Part of: Fundamental Analysis

SEC Filings: Reading the Primary Source Directly

Every third-party analysis loses information. Diffing new SEC risk factors vs. the prior year filing is the highest-leverage research activity for any investor.

Sarah Patel7 min read

Sarah Patel7 min readIn Q4 2022 I was evaluating a mid-cap business-services company that sell-side coverage was uniformly bullish on. The thesis in every note was "durable margin expansion, pricing power, accelerating free cash flow." I pulled the 10-K for the fiscal year just filed, and specifically ran the risk-factor diff against the prior year's 10-K. The diff surfaced a new risk factor, buried on page 24, about 380 words long, which hadn't appeared in any prior filing. It discussed concentration risk in a specific customer representing 14% of revenue whose contract was up for renegotiation within 12 months. The sell-side notes had mentioned the customer in passing, always with a "durable relationship" descriptor, but none had flagged the renewal risk, and none had quoted the new risk factor. Legal counsel had put the disclosure in the 10-K because they're paranoid about under-disclosing material risks that later blow up. Eight months later the customer announced they'd taken 60% of the contract in-house at renewal; the stock gapped 19% down on the announcement, and another 8% over the following week. The risk was disclosed; almost no reader had bothered to read it. That's why reading primary filings, specifically the diff against the prior year, is the highest-leverage research activity available. It's tedious, which is why it's under-priced.

This post is about the SEC Filings card, why reading filings directly beats reading summaries, and the three practices that turn filing access into actual research leverage.

TL;DR

- Every third-party summary loses information; the primary filing is where disclosure lives.

- Newly added risk factors are disproportionately informative: lawyers don't add them casually.

- Critical-accounting-estimate changes can move reported earnings 10-20% without any operational change.

- Change-diff view is the workflow multiplier: reading every word is infeasible; diffing vs. prior year is tractable.

- AI filing summaries are a starting point, not a substitute; spot-check the highlights against the source.

Why primary filings matter

Every third-party analysis of a public company, Bloomberg, Seeking Alpha, sell-side notes, StockTwits, is a summary of SEC filings. And every summary loses information:

- Management footnotes explaining GAAP-to-non-GAAP bridges get condensed to one line

- Changes in accounting estimates with material P&L impact get buried

- New risk factors added to the 10-K get ignored because risk factors are boring until they matter

- Segment-level disclosures that reveal mix shifts get aggregated out

- MD&A (management discussion) tone gets flattened to bullet points

The reader who goes to the primary source catches the information the summaries drop. For retail investors, this is disproportionate alpha because primary-source reading is tedious, and almost nobody does it. The sell-side analysts who *do* read the filings are under pressure to fit their write-ups in a few pages, so the nuance gets cut. The primary source is the one place all of it still lives.

