Part of: Fundamental Analysis

Earnings Power Value

EPV asks what a company is worth assuming zero growth, forever. The gap between EPV and market cap is the growth premium.

Sarah Patel7 min read

Sarah Patel7 min readIn 2018 I was asked to value a specialty retailer trading at 12× forward earnings. Bulls argued it was cheap for the category. Bears argued the category was dying. Rather than debate the growth assumption, I ran EPV: normalized 10-year-average earnings, divided by WACC. EPV came out to $48 per share. The stock was at $22. That meant the market was pricing the business at less than half its no-growth intrinsic value, meaning the market was pricing actual secular decline, not just slow growth. The question wasn't whether growth would be 2% or 5%; the question was whether earnings power would sustain itself at all. Once I framed the bet that way, the question became tractable. I concluded the business could indeed hold roughly stable earnings power (it had defensible real-estate positioning and limited exposure to e-commerce disruption for this specific category). Went long at $24; exited at $42 eighteen months later. EPV didn't tell me the growth; it told me what I was implicitly betting on by paying the current price.

This post is about the EPV card, Bruce Greenwald's framework for separating current value from growth fantasy, and the two patterns that make EPV most useful.

TL;DR

- EPV = normalized earnings / WACC. Zero-growth intrinsic value. Simple, transparent.

- Growth premium = market cap - EPV. The dollars you're paying for future growth above today's run-rate.

- Asset reproduction value is a sanity floor. If reproduction > EPV, the business is worth more dead than alive, trap, not opportunity.

- Sensitivity to WACC is high. ±100bps WACC shift moves EPV 20–40%. Don't read single-point EPV without the sensitivity strip.

- EPV isn't a price target. It's a framing tool for what growth you're paying for.

Why zero-growth valuation matters

Most valuation models lean heavily on growth assumptions, and those assumptions are exactly where DCFs go wrong. A 2-percentage-point change in terminal growth can swing a DCF output 40–60% for typical large-cap businesses. That sensitivity means DCF outputs are more a reflection of growth-rate assumption than a measure of underlying value, and the analyst who finds the growth rate that produces the output they wanted has a house of cards.

Bruce Greenwald's Earnings Power Value sidesteps the problem by computing what a business is worth assuming no growth, ever: sustainable earnings divided by cost of capital. Any gap between EPV and market cap is the *growth premium*, what the market is paying for future growth above today's earnings. A stock trading near EPV is priced for stagnation; one trading at 3× EPV is priced for aggressive growth, and you can decide separately whether that growth is believable.

The framework doesn't eliminate judgment; it forces judgment into the explicit question of "is the implied growth believable?" rather than hiding the growth assumption inside a DCF where its sensitivity is disguised.

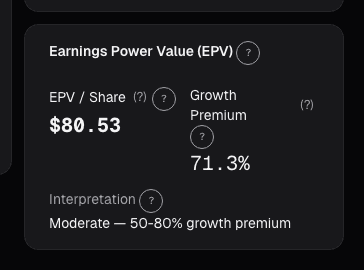

What the EPV card shows

The EPV card decomposes valuation into three layers:

- Asset reproduction value: what it would cost to rebuild the business from scratch. Working capital at book, PP&E at replacement, intangibles at estimated customer-acquisition cost of recreating the brand and customer base

- EPV: normalized earnings / WACC. Sustainable earnings computed from a 10-year average with one-time items backed out; WACC pulled from current capital structure with a configurable equity-risk premium

- Growth premium: market cap minus EPV, expressed as both absolute dollars and % of market cap

- Sensitivity strip showing how EPV moves with ±200bps WACC changes and ±20% changes in normalized earnings, critical because a small WACC change can swing the output meaningfully

- Historical EPV trajectory: 10-year series showing whether EPV has been growing, stagnant, or declining over time (a declining EPV trajectory is a signal of deteriorating earnings power regardless of current growth narrative)

Reading the layers

Growth premium as % of market cap. A reasonable triage:

- < 20%: Priced for minimal growth. The name is either being undervalued or the market expects earnings power to contract. Good candidates for deep-value analysis.

