How to Backtest a Trading Strategy (The Right Way)

Learn how to properly backtest trading strategies, avoid common pitfalls like overfitting, and use statistical credibility testing to validate your results.

Marcus Chen3 min read

Marcus Chen3 min readWhy Most Backtests Lie

Every backtesting tool will show you a strategy that works on historical data. The problem is that most of those strategies fail the moment real money is on the line. The gap between a beautiful equity curve and actual trading performance comes down to one concept that most platforms ignore: statistical credibility.

Backtesting, at its core, is running a set of trading rules against historical price data to see how they would have performed. Buy when RSI drops below 30, sell when it crosses 70. Simple enough. But the devil is in the details, and the details are where most traders get burned.

The Overfitting Trap

The most common mistake in backtesting is overfitting. You tweak parameters until the backtest looks perfect on past data, but those parameters are tuned to noise, not signal. A strategy with 14 parameters that returns 200% annually on 2020-2024 data probably learned the quirks of that specific time period, not a real edge.

Signs your strategy is overfit:

- It has many parameters relative to the number of trades

- Performance degrades sharply on out-of-sample data

- Small parameter changes cause large performance swings

- It works on one ticker but fails on similar stocks

Look-Ahead Bias and Survivorship Bias

Two other silent killers lurk in backtests. Look-ahead bias happens when your strategy uses information that would not have been available at the time of the trade. Using adjusted close prices, referencing future earnings dates, or computing indicators on the full dataset before splitting into train/test sets are all forms of look-ahead bias.

Survivorship bias means only testing on stocks that still exist today. If you backtest a momentum strategy on the current S&P 500, you are ignoring every company that went bankrupt or was delisted. The survivors naturally look better.

What Statistical Credibility Testing Actually Means

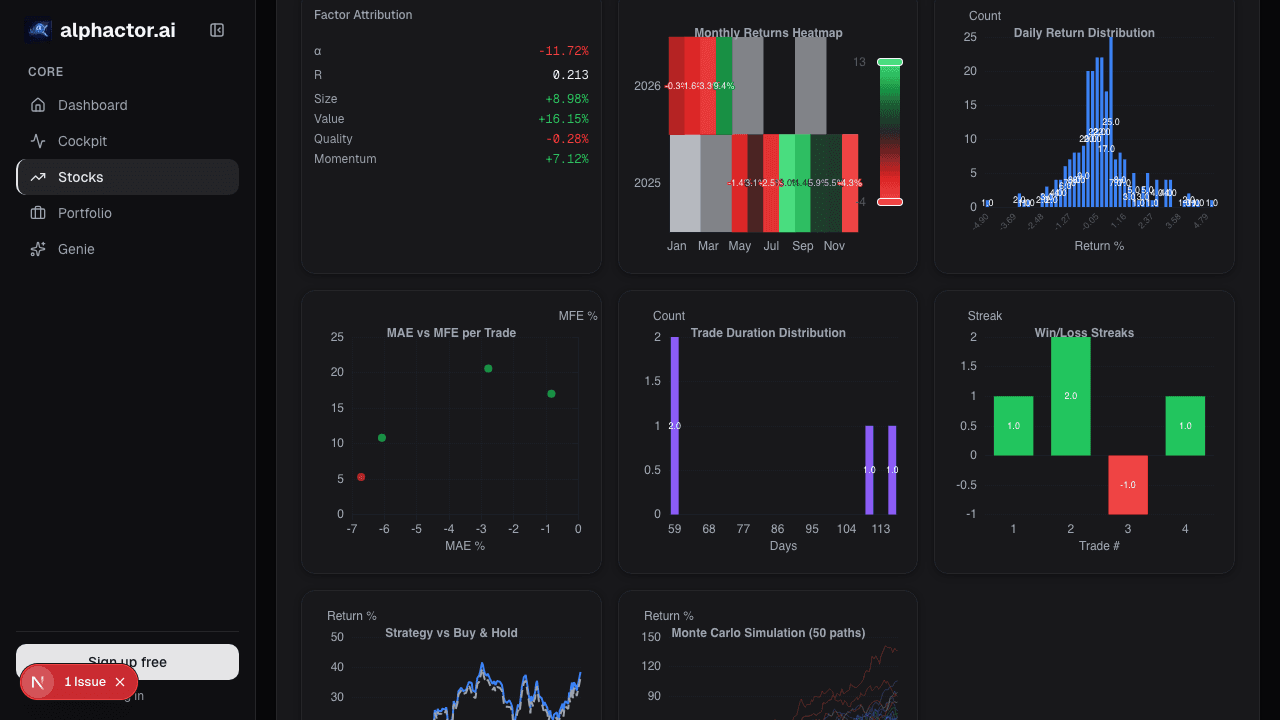

A credible backtest answers a harder question: Would this strategy have performed well even if history had played out differently? This is where Monte Carlo simulation and distributional analysis come in.

