Part of: Technical Analysis

Dark Pool Prints

Off-exchange share above 45% clustered into weakness signals institutional accumulation. Dark pool prints are regulated, post-trade transparent, and measurable.

Jake Morrison7 min read

Jake Morrison7 min readIn October 2023 I was watching a mid-cap enterprise software name that had been range-bound between $38 and $42 for six weeks. Public-tape volume looked pedestrian and the price action was uninteresting. The dark-pool card told a different story. Across the four weeks prior, off-exchange volume had been averaging 49% of total daily volume, well above the 38% 90-day median. The individual prints were clustered: 3-5 prints per day at 15,000-40,000 shares each, timestamped during price weakness rather than strength. That's the textbook pattern of institutional accumulation, funds that don't want to show a bid on the public book but are happy to take size from motivated sellers through a dark pool. Three weeks later the company pre-announced an earnings beat ahead of its scheduled print; the stock gapped to $46 and held. What the tape had shown in retrospect was a four-week window where big holders had been adding, quietly, without moving the quoted price. The dark-pool card wasn't giving me the fundamental story, I had to infer that, but it was giving me the positioning story, and the positioning led the fundamental by weeks. That's the main value: not "buy on this signal" but "something structural is building that the tape itself is hiding."

This post is about the Dark Pool card, what off-exchange prints actually are, and the two reads that translate dark-pool share and print timing into an accumulation-vs-distribution inference.

TL;DR

- Dark pools are regulated ATSs, not shadowy venues. Prints report within 10 seconds under TRF codes.

- Dark-pool share above 45% of total volume is unusually high. Baseline for most names is 30-40%.

- Prints clustered into weakness ≈ accumulation. Prints clustered into strength ≈ distribution.

- Direction is an inference, not a fact. The tape shows fills, not bid/ask side.

- Pair with insiders, options flow, or 13F momentum for confirmation. Single-signal dark pool is weak; stacked, it's strong.

What dark pools actually are

The myth is that dark pools are hidden or unregulated. They aren't. A dark pool is an Alternative Trading System (ATS), a private venue registered with the SEC that matches large institutional orders away from the public order book, then reports each fill within 10 seconds to a TRF (trade reporting facility) feed. The consolidated tape shows every fill. What's not public is the limit book: the unfilled orders sitting in the pool. You see fills; you don't see intent.

The reason dark pools exist is market impact. If a fund needs to buy 500,000 shares of a mid-cap with 1.5M daily volume, working that order through the public book would move the quote several percent against them before they're half-filled. Dark pools let them match with natural sellers, other funds that want to exit, at sizes and prices that wouldn't clear on the public book. The trade reports after the match, post-trade transparent, but the price-impact damage is avoided because the quote never moved during the negotiation.

This matters for reading the signal because:

- Dark-pool fills are mostly institutional (retail orders almost always route to market makers, not dark pools)

- Print size is a weak proxy for conviction (the fund wanted this size, was willing to commit capital for it)

- Print timing within the day can hint at direction without revealing it explicitly

What the Dark Pool card shows

The Dark Pool card tracks off-exchange prints on a rolling intraday and daily basis:

- Today's dark-pool share as a % of total volume

- 20-day and 90-day moving averages for comparison

- Print count over size threshold: 10k+ shares for large-caps, 2k+ for mid-caps

- Largest print of the day with timestamp

- Print timeline: every flagged print plotted alongside the price path intraday

- Percentile flag: prints above the 80th percentile of recent history highlighted

- Cumulative off-exchange volume trending over the last 20 sessions

- Daily print distribution: how clustered vs. dispersed the fills were

Two reads that convert fills to inference

Prints clustered into weakness = accumulation. When the price is drifting down on the public tape and dark-pool share jumps to 45%+ with multiple large prints timestamped during the weakness, the inference is that institutions are adding positions, using the weakness to take size from sellers without pushing the public quote down further. The pattern is especially strong when it persists over multiple days: a single weak session with high dark-pool share is noise, but four weeks of "weak days have high off-exchange volume" is accumulation.

Prints clustered into strength = distribution. The inverse pattern. When the price is rallying and dark-pool share spikes on the up-days, particularly late in a multi-week rally, institutions are more likely distributing into the strength. They're exiting using the rally to find natural buyers in the dark pool, keeping the public quote from giving the exit away. This read is more subtle than the accumulation read because rallies naturally attract trading volume, so the threshold for "unusual" distribution has to be higher.

Neither read is definitive. Dark-pool prints show fills, not aggressor side. A single trade through a dark pool can be a buyer or a seller. The inference from clustering is probabilistic: the *pattern* of when prints happen, not any individual print, is what's informative. That's why dark-pool reads always need corroboration from a second signal, insiders, options flow, 13F momentum, or news context, before they turn into a trade.

