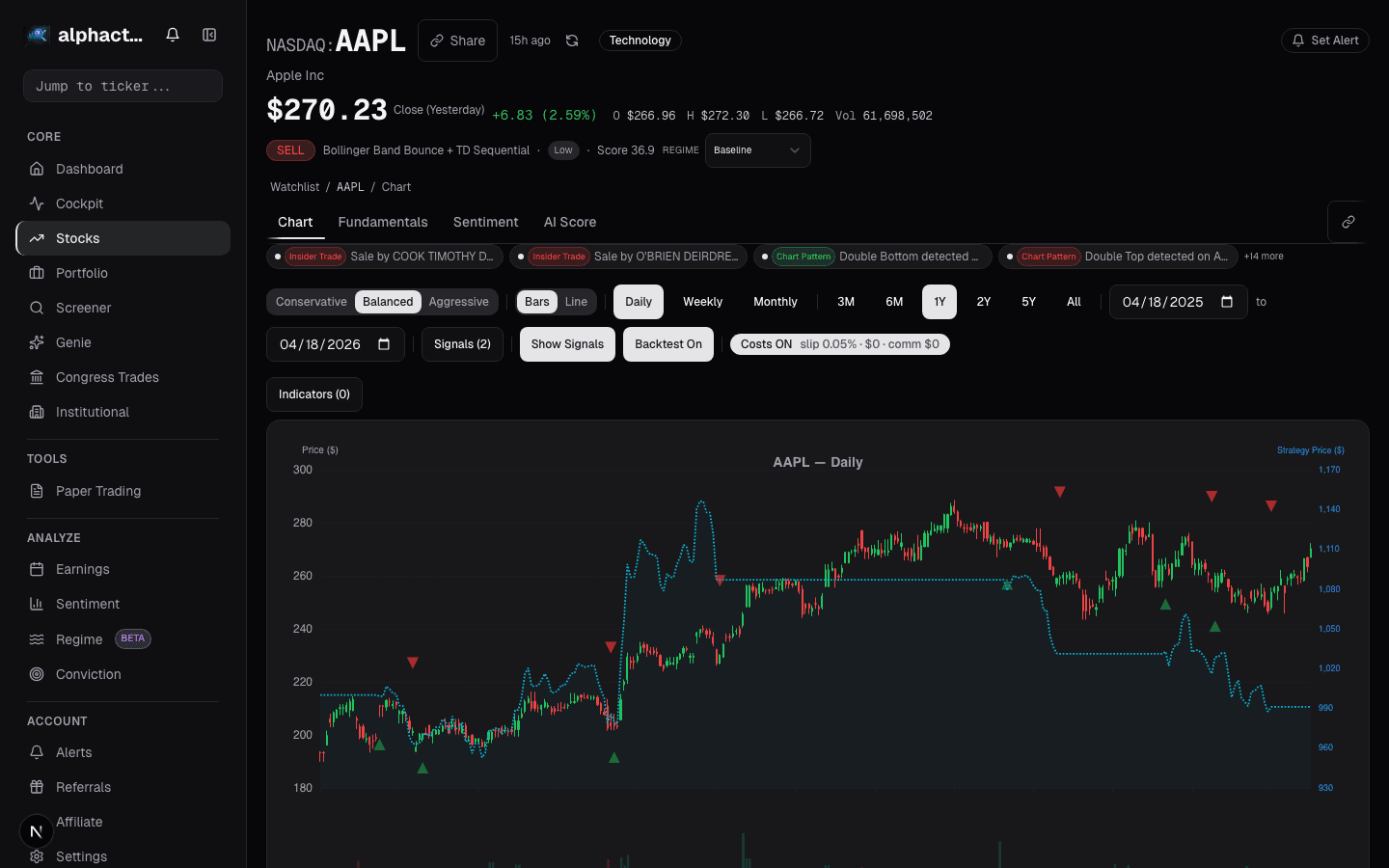

Part of: Technical Analysis

Combining Multiple Signals Into One Strategy

How to merge momentum, value, and quality signals into a single composite score that survives walk-forward testing, with practical rules to avoid the…