Instead of looking at a single equity curve, credibility testing generates thousands of possible outcomes by resampling trades, shuffling return sequences, and stress-testing assumptions. If your strategy holds up across the majority of simulated paths, you have evidence of a real edge.

Alphactor's 8-layer credibility pipeline in Alphactor backtesting goes further:

- Deflated Sharpe Ratio (DSR) adjusts for the number of strategies you tested, correcting for data-snooping bias

- Monte Carlo simulation resamples trade sequences to build confidence intervals around returns

- Walk-forward validation tests the strategy on rolling out-of-sample windows, not just a single train/test split

- Regime detection checks whether the strategy works across different market conditions (bull, bear, high-volatility, low-volatility)

- Drawdown analysis measures worst-case scenarios and recovery times

- Parameter stability verifies that nearby parameter values produce similar results, catching overfitting

A Practical Backtesting Workflow

Here is a workflow that actually produces reliable results:

- Start with a hypothesis, not a parameter search. "Momentum works in large-cap tech" is a hypothesis. "What RSI/MACD combo maximizes returns?" is a fishing expedition.

- Use walk-forward testing instead of a single train/test split. Roll your out-of-sample window forward in time to simulate real deployment.

- Keep parameters minimal. Fewer moving parts means less room for overfitting. If you can not explain each parameter's role in one sentence, you probably do not need it.

- Test across tickers and time periods. A strategy that only works on AAPL in 2023 is not a strategy. It is a coincidence.

- Check the credibility score before risking capital. On Alphactor, a strategy needs to pass all six credibility layers to earn a high confidence rating.

The Bottom Line

Backtesting is not about finding a strategy that would have made money. It is about finding a strategy that has statistically credible evidence of an edge that persists across market conditions. The difference between the two is the difference between gambling and investing.

If your current backtesting tool does not tell you whether your results are statistically significant, you are flying blind. A high return on a backtest means nothing without credibility validation to back it up. Start free and run your first credibility-validated backtest today.

