Regime-Aware Strategy Selection

Markets cycle through trends, ranges, and shocks. Learn how regime detection drives which strategy runs, and why a mixture of experts beats a single static…

Marcus Chen5 min read

Marcus Chen5 min read

The Single-Strategy Trap

Most backtested rules look great in one market and ugly in the next. A trend-following system wins in 2017 and 2023, then gives it all back in 2022. A mean-reversion rule thrives in quiet ranges and then hemorrhages through a breakout month. The ugly truth is not that the strategy is wrong, it is that the strategy is right for one regime and wrong for another.

When you treat a backtest as a single number, "this rule earned 14% CAGR over ten years", you paper over months where it lost 8% because the market stopped behaving the way the rule needed. Live trading exposes that immediately. The strategy does what it was optimized to do, the market does something else, and you sit at -8% watching the rule generate textbook signals into a hostile tape.

The fix is not a better indicator. It is to stop pretending the market is one thing.

What a Regime Actually Is

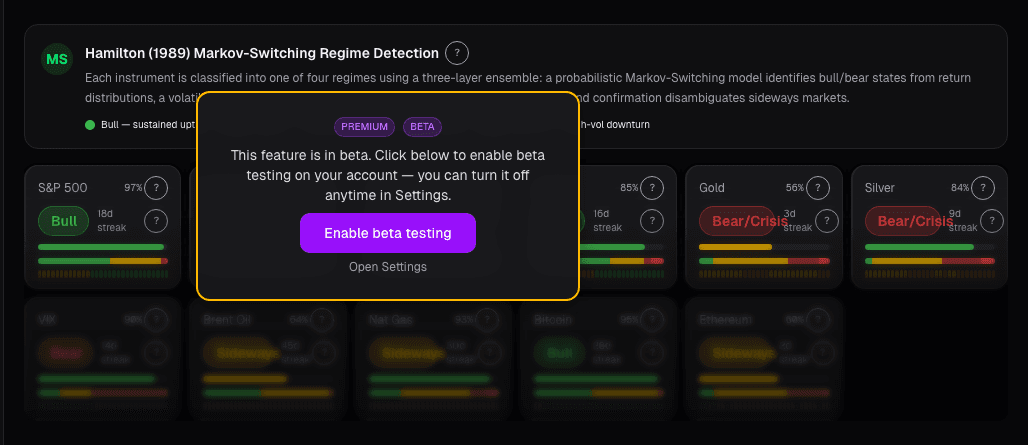

Academically, a market regime is a hidden state that changes which statistical properties hold. Practically, you can describe most US-equity regimes with four observable conditions:

- Trend strength. Is price above or below its 200-day moving average, and is the slope positive or negative?

- Volatility state. Is realized volatility inside its normal band, expanding into a stress move, or compressed into a coil?

- Breadth. Is most of the market participating, or is a handful of mega-caps dragging the index while the median stock bleeds?

- Dispersion. Are correlations crashing toward 1 (risk-off) or spreading out (stock-pickers market)?

Combine those and you get a handful of named states, `trending_calm`, `trending_volatile`, `ranging`, `crisis`, `recovery`, and each one favors a different kind of rule. Trends reward momentum and breakouts. Ranges punish them and reward mean reversion. Crises reward defense and cash. Nothing is universal.

The Four Selection Modes We Run

Alphactor's regime-aware strategy selection has four modes that trade off conservatism against aggressiveness. You can inspect each one in the strategy comparison panel before committing capital.

1. Baseline

Baseline runs a single strategy regardless of regime. It is the control group. Every other mode has to beat it out-of-sample or it is not doing real work. If your mixture of experts can't outperform the baseline on a rolling window, you do not have a mixture problem, you have a feature problem.

2. Shadow

Shadow runs two strategies simultaneously: the baseline trades real capital and a candidate regime-switching rule trades on paper. Their PnLs diverge and converge over time, and the gap tells you whether the switching logic adds real value or just churns turnover. Shadow is our default for any new selection policy, we run it for at least 60 trading days before promoting to live.

3. Hard Switch

Hard switch commits to one expert at a time. When regime classification flips, the old strategy is fully exited and the new one is entered. It is decisive, easy to reason about, and prone to whipsaw at regime boundaries. If the regime signal is noisy, hard switching will chop you. The defense is to require a persistence threshold, for example, the regime must hold for five consecutive days before the switch is honored.

4. Soft Mixture of Experts (MoE)

Soft MoE weights multiple strategies by regime probability. Instead of "we are in regime A, run strategy A," it runs "regime A has 0.6 probability, regime B has 0.3, regime C has 0.1" and blends the three strategies' signals accordingly. Near regime transitions, the times hard switching hurts most, soft MoE degrades gracefully. Well inside a regime, it behaves close to the dominant expert.

Soft MoE is our recommended default for most portfolios. It sacrifices a little peak performance inside a stable regime in exchange for much better transition behavior.

What Changes in Your Signals

When regime-aware selection is on, two things change in how the platform recommends trades:

Signal weights reflect regime. A momentum buy signal in a trending regime carries full weight. The same signal in a ranging regime is discounted or ignored. You see this in the conviction score, a rule that fires in the wrong regime shows up with lower conviction.

Strategy recommendations rotate. The backtest leaderboard on a ticker is not a fixed ranking. It is filtered by the regime the platform currently classifies. A mean-reversion strategy that topped the leaderboard last quarter may not appear at all this quarter because the classified regime no longer favors it.

When Regime Selection Hurts

Regime-aware selection is not free. It has two failure modes worth naming:

Regime classification error. If the classifier is wrong, you run the wrong expert. A false "trend" classification during a genuine ranging market will put you into a breakout rule that gets stopped out repeatedly. This is why we expose the regime probability vector, if you see probabilities split across three regimes at 0.35 / 0.33 / 0.32, trust the signal less, not more.

Overfit experts. If each expert is overfit on its training regime, the ensemble is overfit too, you have not escaped the single-strategy trap, you have just multiplied it by four. The defense is walk-forward validation on each expert individually, on data the regime classifier never saw.

What to Do Today

Open any ticker in your portfolio, click the Strategy tab, and scroll to the regime-aware selection panel. You will see the current classified regime, the probability vector, and the weighted blend the platform would apply right now. If the regime is uncertain, probabilities near-equal across two or three states, prefer baseline. If the regime is decisive and persistent, soft MoE gives you most of the edge with less transition risk than hard switching.

Regimes change. Your rules should too. The math for doing that responsibly exists, the platform runs it every night, and the result is a leaderboard that reflects the market you are actually trading, not the market your backtest wishes you were trading.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Related reading

The AI Copilot: Ask Your Portfolio a Question

How Alphactor's AI Copilot turns natural language questions into data-driven portfolio insights, grounded in your actual holdings and market data.

Why Most Backtests Lie

How Alphactor's 8-layer credibility pipeline catches overfitting, data snooping, and curve-fitted strategies before they cost you money.

Breakout Strategies

A systematic look at breakout trading across 500 stocks over 10 years, with real numbers on win rates, expectancy, and the filters that separate signal from…

How to Build a Watchlist That Beats the Headlines

A practical approach to screening stocks, defining what criteria actually matter, and avoiding the FOMO trap of chasing news-driven momentum.

Market Regime on the Chart

Regimes change discretely, but regime models detect them in near-real-time. The Market Regime overlay annotates where the regime flipped so you can see…

Cockpit Cards: Quick-Glance Intelligence per Stock

How cockpit cards surface the signals, events, and changes that matter most across your watchlist and portfolio without information overload.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free