Earnings Power Value (EPV)

A valuation method that uses current sustainable earnings and zero growth to estimate a conservative fair value.

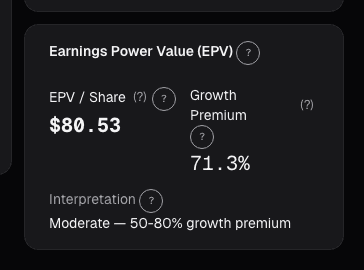

Earnings Power Value, popularised by Columbia's Bruce Greenwald, values a business on normalised current earnings only, it assumes the company never grows. Unlike a DCF, there is no dependence on long-range growth forecasts, which makes EPV a useful *lower-bound* estimate.

Formula. `EPV = Normalised earnings × (1 − tax rate) / cost of capital + non-operating assets − debt`.

Why it matters. Compare EPV to a firm's market cap: a market cap well below EPV implies either the market is underpricing today's earnings or there is a structural reason to expect decline. A market cap well above EPV means the market is paying for growth, a DCF can then quantify whether that growth assumption is reasonable.

Pitfalls. Normalising earnings is the hard part. Use 5- to 10-year averages for margin and include maintenance capex, not accounting depreciation. Under-normalised earnings produce EPVs that look like bargains but aren't.

See it applied

Related reading

- EV/Revenue: The Multiple That Survives When Earnings Don't

EV/Revenue survives where P/E breaks, but needs a growth bridge. Pre-profit software mid-cycle runs 0.2-0.4x growth-adjusted, how to avoid the reading traps.

- FCF Yield: What You're Actually Earning Today

FCF yield answers the most basic question in equity investing: if I buy this company today, how much cash does it throw off per dollar?

- Earnings Power Value

EPV asks what a company is worth assuming zero growth, forever. The gap between EPV and market cap is the growth premium.