Part of: Risk Management

Risk Parity: Allocating by Risk, Not by Dollars

How risk parity portfolios work, why they differ from traditional allocation, and how to apply the concept without a PhD in finance.

Marcus Chen4 min read

Marcus Chen4 min readThe Problem with 60/40

The traditional 60% stocks, 40% bonds portfolio looks balanced on paper. Sixty cents of every dollar in equities, forty cents in bonds. But it is not balanced at all from a risk perspective.

Equities are roughly three times as volatile as investment-grade bonds. In a 60/40 portfolio, the equity allocation contributes approximately 90% of the total portfolio risk. The bond allocation, despite being 40% of the dollars, contributes only about 10% of the risk. When stocks drop sharply, the bond cushion barely registers.

Risk parity flips this logic. Instead of allocating dollars equally, it allocates risk equally. Each asset class contributes the same amount of portfolio volatility. The result looks very different from traditional portfolios, and it has quietly outperformed them over most multi-decade periods.

How Risk Parity Works

The core idea is straightforward. If stocks are three times as volatile as bonds, you need three times as many bonds (by dollar amount) to equalize risk contributions.

A simplified two-asset example: U.S. stocks at 15% annualized volatility, U.S. Treasury bonds at 5%. To equalize risk, hold roughly 25% stocks and 75% bonds by dollar value. Each asset now contributes approximately 50% of total portfolio risk.

The immediate objection: a 75% bond portfolio will have low returns. This is where risk parity gets creative. Practitioners use modest leverage, typically 1.5x to 2x, to bring overall returns up to equity-like levels while maintaining balanced risk. The argument is that leveraged diversification is more efficient than unlevered concentration.

Why It Has Worked

Risk parity has outperformed traditional 60/40 allocations over most long-term periods, including the 2000-2020 stretch that included two major equity bear markets. The reasons are structural.

Diversification that works. Because each asset class contributes equally to risk, no single market regime dominates the portfolio. A 60/40 portfolio gets crushed when stocks fall. A risk parity portfolio distributes the damage, and the assets contributing more risk during a crisis are smaller positions by design.

Harvesting risk premia broadly. Every major asset class offers a positive expected return over time. Risk parity captures all of these premia efficiently, rather than concentrating in just one.

Volatility drag reduction. A portfolio with lower volatility compounds more efficiently than a higher-volatility portfolio with the same average return. If two portfolios both average 10% but one has 15% volatility and the other 10%, the less volatile portfolio ends up with more money due to reduced volatility drag.

The 2022 Problem

Risk parity's Achilles heel was on full display in 2022. When both stocks and bonds fell simultaneously, the strategy had nowhere to hide. The stock-bond correlation, reliably negative for two decades, flipped positive. Risk parity portfolios suffered their worst year in recent memory.

This does not invalidate the approach, but it is a critical caveat. Risk parity assumes correlations are relatively stable and that at least some assets perform well in any environment. When inflation drives stocks and bonds down together, that assumption breaks.

Applying Risk Parity Principles Without Leverage

You do not need to run a leveraged risk parity fund to benefit from the concept. The core insight, allocate by risk contribution rather than dollar weight, is useful at any scale.

Step 1: Estimate the volatility of each holding. Use trailing 12-month standard deviation as a starting point. A stock with 30% annualized volatility contributes twice the risk of one with 15% volatility, all else equal.

Step 2: Calculate risk contribution. Multiply each position's weight by its volatility. In a two-stock portfolio where Stock A is 50% of the portfolio with 30% volatility, its risk contribution is 15. Stock B at 50% with 15% volatility contributes 7.5. Stock A dominates the risk budget despite equal dollar allocation.

Step 3: Adjust weights. To equalize risk contribution, you would hold less of the volatile stock and more of the stable one. In this example, roughly 33% Stock A and 67% Stock B would equalize risk contributions.

