Form 4 Decoded: Insider Trades That Mean Something

A '$2M insider sale' headline hides what actually happened. A discretionary sale at CEO-level the week after a bad call is loud; the same CEO selling on a…

Marcus Chen6 min read

Marcus Chen6 min readIn January 2024 a finance Twitter thread was making the rounds about a consumer-products CEO who had "dumped $4.8M of stock" in the week following a mildly disappointing earnings print. The framing was that the dump confirmed the earnings weakness was the beginning of something worse. I pulled up the Form 4 detail on the transactions card and the story fell apart immediately. The transactions were all coded S-Plan, sales executed under a 10b5-1 plan filed 11 months prior, with pre-scheduled quarterly dates that had been public for the entire period. The sale dates were exact plan dates, not discretionary. The CEO hadn't "dumped" anything reactive to the earnings; the sales were mechanical, scheduled, and pre-committed before the earnings print was even on the calendar. The "sell signal" in the thread was fabricated from a misread of the filing. The stock recovered its post-earnings losses over the next six weeks; the thread's "confirmed bearish" call turned out to be based on a code they hadn't looked at. That's the archetypal Form 4 misread: looking at dollar values without reading transaction codes, and drawing conclusions from the wrong number. The code is where the information lives.

This post is about the Insider Transactions table, why transaction codes matter more than dollar amounts, and the six codes that cover 95% of what you'll actually see.

TL;DR

- Code determines meaning; dollar amount alone is uninterpretable.

- P (open-market purchase) is the strongest bullish signal: insider using personal cash to buy.

- S-Plan (10b5-1 scheduled sale) is noise: pre-committed months in advance.

- M+S (option exercise + sale) is mechanical: ignore unless magnitude is very unusual.

- G (gift) and F (tax withholding) are non-discretionary: ignore.

Why codes matter more than numbers

A Form 4 filing reports an insider transaction with a single-letter SEC transaction code that describes what actually happened. The code is the single most important field; the dollar value and share count are meaningless without it. Without the code:

- A sale could be the CEO liquidating on a pre-set plan (noise) or dumping discretionary stock after seeing bad news (signal)

- A sale could be the same-day consequence of exercising options (mechanical) or a new market-open order (discretionary)

- A buy could be an open-market purchase with personal cash (signal) or a grant-related transaction (noise)

Headlines and many retail interpretations ignore the code entirely, treating all transactions as equivalent. They aren't. A single P-code purchase by a CFO at $300k is often more informative than ten S-Plan sales totaling $10M.

