiple tech. But they also decline faster than defensive sectors during recessions and offer limited protection when the economy weakens.

The Sub-Sector Map

Industrials is a broad sector that contains several distinct business models, each with different cycle sensitivity and growth characteristics.

Aerospace and defense (Honeywell, GE Aerospace, TransDigm) benefits from long-duration aviation cycles and defense budgets. Aircraft orders placed today deliver revenue for 7-10 years, and the post-COVID travel recovery has driven a multi-year order boom benefiting the entire supply chain.

Railroads (Union Pacific, CSX, Norfolk Southern) are oligopoly businesses with pricing power, high barriers to entry, and volumes tied to freight activity. Rail pricing consistently exceeds inflation because shippers have limited alternatives for long-haul freight.

Electrical equipment (Eaton, Emerson Electric, Parker Hannifin) sells into diverse end markets including construction, energy, and manufacturing. Companies like Eaton have repositioned toward electrification, adding secular growth on top of the cyclical base.

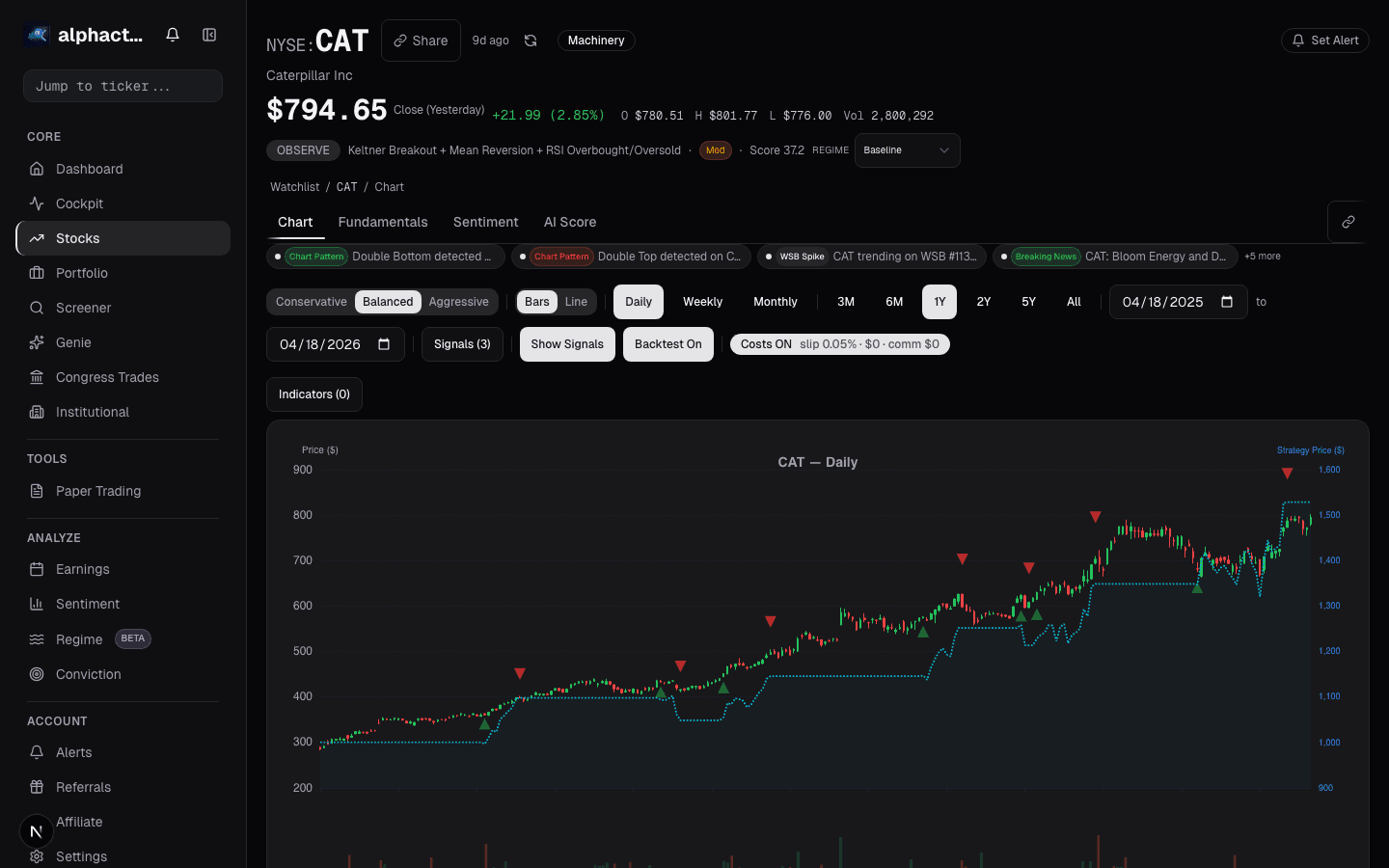

Machinery (Caterpillar, Deere, Illinois Tool Works) provides equipment for construction, mining, and agriculture. Classic cyclicals with high operating leverage: Caterpillar's earnings can swing 40-50% in a single cycle.

Transportation (FedEx, XPO, C.H. Robinson) directly tracks freight volumes. Rates and volumes are coincident indicators of economic health and provide early signals of acceleration or deceleration.

Leading Indicators for Industrial Timing

The industrial sector's cycle sensitivity means timing matters more than in defensive sectors. Several indicators reliably signal turning points:

ISM Manufacturing PMI. A reading above 50 indicates expansion; below 50 indicates contraction. The direction of change is more predictive than the level. PMI troughing and starting to rise, even from contractionary levels like 46 to 48, historically generates positive industrial stock returns over the following 6-12 months.

Architectural Billings Index (ABI). Billings lead construction activity by 9-12 months, signaling future demand for electrical equipment, HVAC, and building materials companies.