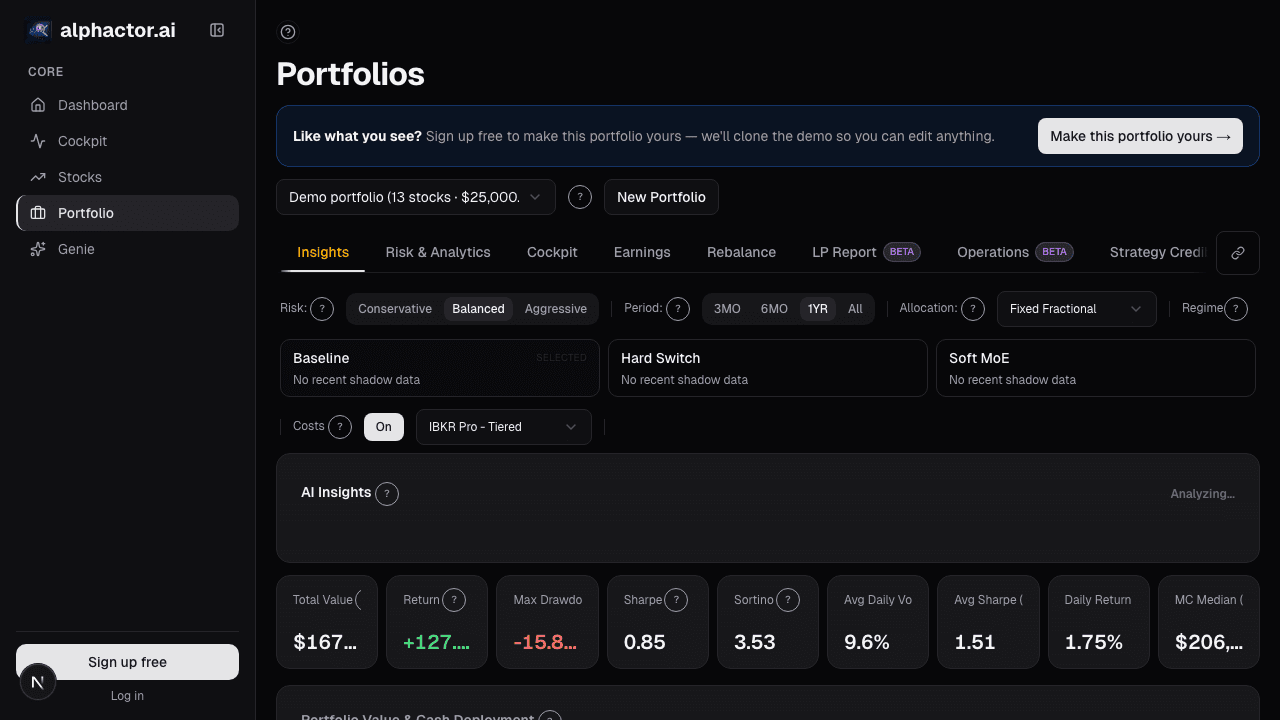

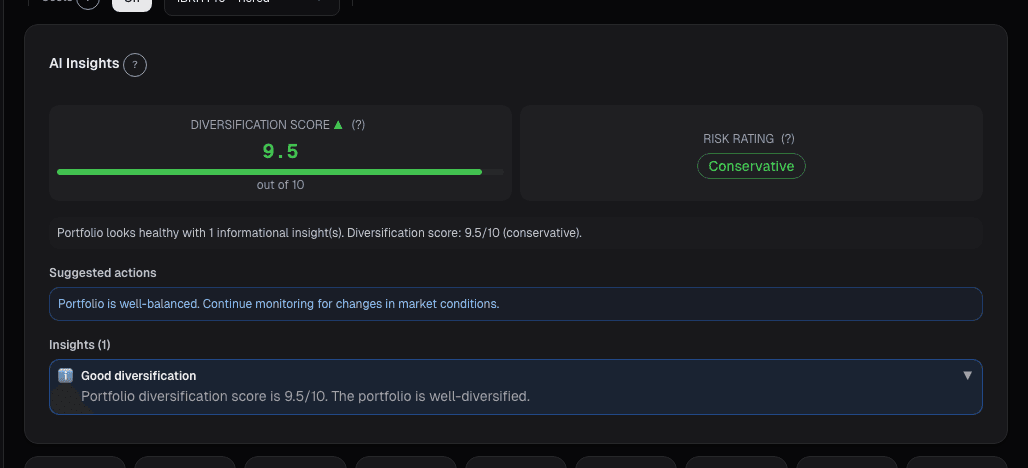

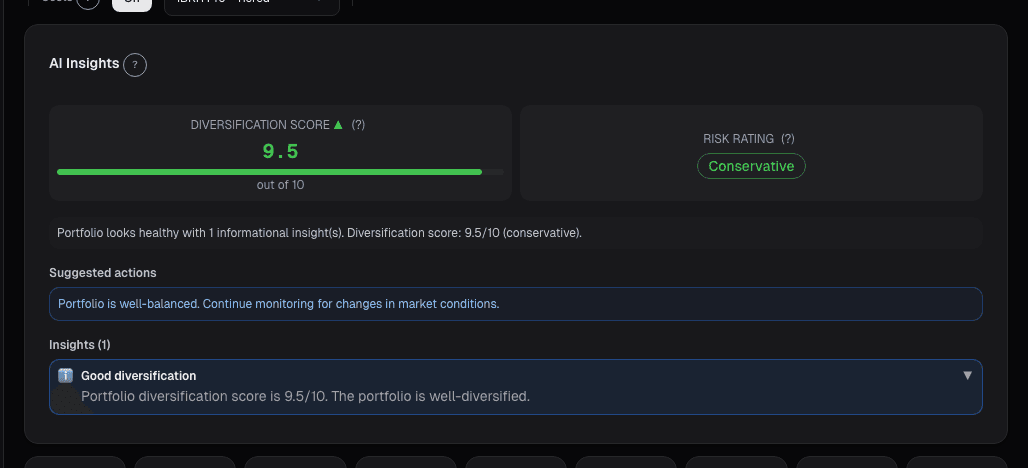

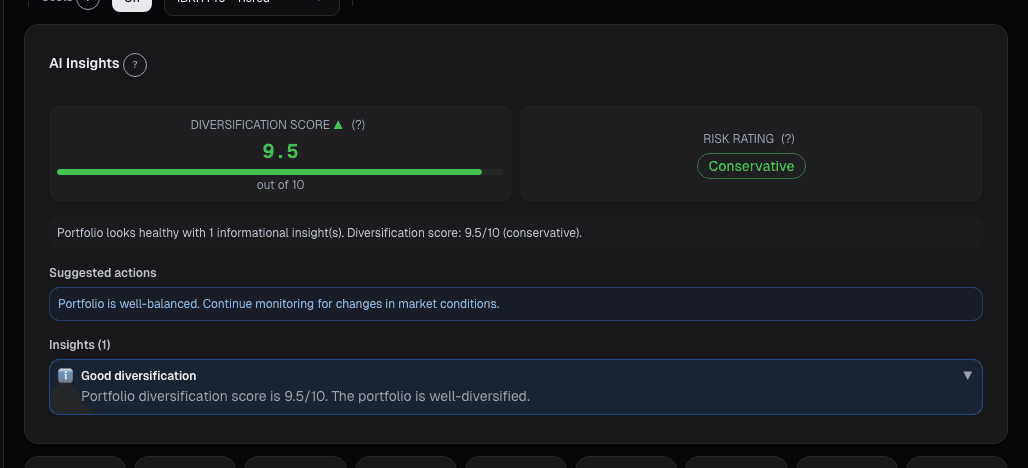

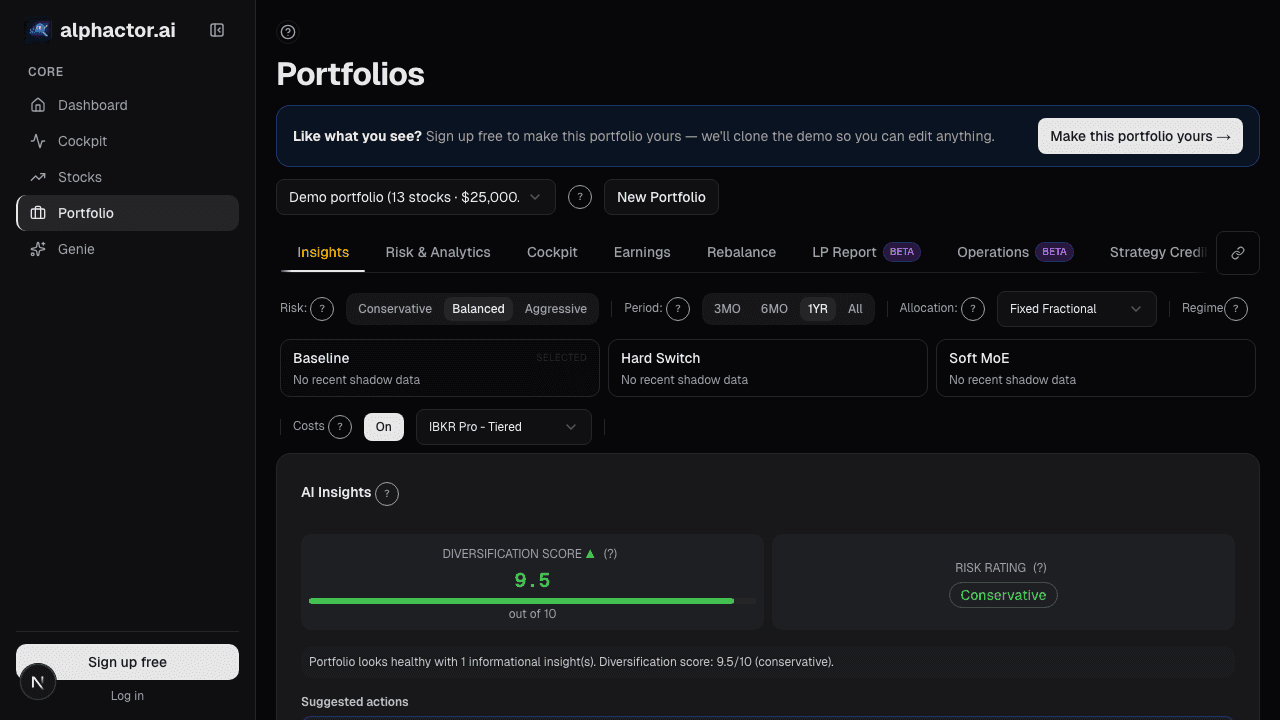

Alphactor's portfolio dashboard automates this calculation across your full portfolio, showing you how much risk each position contributes and suggesting weight adjustments to achieve a more balanced risk profile.

Who Should Consider This Approach

Risk parity principles are most valuable for investors who are building a multi-asset portfolio and want to avoid unintended concentration in equity risk. If your portfolio is 100% individual stocks, the technique still applies at the position level: size volatile positions smaller and stable positions larger.