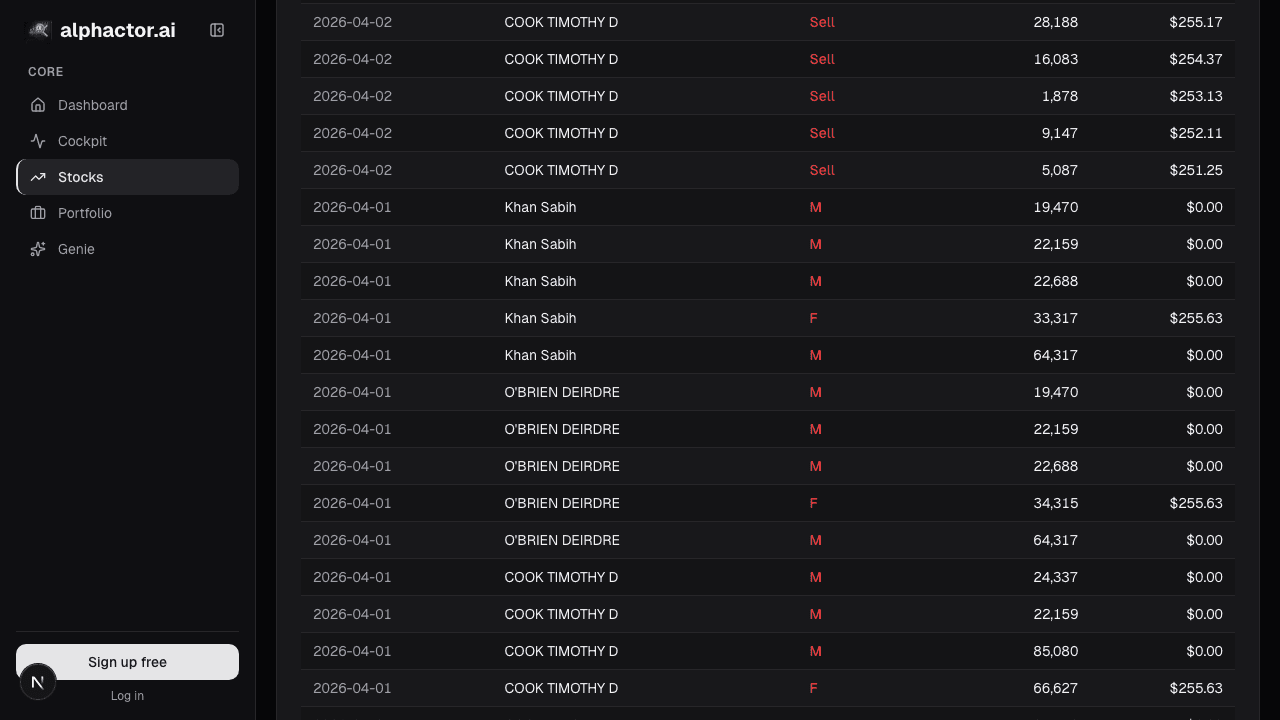

What the Insider Transactions table shows

The Insider Transactions table lists every Form 4 filed in the trailing 180 days:

- Transaction date and filing date (can differ by days, the lag is itself informative)

- Insider name and role: CEO, CFO, other officer, director, 10% owner

- Transaction code: the critical field

- Shares and price and net dollar value

- 10b5-1 plan flag: was the transaction under a pre-scheduled plan?

- Post-transaction holdings: how much the insider owns after the trade

- SEC filing link: click-through to the full Form 4 on EDGAR

- Filter by code: most useful: filter to P only to surface open-market purchases

The six codes that matter

P, Open-market purchase. The strongest bullish signal. An insider used personal cash to buy shares at market price on an open exchange. There is no offsetting compensation, no tax obligation, no scheduled plan, just a discretionary decision to add exposure. Purchases by the CFO or by multiple non-related officers in the same window are the highest-signal versions.

S, Open-market sale (discretionary). Ambiguous on its own. Could be routine liquidation for diversification, could be a response to internal information. Always check the 10b5-1 flag: S without plan coverage is discretionary and worth attention; S-Plan is mechanical and rarely informative.

M, Option exercise. Mechanical, the insider exercised options to convert to shares. Usually immediately followed by S (sale) on the same day to cover the exercise cost and tax. M+S on the same day is the most common Form 4 pattern; it's compensation realization, not a view. Ignore unless the exercise quantity is wildly out of pattern for the insider.

A, Award / grant. Not a transaction in the discretionary sense, it's a grant of stock or options from the company. Zero information content about the insider's view. Ignore.

G, Gift. The insider transferred shares to a trust, family member, or charity. Often tax-motivated (estate planning) or charitable. Slightly bearish as a soft signal but usually not material.

F, Tax-withholding sale. Shares automatically withheld by the company to cover taxes on vested restricted stock. Forced, non-discretionary, zero information. Ignore.

Filtering aggressively to P-code transactions (and S-code without plan coverage, for bearish reads) reduces the noise in the table by roughly 80%. The remaining 20% is where the information lives.

Example: the January 2024 "CEO dump" that wasn't

The actual filings on the consumer-products CEO:

| Filing Date | Code | Shares | Value | 10b5-1? | Interpretation |

|---|---|---|---|---|---|

| Jan 8 | S-Plan | 30,000 | $1.5M | Yes (filed Feb 2023) | Scheduled, noise |

| Jan 8 | S-Plan | 20,000 | $1.0M | Yes | Scheduled, noise |

| Jan 15 | S-Plan | 25,000 | $1.25M | Yes | Scheduled, noise |

| Jan 22 | S-Plan | 21,000 | $1.05M | Yes | Scheduled, noise |

Four filings, $4.8M total, zero discretionary. All dates were pre-scheduled 11 months prior. The plan predated the quarter in question entirely; the CEO couldn't have timed sales around an earnings print that hadn't yet happened when the plan was filed. The thread had conflated "large dollar sales" with "bearish insider activity" by ignoring the plan coverage and the transaction code. Reading two columns (code and 10b5-1 flag) in the table would have prevented the misinterpretation in 10 seconds.