Example: October 2023 enterprise software accumulation

The dark-pool pattern over the 4-week accumulation window:

| Week | Dark-pool share | Avg print count/day | Price range | Intraday timing |

|---|---|---|---|---|

| W1 | 47% | 5 | $38-41 | 80% on down ticks |

| W2 | 51% | 6 | $38-40 | 75% on down ticks |

| W3 | 48% | 4 | $39-42 | 70% on down ticks |

| W4 | 53% | 7 | $38-40 | 85% on down ticks |

| 90-day median | 38% | 2 | , | 50% (neutral) |

Dark-pool share consistently 10-15 points above the 90-day median; print count 2-3× normal; timing heavily skewed toward weakness. That's the cleanest accumulation signature you can get from the card. The pre-announcement arrived three weeks after week 4; someone had been building a position over that window. I'd taken a tag-along long in week 2 based on the pattern, sized conservatively because dark-pool inference is never certain. The pre-announcement was the confirmation.

What the dark-pool card can miss

- Direction ambiguity. The tape doesn't tell you who's buying. Inference is probabilistic, not deterministic.

- Multi-leg and hedging prints. A large print may be one leg of a complex trade (risk arb, pair trade, option-equity hedge) that doesn't imply directional conviction.

- Dealer inventory. Market-maker fills through dark pools are inventory management, not positioning.

- Index rebalance effects. Index changes force mechanical dark-pool fills; those are scheduled flow, not conviction.

- ETF creation/redemption. ETF APs use dark pools heavily; high dark-pool share during ETF flow events is mechanical, not directional.

Common mistakes

- Trading on a single-day print spike. One unusual day is noise; the signal is in multi-day clustering.

- Ignoring the price-path context. A large print is neutral; a large print during weakness is bullish-leaning.

- Taking dark-pool reads as standalone triggers. They're corroborating signals, not primary ones.

- Confusing absolute print size with significance. A 30k print in a mid-cap is large; the same print in AAPL is routine.

- Forgetting the 10-second report delay. Dark-pool prints appear on tape a few seconds after execution; the timestamping is accurate but not real-time.

Where it fits

Dark pool activity is a tape-reading supplement, not a trade trigger. Use it to confirm a thesis from Insider MSPR or Unusual Options Activity. When insiders are buying, MSPR is green, and dark pool prints cluster into weakness on the same week, three independent institutional proxies are pointing the same direction. For longer-horizon flow that lags but confirms, cross-reference Institutional Holders quarterly.

FAQ

How fresh is the data?

Near-real-time intraday. Prints appear on the card within a few seconds of the TRF report.

What does "dark-pool share" normalize against?

Total daily consolidated volume, both public and off-exchange. The share % is off-exchange volume / total volume.

Does the card show which ATS executed each print?

Sometimes, FINRA publishes ATS-specific data on a weekly lag. Aggregate dark-pool share updates intraday.

Are retail trades ever routed through dark pools?

Rarely. Retail orders predominantly route to market makers (PFOF) or wholesalers. Dark-pool fills are overwhelmingly institutional.

Is high dark-pool share always a signal?

No. Very liquid names have structurally higher dark-pool share (SPY, QQQ routinely >50%). The signal is deviation from the name's own baseline.