Freight volumes. The Cass Freight Index and DAT spot rates provide real-time reads on transportation demand. Rising volumes confirm economic acceleration; falling volumes signal deceleration.

Core capex orders. The Census Bureau's nondefense capital goods orders excluding aircraft is the best proxy for business investment trends driving industrial demand.

When these indicators align in an uptrend, industrial stocks typically outperform by 500-1000 basis points annually. When they deteriorate in concert, the underperformance is equally sharp.

Valuation Through the Cycle

Like semiconductors, industrial stocks require cyclical adjustment to avoid the peak-earnings trap. A machinery company at 12x peak earnings may look cheap but could be at 20x normalized earnings near cycle top. Conversely, the same company at 25x trough earnings may be a bargain if recovery is imminent.

The approach that works: compare current valuations to the mid-cycle P/E range using 5-year average earnings. The opportunity exists when leading indicators suggest the market's embedded assumptions are wrong. Alphactor's stock comparison tool displays historical valuation ranges alongside current metrics, making it straightforward to screen for industrials where pessimism may be overdone.

The Quality Premium in Industrials

Not all cyclicals are created equal. Within industrials, a clear quality tier of companies has demonstrated the ability to grow earnings through cycles, not just with them. These companies share common traits:

Aftermarket revenue. TransDigm generates the majority of revenue from proprietary aerospace replacement parts at high margins. Aftermarket revenue is recurring, higher-margin, and less cyclical than original equipment sales.

Pricing power. Companies with proprietary products or sole-source positions raise prices consistently. Parker Hannifin and Roper Technologies have demonstrated steady pricing above input cost inflation across multiple cycles.

Portfolio management. The best conglomerates actively divest low-margin cyclical segments and acquire higher-quality businesses. Danaher pioneered this with the Danaher Business System. Honeywell, Emerson, and GE have pursued similar transformations.

Quality industrials command higher multiples (18-25x) but deliver more consistent returns with lower drawdowns than commodity cyclicals. For long-term holders, paying the premium is usually worth it.

Portfolio Role

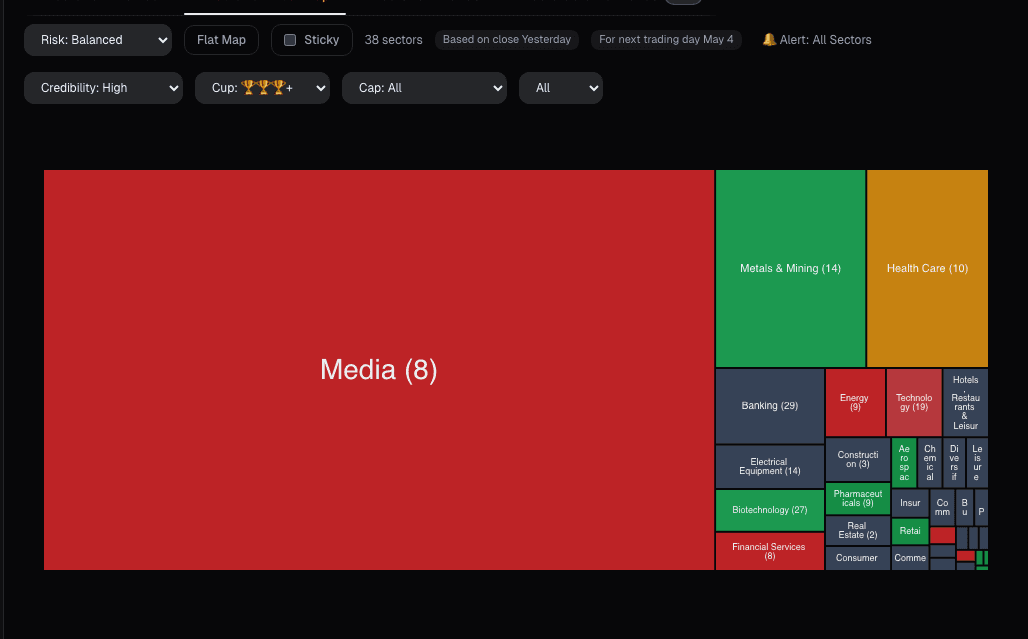

Industrial stocks belong in the cyclical growth allocation of a diversified portfolio, typically 8-12% of equities. Increase exposure when leading indicators are turning up from depressed levels. Reduce when indicators peak and start rolling over. Use the universe scanner heatmap to monitor relative performance; industrials leading the market usually confirms economic expansion, while persistent underperformance is an early recession warning.

The real economy does not disappear during downturns. It contracts and then expands again. Industrial stocks give you a direct way to participate in that expansion, provided you respect the cycle and buy when the PMI is ugly, not when the headlines are cheerful.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

How to Analyze Tech Stocks

The financial metrics that separate winning tech investments from hype-driven traps, with frameworks for evaluating SaaS, hardware, and platform businesses.

Market Regime on the Chart

Regimes change discretely, but regime models detect them in near-real-time. The Market Regime overlay annotates where the regime flipped so you can see…

Consumer Staples as Portfolio Defense

Why consumer staples outperform during downturns, which metrics define quality in the sector, and how to use boring stocks as portfolio insurance.

Defense Stocks: Government Contracts as a Revenue Moat

How defense contractors generate durable revenue through government contracts, and the metrics that matter for analyzing Lockheed Martin, RTX, and their peers.

Energy Stocks and the Commodity Cycle

How commodity price cycles drive energy stock returns, and a framework for timing entries and exits across upstream, midstream, and downstream companies.

How Fed Policy Actually Affects Your Stock Portfolio

A practical guide to understanding how interest rate decisions, quantitative tightening, and Fed communication move equity markets at the sector and stock…

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free