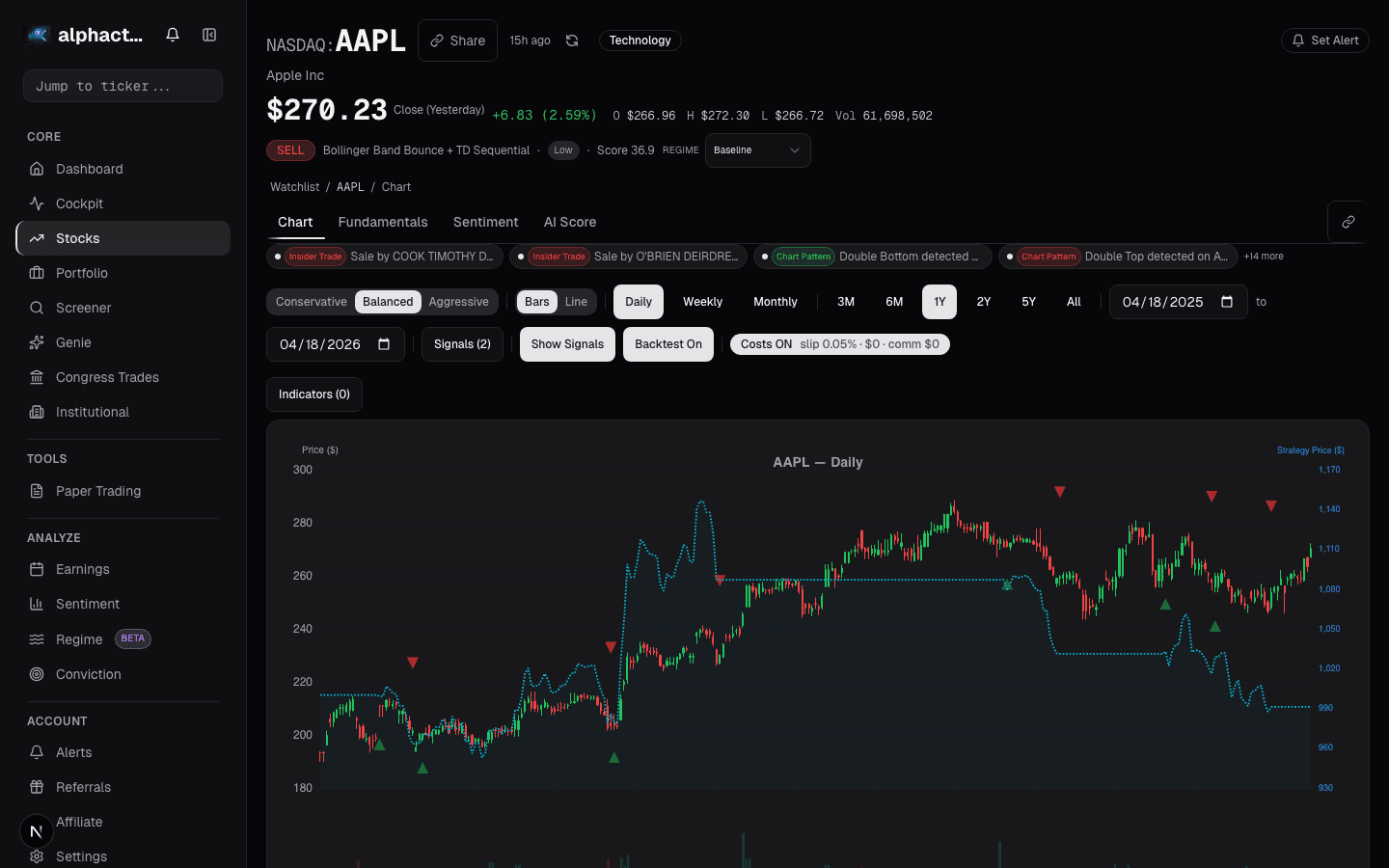

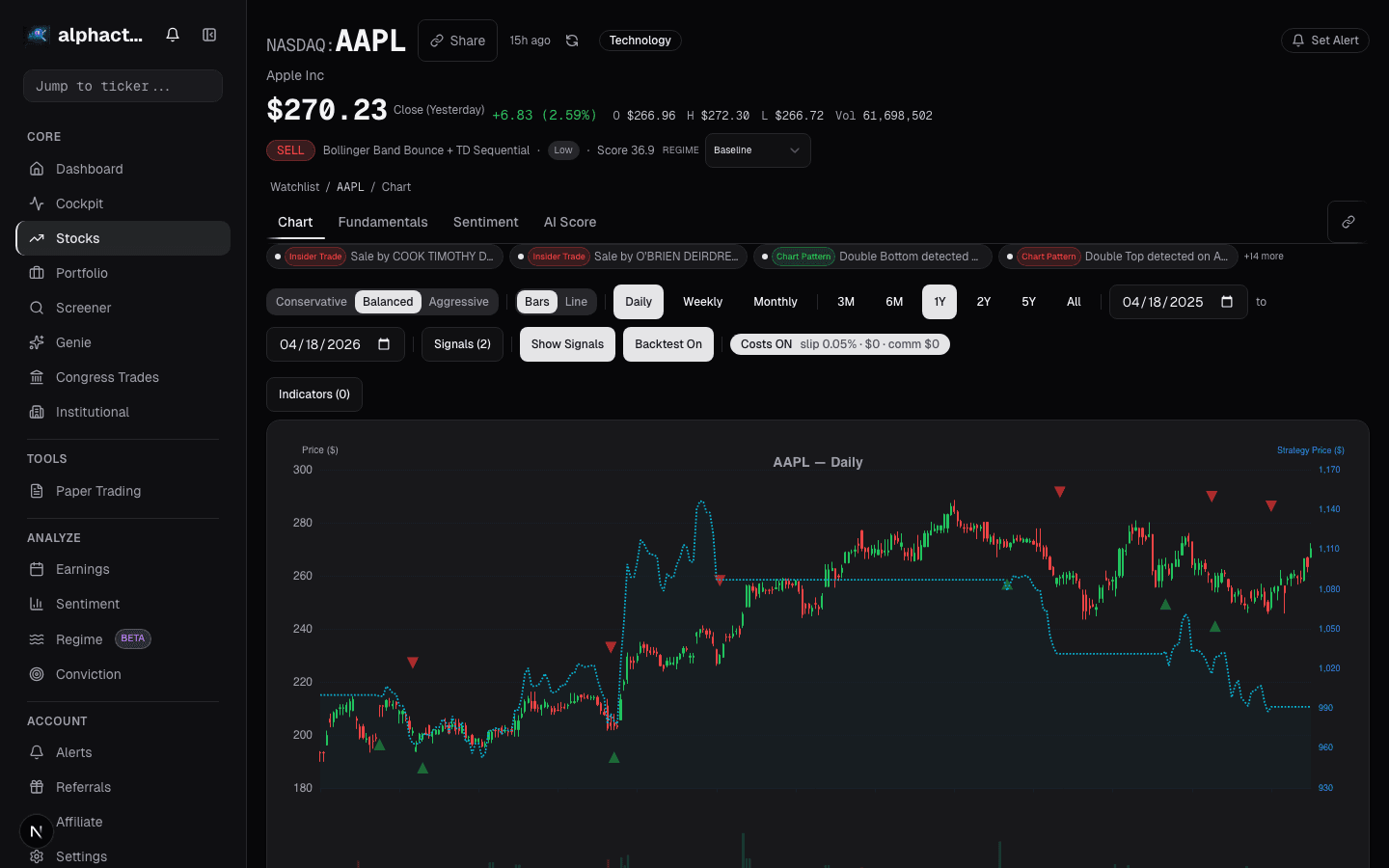

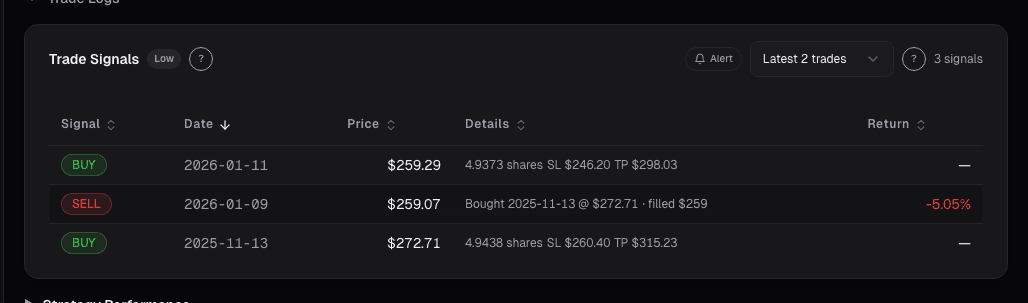

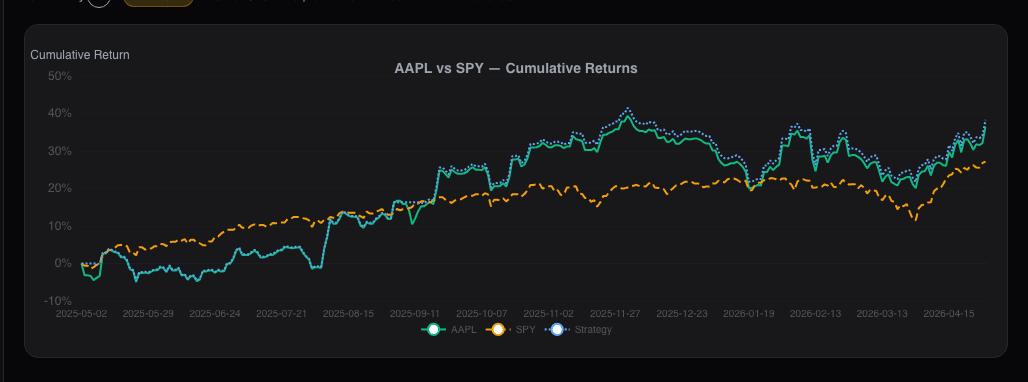

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Why Most Backtests Lie

How Alphactor's 8-layer credibility pipeline catches overfitting, data snooping, and curve-fitted strategies before they cost you money.

Breakout Strategies

A systematic look at breakout trading across 500 stocks over 10 years, with real numbers on win rates, expectancy, and the filters that separate signal from…

A Mean Reversion Strategy That Survived Walk-Forward

How a 2-period RSI mean reversion strategy on the S&P 500 held up across 15 years of walk-forward validation, and what the numbers actually look like.

Combining Multiple Signals Into One Strategy

How to merge momentum, value, and quality signals into a single composite score that survives walk-forward testing, with practical rules to avoid the…

Regime-Aware Strategy Selection

Markets cycle through trends, ranges, and shocks. Learn how regime detection drives which strategy runs, and why a mixture of experts beats a single static…

Your Trading Signals Have a Noise Problem

Why most trading signals fire too often to be useful, and how to filter with multiple timeframes, volume confirmation, and market regime awareness.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free