Return on Equity (ROE)

Net income divided by shareholders' equity, how productively a business uses its own capital.

`ROE = Net income / Shareholders' equity`. DuPont decomposition breaks it into three drivers: `ROE = Net margin × Asset turnover × Equity multiplier (leverage)`.

Why it matters. Sustained ROE above 15–20% is one of the strongest quantitative signatures of a durable competitive advantage. High ROE plus low leverage typically indicates genuine pricing power; high ROE driven by leverage is a different story.

Pitfalls. Buybacks mechanically shrink equity and lift ROE without improving the operating business. Equity made small by past write-offs can distort the ratio. Cross-check ROE against ROIC (which isn't distorted by capital structure) for a cleaner signal.

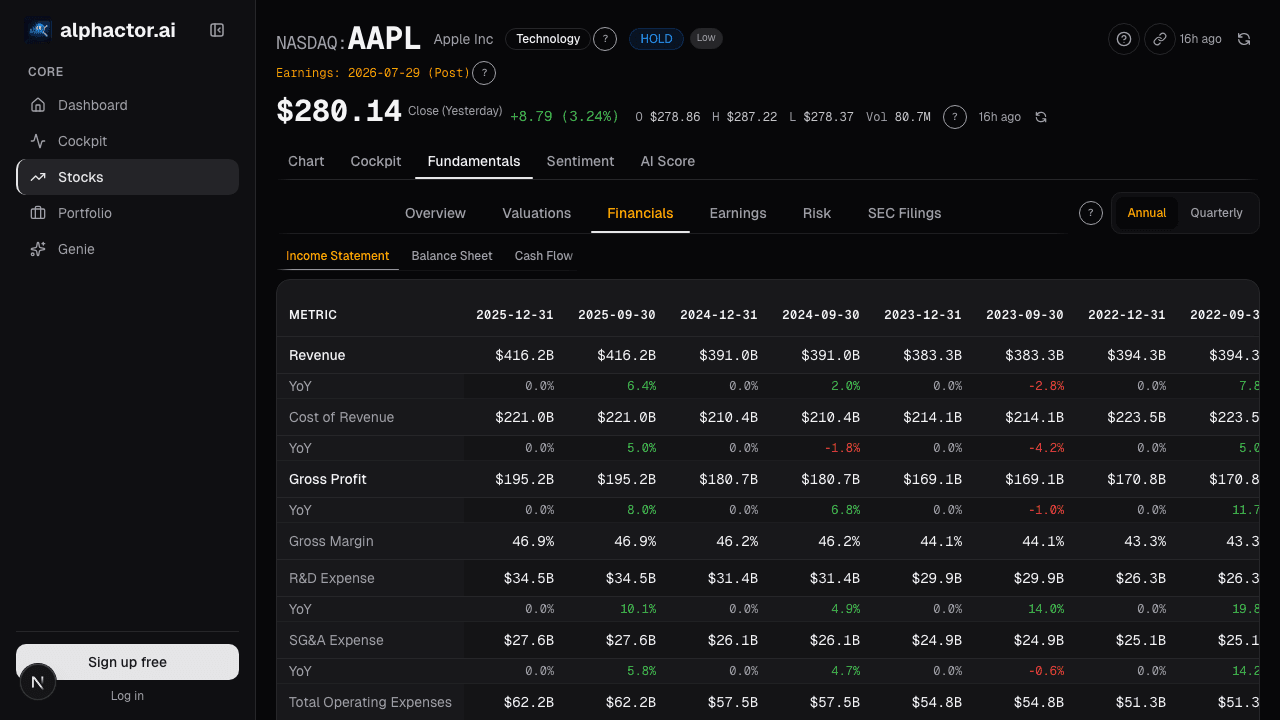

See it applied

Related reading

- Accruals Quality: How to Spot Earnings That Aren't Real

Accruals measure the gap between reported earnings and actual cash. Widening accruals is one of the most reliable red flags in financial analysis, Sloan's…

- Piotroski F-Score

Piotroski's 9 tests filter the value quintile for fundamental improvement. F-scores of 8-9 produced a 72% forward win rate; scores of 0-3 produced only 15%.

- Return on Equity

How to use ROE to identify high-quality businesses, why the DuPont decomposition matters, and the leverage trap that inflates the metric.