Economic Moat

A structural advantage that protects a firm's long-run economic profit from competition.

Popularised by Warren Buffett and formalised by Morningstar, a moat is a durable barrier that lets a company sustain returns on capital above its cost of capital. The five canonical moat sources are:

- Intangible assets (brands, patents, licences)

- Switching costs (enterprise software, payment rails)

- Network effects (marketplaces, social graphs)

- Cost advantages (scale, process, unique access)

- Efficient scale (rational oligopolies in bounded markets)

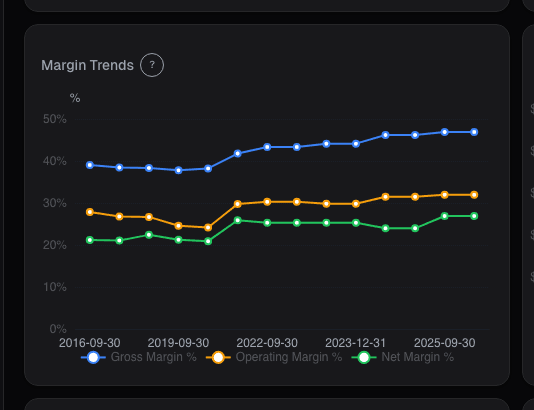

Why it matters. A DCF's long-range growth and margin assumptions only hold if the competitive moat is deep enough. Without a moat, ROIC mean-reverts to the cost of capital, and intrinsic value collapses. Moat analysis is where the *quality* of a compounding estimate is made or broken.

Pitfalls. Moats erode, Kodak, Nokia, Blockbuster. Monitor moat signals (pricing power, share stability, customer churn) every quarter; do not assume yesterday's moat is still intact.

See it applied

Related reading

- Accruals Quality: How to Spot Earnings That Aren't Real

Accruals measure the gap between reported earnings and actual cash. Widening accruals is one of the most reliable red flags in financial analysis, Sloan's…

- Piotroski F-Score

Piotroski's 9 tests filter the value quintile for fundamental improvement. F-scores of 8-9 produced a 72% forward win rate; scores of 0-3 produced only 15%.

- Return on Equity

How to use ROE to identify high-quality businesses, why the DuPont decomposition matters, and the leverage trap that inflates the metric.