Related reading

- Institutional Holders, 13F

- Dark Pool Activity Guide

- Congress Trades per Ticker

- Corporate Lobbying Spend

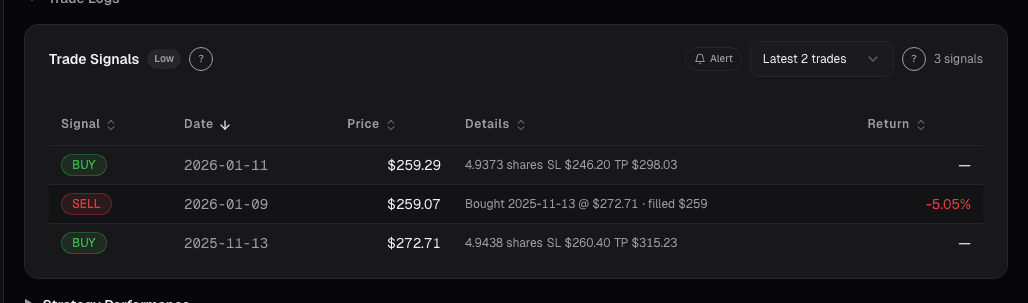

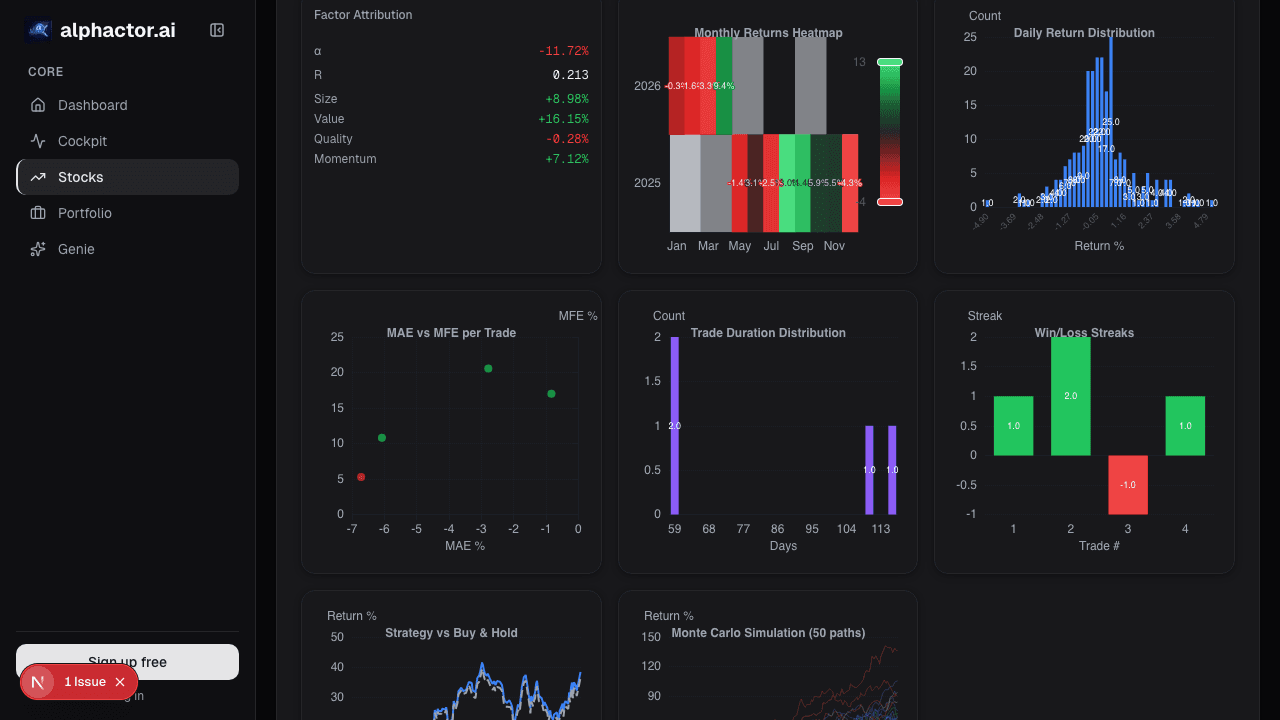

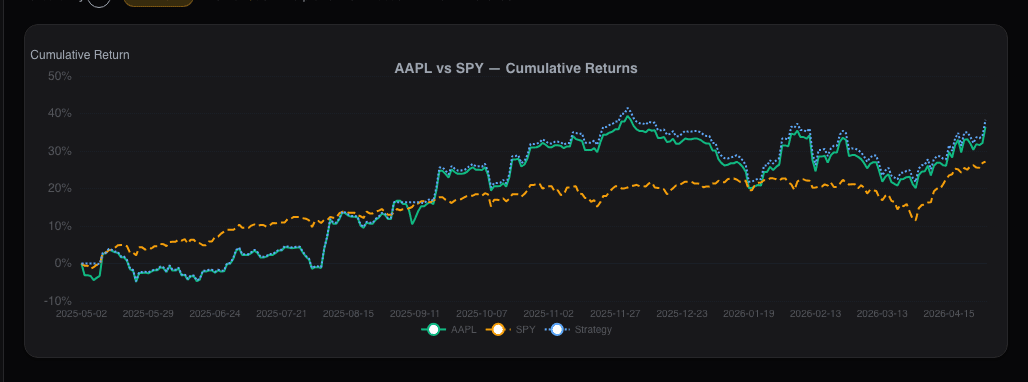

Open the Dark Pool card → /app/stocks/CRWV/sentiment

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Congressional Trades on a Single Stock

The 'Congress outperforms the market' story hides where the actual signal is. It's not aggregate Congressional portfolios, it's a single committee chair's…

Corporate Lobbying Disclosures

Lobbying spend publicly discloses which regulatory fights a company is fighting. A quarter-over-quarter jump in contacts to a new agency often precedes the…

Dark Pool Activity: Reading the Institutional Order Flow

What dark pools are, why institutions use them, and how tracking dark pool prints and volume can reveal where smart money is positioning before it shows up…

Dashboard Movers: Catching Unusual Moves Before They're Old

Most platform movers lists are dangerous, they rank by % change alone, surfacing illiquid small-caps on meaningless volume.

Dashboard News: A Filtered Stream Across Your Holdings

Generic news feeds drown you in noise. The Dashboard News card filters by your holdings and ranks by sentiment impact: what's new, what matters, why.

ETF Holdings: How Passive Flows Shape a Stock's Path

For large-cap US equities, 20-40% of shares outstanding sit inside ETFs that trade mechanically on creation/redemption, not fundamentals.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free