What the table can miss

- Planned vs. re-planned. An insider can amend a 10b5-1 plan; amendments are flagged but occasionally obscured.

- Beneficial-ownership structures. Complex trust arrangements can show up as "indirect" transactions that are hard to interpret.

- Cross-trading between related insiders. Husband-wife or founder-family transactions often net out without being informative.

- Delayed filings. Late Form 4s can skew the recency ordering; the filing date vs. transaction date gap matters.

- Secondary-offering sales. Some sales happen during a registered secondary; those are book-building, not discretionary signal.

Common mistakes

- Aggregating dollar values across codes. $10M of M+S is meaningless; $500k of P is meaningful.

- Treating S as bearish without checking 10b5-1. S-Plan is not a discretionary sale.

- Ignoring role. The CFO's signal is usually stronger than a director's.

- Weighting by dollar size only. A $100k P by a CFO is stronger than a $5M S-Plan by a director.

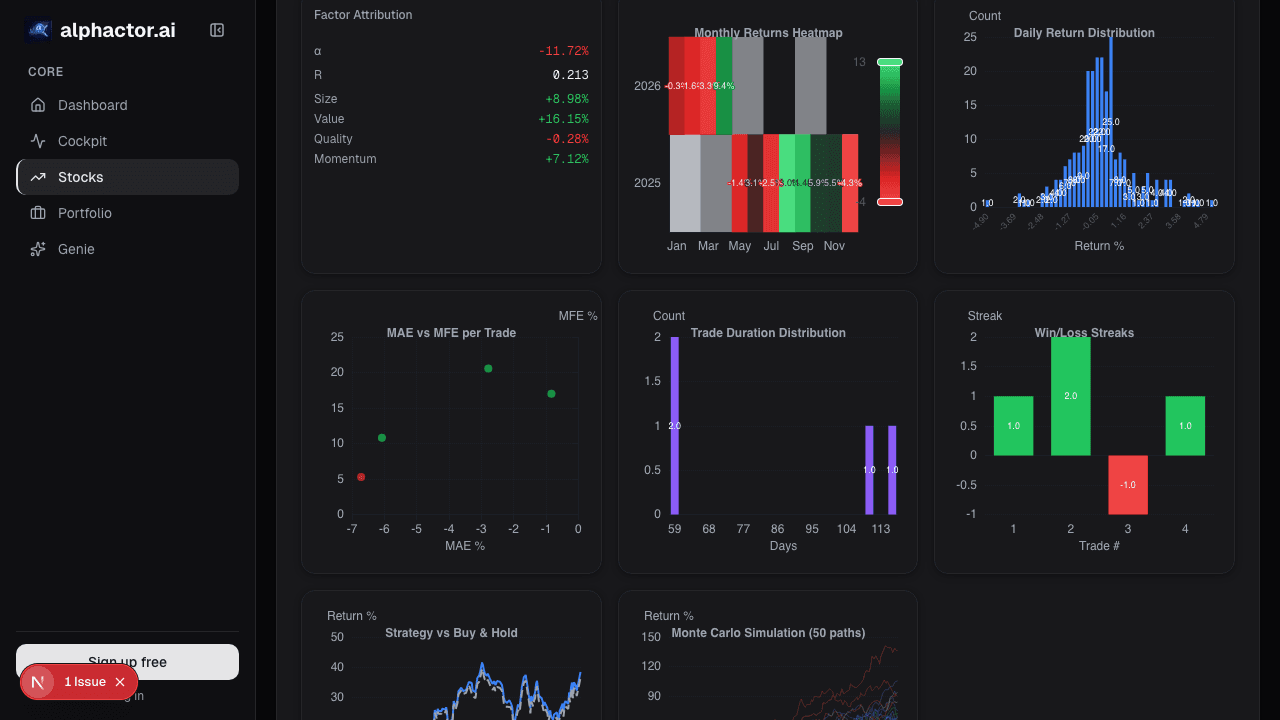

- Reading a single transaction in isolation. The pattern across 30-90 days is what informs, clusters, not singletons.