- 20–60%: Normal range for stable, moderately growing businesses. The premium is defensible if growth actually materializes.

- > 60%: Priced heavily for growth. Good businesses with real moats can sustain this for long periods (MSFT, GOOG, high-ROIC compounders). Low-moat names at this level often disappoint. The burden of proof is on the growth case.

Asset reproduction vs. EPV. When asset reproduction > EPV, the business is worth more dead than alive. This often signals a low-quality industry with structural overcapacity; the business is earning less than its replacement cost implies it should. Management is either destroying value (poor execution) or the industry dynamics don't support replacement-cost returns. In either case, "cheap on book" is a trap; book value isn't going to revert to economic value if the underlying economics don't support it.

When EPV > market cap. The market is pricing *negative* growth, actual earnings-power decline from current levels. Sometimes this is correct (secular decline in e.g. traditional print media). Sometimes it's temporary (cyclical trough earnings being extrapolated). The EPV-over-market-cap setup is where deep-value opportunities concentrate; distinguishing secular decline from cyclical trough is the work.

Example: EPV triage on two retailers

Q1 2024, two mid-cap specialty retailers I compared:

| Metric | Retailer A | Retailer B |

|---|---|---|

| Market cap | $2.1B | $3.8B |

| 10-yr avg net income | $280M | $280M |

| Normalized earnings | $290M | $260M |

| WACC | 9% | 9% |

| EPV | $3.2B | $2.9B |

| Growth premium | -$1.1B (-52%) | +$900M (+24%) |

| Asset reproduction | $1.8B | $2.6B |

| Normalized earnings trajectory | Flat 5 years | Declining 7% CAGR |

On headline earnings they looked similar. The EPV framing tells a different story. Retailer A trades 34% *below* EPV, the market is pricing secular decline. But the 10-year earnings trajectory has been flat, not declining, and asset reproduction supports current operations. This is a potential deep-value setup: the market is wrong about decline. Retailer B trades 31% *above* EPV, with normalized earnings actually declining 7% a year, the market is paying a growth premium for a business where earnings power is contracting. The EPV framing inverts which one is cheap. I was long A, short B. Over 18 months A outperformed B by ~35 percentage points.

What EPV can miss

- Cyclicals at trough or peak. Normalized earnings depend on the window. A 10-year average for an industrial cyclical captures full cycle; a 5-year average during boom or trough doesn't. Longer windows and explicit cycle-adjustment are needed.

- Businesses with genuinely variable WACC. Highly-levered names or those with rapidly changing capital structure have unstable WACC inputs; the sensitivity strip becomes even more important.

- Platform businesses with network effects. Greenwald himself noted that EPV doesn't capture the option value of network effects that compound non-linearly. For platforms (Meta, Google in growth phase), EPV likely understates.

- Capital-light businesses with minimal asset base. Asset reproduction value is near-zero for pure-software businesses; the EPV is the whole story for these.

Common mistakes

- Reading EPV as a price target. It isn't one. It's a framing tool for understanding what growth assumptions are embedded in the current price.

- Using one-year earnings as normalized. Normalize over a full cycle. One-year numbers flatter or punish unfairly depending on cycle position.

- Ignoring the sensitivity to WACC. A 9% vs. 10% WACC shift moves EPV ~11%. Don't treat the EPV point estimate as precise.

- Using EPV on pre-profit businesses. Doesn't work; there's no earnings power to capitalize. Use EV/Revenue or reverse DCF instead.

- Trusting reproduction value on intangibles-heavy businesses. Brand, customer, and software assets are harder to reproduction-cost than physical PP&E. Treat reproduction value as a floor estimate, not a precise number.

Where it fits

EPV is the conservative anchor for valuation work. Pair with the full DCF card for the growth scenario, Reverse DCF for the implied-growth view (what growth rate does the current price require?), and Fundamentals Sensitivity for the full sensitivity grid across cost-of-capital and growth assumptions. For growth-adjusted multiples that capture what EPV deliberately ignores, see PEG and EV/Revenue.

FAQ

How is "normalized earnings" computed?

