Price-to-Earnings (P/E) Ratio

The price an investor pays per dollar of company earnings, the single most-quoted valuation metric.

`P/E = Price per share / Earnings per share`. Forward P/E uses next-year estimates; trailing uses the past 12 months. The cyclically adjusted P/E (CAPE, Shiller) smooths over 10 years of real earnings.

Why it matters. P/E is a quick, comparable snapshot of how the market is pricing a stream of earnings. But "expensive" vs "cheap" only means something relative to growth and capital intensity, a capital-light, fast-growing business legitimately earns a higher multiple than a cyclical with flat earnings.

Pitfalls. P/E breaks on negative earnings; is easily distorted by one-off items; and ignores balance-sheet leverage. Always pair with EV/EBITDA for a capital-structure-neutral view and a DCF for a first-principles anchor.

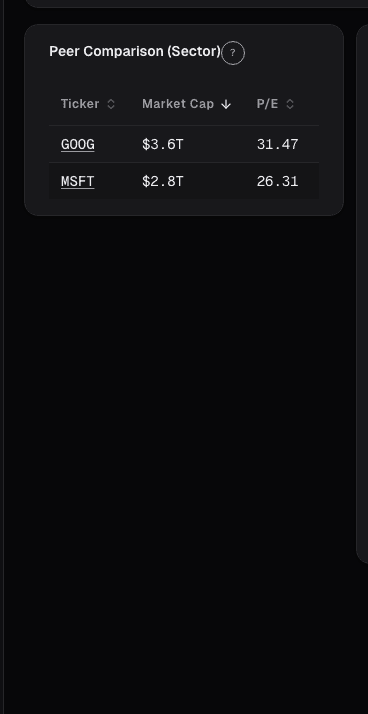

See it applied

Related reading

- EV/Revenue: The Multiple That Survives When Earnings Don't

EV/Revenue survives where P/E breaks, but needs a growth bridge. Pre-profit software mid-cycle runs 0.2-0.4x growth-adjusted, how to avoid the reading traps.

- FCF Yield: What You're Actually Earning Today

FCF yield answers the most basic question in equity investing: if I buy this company today, how much cash does it throw off per dollar?

- Earnings Power Value

EPV asks what a company is worth assuming zero growth, forever. The gap between EPV and market cap is the growth premium.