Where it fits

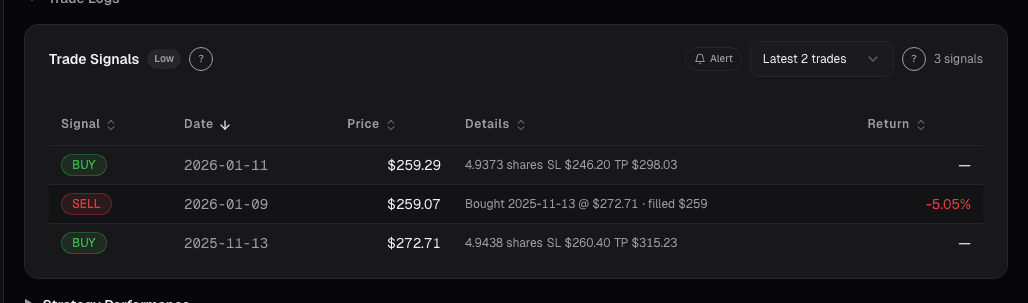

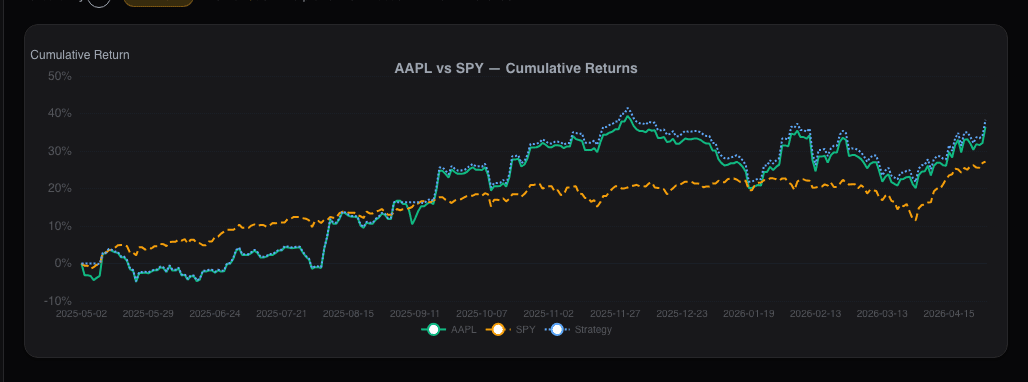

The transactions table is the detail layer behind the MSPR chart. When MSPR spikes green, come here to verify the spike came from real P purchases, not a one-off outlier. Combine with Institutional Holders to see whether insiders and 13F filers are moving the same direction, when they diverge, insiders have usually been right on 6-month horizons.

FAQ

How fresh is the data?

Form 4s appear within 48 hours of filing (SEC requires filing within 2 business days of the transaction).

What does "indirect" beneficial ownership mean?

The insider benefits from the shares but they're held in a trust, LLC, or family entity. Still counts as insider ownership for reporting purposes.

Why do CEOs file so many S-Plan sales?

10b5-1 plans let insiders diversify without insider-trading liability. Scheduled sales are a normal part of executive compensation realization.

Are all officer purchases P-code?

Yes, if the purchase is open-market. Shares received via option exercise are M-code, not P.

What about Section 16 vs. non-Section 16 filings?

Section 16 officers, directors, and > 10% holders file Form 4. Other employees don't. Form 4 covers the people whose transactions matter most for signal.

Related reading

- Insider MSPR, Net Purchases

- Congress Trades per Ticker

- Corporate Lobbying Spend

- Dark Pool Prints Explained

Open the Insider Transactions table → /app/stocks/AAPL/sentiment

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Congressional Trades on a Single Stock

The 'Congress outperforms the market' story hides where the actual signal is. It's not aggregate Congressional portfolios, it's a single committee chair's…

Corporate Lobbying Disclosures

Lobbying spend publicly discloses which regulatory fights a company is fighting. A quarter-over-quarter jump in contacts to a new agency often precedes the…

Dark Pool Prints

Off-exchange share above 45% clustered into weakness signals institutional accumulation. Dark pool prints are regulated, post-trade transparent, and measurable.

Dashboard News: A Filtered Stream Across Your Holdings

Generic news feeds drown you in noise. The Dashboard News card filters by your holdings and ranks by sentiment impact: what's new, what matters, why.

Insider MSPR: The Ratio That Cuts Through Form 4 Noise

MSPR strips 10b5-1 sales to show discretionary insider buying. Cluster above 0.7 from three or more insiders has outperformed by 4-6% over three months.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free