The approach is less appropriate if you have strong directional views, high conviction in concentrated picks, or a short time horizon. Risk parity is fundamentally agnostic: "I do not know what will work best, so I will balance my bets." If you have conviction, concentration may serve you better.

The Core Takeaway

The dollars in your portfolio are less important than the risk they represent. A position that is 5% of your portfolio but has twice the volatility of everything else is functionally a 10% position from a risk perspective. Thinking in risk units rather than dollar units changes how you size positions, and it almost always leads to better-balanced portfolios.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Related reading

Alt-Data Sentiment at the Portfolio Level

Per-ticker alt-data breaks down past 10 positions. A roll-up of WSB, news, MSPR, and options lets a 90-second scan replace 100 minutes of manual checking.

Portfolio Attribution: Where Your Returns Actually Come From

Beating the benchmark by 400bps feels good until attribution tells you it was all allocation luck on one sector call. Selection vs. allocation vs.

Portfolio Audit Trail: Every Decision

Regulated managers need an audit trail. The Audit Trail card on alphactor.ai records every trade, rebalance, alert, and note into one timestamped log you…

Portfolio Optimizer: From Holdings to an Efficient Frontier

Naive mean-variance overweights recent winners. Running MVO, risk parity, and Black-Litterman in parallel shows which allocation choices are robust vs. fragile.

Sector Allocation: How Much Tech Is Too Much?

Sector creep is the most common risk in retail portfolios. Measuring weight vs. risk contribution and setting caps prevents a rotation from causing big losses.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free