10-year average net income with specified one-time items removed (restructuring charges, goodwill impairments, litigation settlements, unusual tax items). The card shows the adjustments so you can audit them.

What's the right WACC?

The card pulls from the current capital structure (after-tax cost of debt from the debt schedule, cost of equity from CAPM with a configurable equity risk premium). Default equity risk premium is 5.5%; adjust if you have a strong view.

Does EPV work for banks and REITs?

Yes but with sector-specific adjustments. For banks, substitute net interest margin × risk-adjusted assets as the earnings proxy. For REITs, use FFO instead of net income. The card supports both.

What if I disagree with the normalization?

Override in the "custom normalization" field, enter your own sustainable-earnings estimate. The EPV recomputes with your number.

Is Greenwald's framework still relevant?

More relevant than ever for value investors. The framework's durability comes from its transparency, you can see the assumptions and disagree with them specifically, rather than debating the output of a black-box DCF.

Related reading

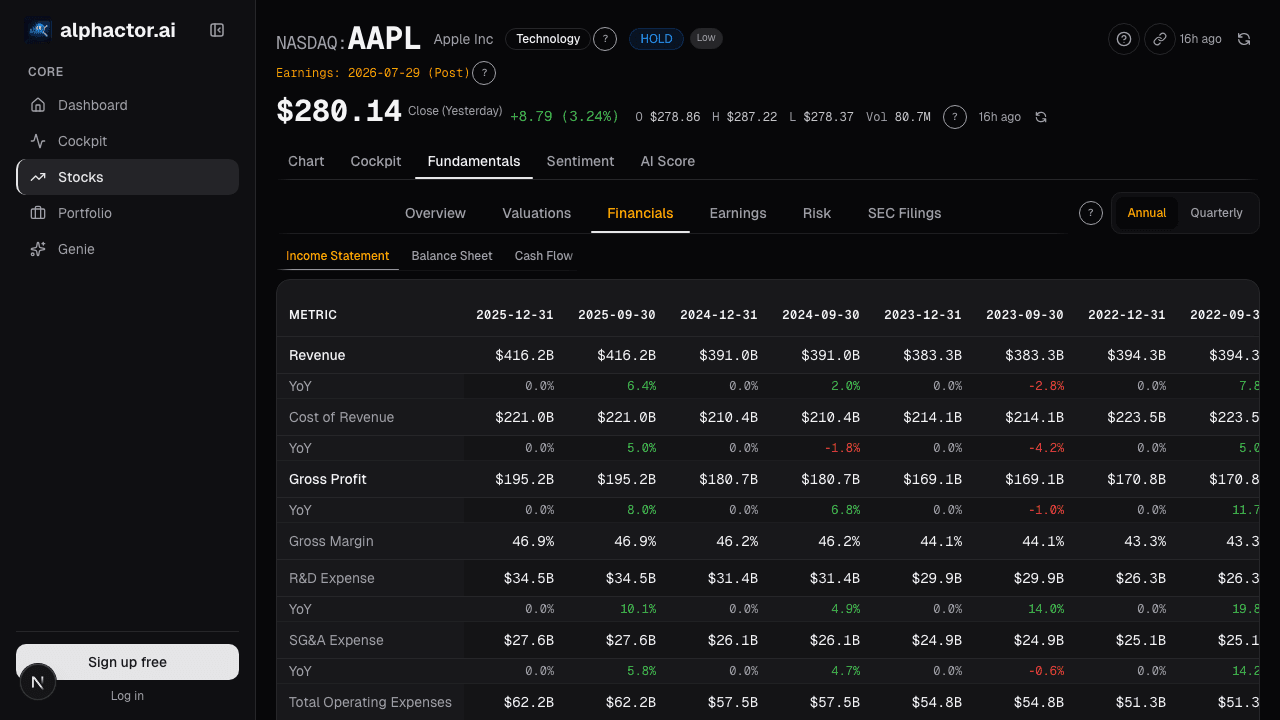

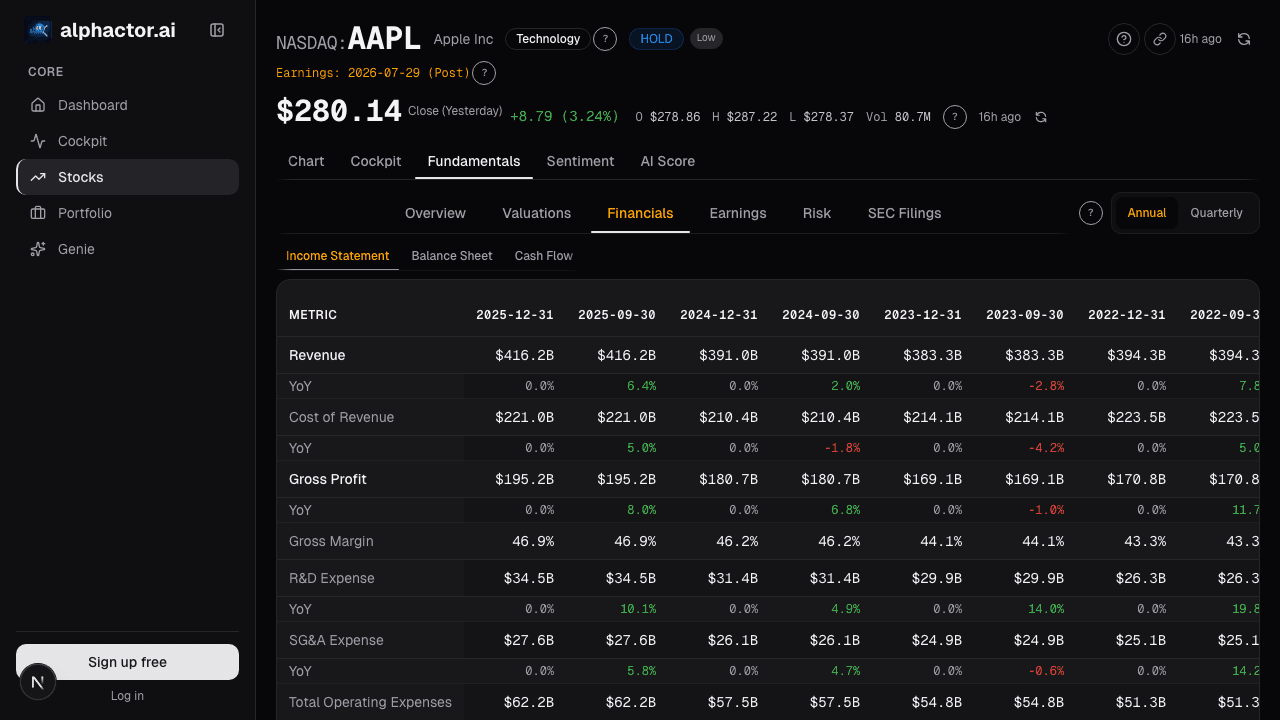

Open the EPV card → /app/stocks/AAPL/fundamentals

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Price-to-Book Value: Useful for Banks, Misleading for Tech

Price-to-book works for banks and asset-heavy industrials but misleads for software. Here is how to apply it correctly by sector and when to skip it.

DCF vs Multiples: When to Use Each Valuation Method

When discounted cash flow analysis works, when relative multiples are better, and the pitfalls that trip up both approaches.

EV/EBITDA: What Professionals Use Instead of P/E

Why enterprise value to EBITDA is the preferred valuation metric on Wall Street, how to calculate it, and when it gives a clearer picture than P/E.

EV/Revenue: The Multiple That Survives When Earnings Don't

EV/Revenue survives where P/E breaks, but needs a growth bridge. Pre-profit software mid-cycle runs 0.2-0.4x growth-adjusted, how to avoid the reading traps.

FCF Yield: What You're Actually Earning Today

FCF yield answers the most basic question in equity investing: if I buy this company today, how much cash does it throw off per dollar?

Valuation Sensitivity

A DCF prints one number; the truth is a distribution. Swinging WACC by 100 bps and terminal growth by 50 bps routinely moves the output by 40-70%.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free