Marcus Chen4 min read

Marcus Chen4 min readThe Case for Multiple Signals

Single-signal strategies have a fundamental weakness: every signal goes through periods where it stops working. Value underperformed for nearly a decade from 2010-2020. Momentum crashed violently in March 2009 and again in November 2020 when the Pfizer vaccine announcement triggered a sudden rotation. Quality lags during speculative manias when low-quality, high-beta stocks lead.

Combining signals into a composite score reduces this regime dependency. If value is struggling but momentum and quality are both contributing, the portfolio stays on track. The math is straightforward: uncorrelated alpha sources, when combined, produce a higher Sharpe ratio than any individual source.

The danger is equally straightforward: every additional signal is an additional degree of freedom. Combine enough signals and you can fit any historical dataset perfectly. The strategy will look flawless in a backtest and collapse in live trading. The discipline is in how you combine signals, not how many you use.

A Three-Signal Composite

We built a composite stock ranking using three well-documented signals:

- Momentum: 12-month return, skipping the most recent month. Ranked across the universe, normalized to a 0-100 percentile score.

- Value: Earnings yield (inverse of P/E, using trailing 12-month earnings). Ranked and normalized identically.

- Quality: Return on equity (trailing 12 months). Ranked and normalized.

Each stock receives three percentile scores. The composite score is the simple average of the three. No optimization of weights. No interaction terms. No conditional logic. Equal weighting is the deliberate default because it introduces zero additional parameters.

Why Equal Weights

Research from DeMiguel, Garlappi, and Uppal (2009) demonstrated that equal-weight portfolios frequently outperform optimized portfolios out of sample, because estimation error in the optimization inputs exceeds the theoretical benefit. The same logic applies to signal combination.

We tested this directly. Optimized weights (fitted on 2004-2014) produced a CAGR of 16.1% in sample and 9.8% out of sample (2015-2024). Equal weights produced 13.7% in sample and 12.4% out of sample. The equal-weight approach underperformed in sample by 2.4% but outperformed out of sample by 2.6%. This is the textbook signature of overfitting.

Backtest Results

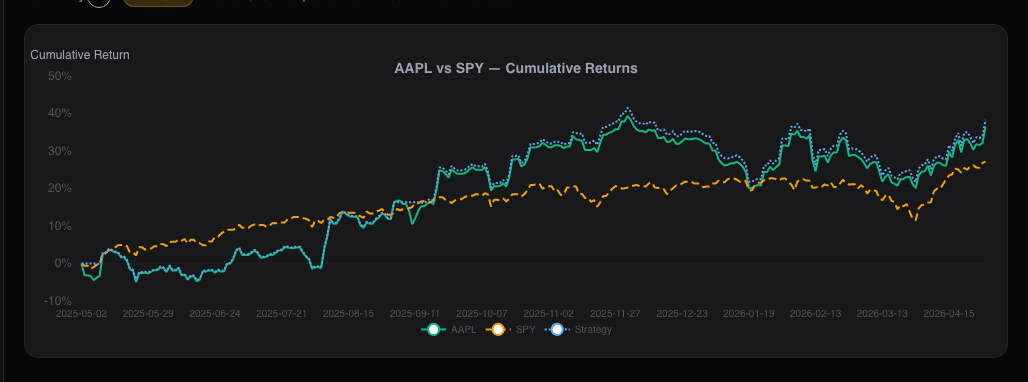

We applied the equal-weight composite score to the Russell 1000 universe, holding the top 50 stocks, rebalancing monthly, from January 2004 through December 2024:

- CAGR: 13.1%

- Maximum drawdown: -39.7%

- Sharpe ratio: 0.78

- Information ratio vs. Russell 1000: 0.41

- Annual turnover: 142%

For comparison, single-signal strategies over the same period:

- Momentum only: CAGR 11.4%, max drawdown -52.3%, Sharpe 0.58

- Value only: CAGR 9.2%, max drawdown -58.1%, Sharpe 0.42

- Quality only: CAGR 10.8%, max drawdown -41.2%, Sharpe 0.63

The composite outperformed all three individual signals on both absolute return and risk-adjusted return. The drawdown improvement over momentum-only and value-only was substantial. This is the diversification benefit at work: the signals have low correlation with each other (momentum-value correlation is approximately -0.30), so their drawdowns rarely coincide.

Walk-Forward Validation

We ran walk-forward testing via Alphactor backtesting with 60-month in-sample windows and 12-month out-of-sample windows, rolled annually. Results across 16 out-of-sample periods:

- Walk-forward efficiency ratio: 0.79

- Profitable periods: 13 of 16 (81%)

- Out-of-sample CAGR: 11.8%

- Out-of-sample max drawdown: -41.3%

The efficiency ratio of 0.79 is strong, and the 81% profitable-period rate gives confidence that the composite captures a genuine multi-factor premium. The three losing periods (2008, 2018 Q4, 2022) were all broad market declines where even diversified long-only strategies struggled.

Rules for Adding Signals

When you are tempted to add a fourth, fifth, or sixth signal, apply these constraints:

- Independent academic evidence. Published in a peer-reviewed journal, replicated across markets, with an economic rationale for persistence.

- Low correlation with existing signals. A signal that correlates at 0.7 with momentum adds noise without diversification. Require pairwise correlation below 0.30.

- Marginal improvement must survive walk-forward testing. If the efficiency ratio does not improve after adding the signal, it is not earning its parameter budget.

- Equal weights unless overwhelming evidence otherwise. "Overwhelming" means optimized weights are stable across multiple non-overlapping time periods.

Parameter Budget

Think of each signal as spending from a finite budget. You need roughly 10 years of data per free parameter. A three-signal strategy with equal weights has three parameters; twenty years of data gives reasonable confidence. A six-signal strategy with optimized weights has twelve parameters and would need 120 years of data.

This is why simplicity matters as a statistical requirement, not an aesthetic preference. Alphactor's credibility pipeline -- part of the Alphactor backtesting suite -- applies the Deflated Sharpe Ratio, adjusting the significance threshold based on parameter count. Strategies with fewer parameters earn higher credibility scores because the evidence is harder to explain by chance.

For most stock selection strategies on U.S. equities, three to four signals is the practical ceiling before overfitting risk dominates the diversification benefit. The goal is not the highest backtest return. It is the highest confidence that the strategy captures a real, persistent edge. That confidence comes from simplicity, independence between signals, and rigorous out-of-sample validation. Browse published multi-signal strategies on the strategy marketplace.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Breakout Strategies

A systematic look at breakout trading across 500 stocks over 10 years, with real numbers on win rates, expectancy, and the filters that separate signal from…

How to Backtest a Trading Strategy (The Right Way)

Learn how to properly backtest trading strategies, avoid common pitfalls like overfitting, and use statistical credibility testing to validate your results.

Mean Reversion Signals: Buying the Dip With Math, Not Hope

How to use z-score, Bollinger %B, and RSI extremes as mean reversion triggers, and why the strategy only works in specific market conditions.

A Mean Reversion Strategy That Survived Walk-Forward

How a 2-period RSI mean reversion strategy on the S&P 500 held up across 15 years of walk-forward validation, and what the numbers actually look like.

Regime-Aware Strategy Selection

Markets cycle through trends, ranges, and shocks. Learn how regime detection drives which strategy runs, and why a mixture of experts beats a single static…

Your Trading Signals Have a Noise Problem

Why most trading signals fire too often to be useful, and how to filter with multiple timeframes, volume confirmation, and market regime awareness.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free