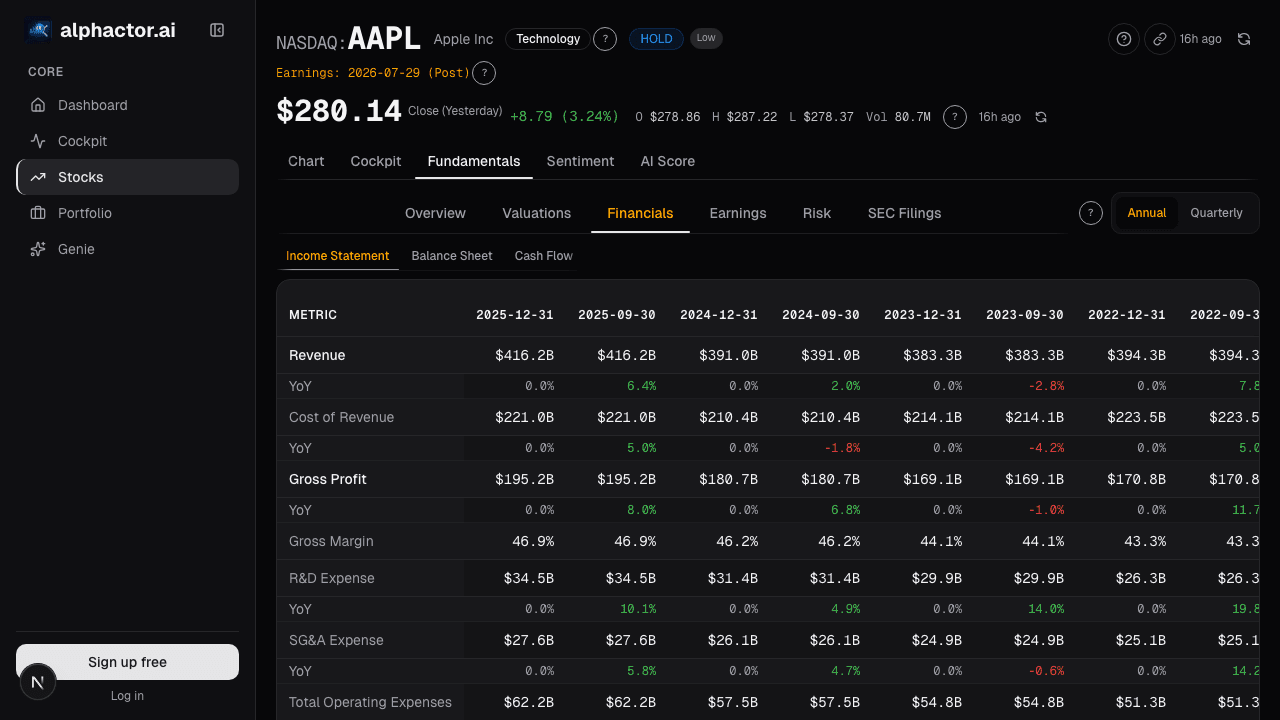

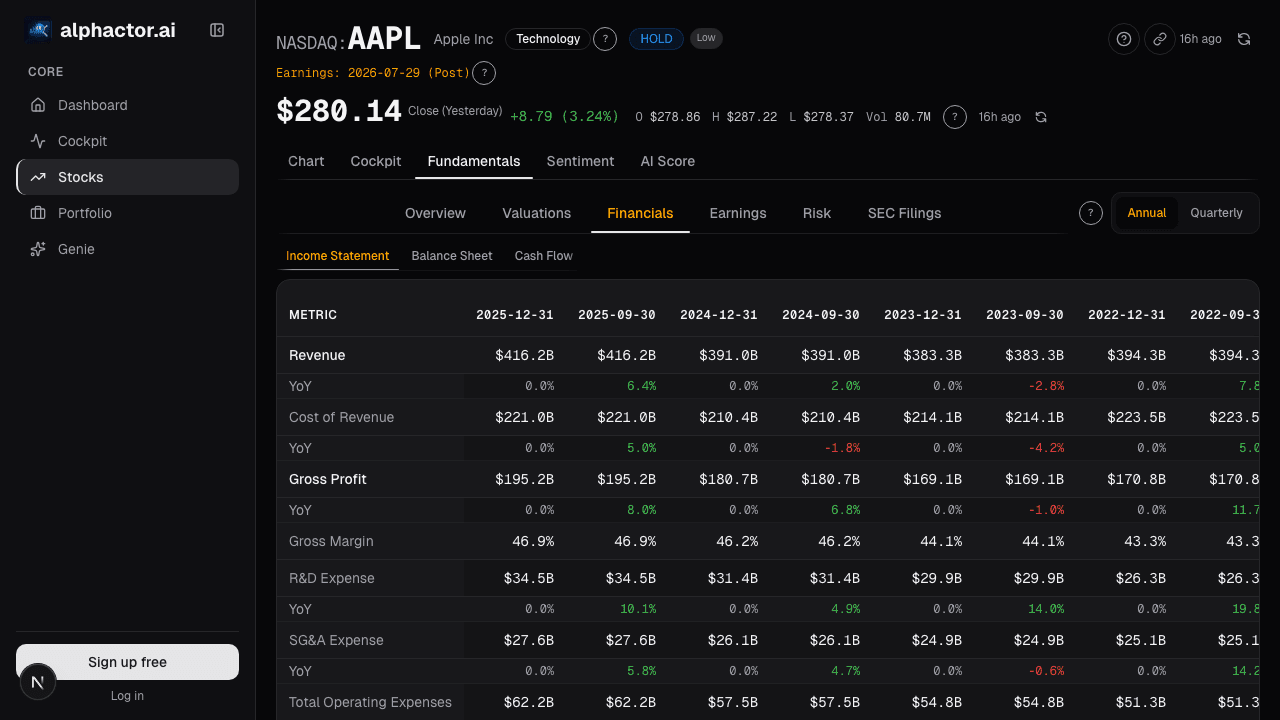

What the SEC Filings card shows

The SEC Filings card lists the last 24 months of EDGAR filings:

- 10-K (annual report), the comprehensive filing with risk factors, MD&A, full financial statements, footnotes

- 10-Q (quarterly), interim updates, less comprehensive than 10-K but with updated MD&A

- 8-K (material events), filed within 4 business days of any material event (earnings, executive departures, acquisitions, lawsuits)

- DEF 14A (proxy), annual meeting materials with executive comp and governance

- Form 4 (insider), individual insider transactions

- 13F (institutional), quarterly holdings

- 20-F (foreign private issuers), annual for ADRs

Key workflow features:

- Full-text search across the last 5 years of filings

- Change-diff view: every paragraph added, removed, or materially changed between the current 10-K/10-Q and the prior year's equivalent, highlighted side-by-side

- AI filing summary: top 5-10 material changes per filing in plain English

- Section-targeted diffing: focus diff on risk factors, MD&A, or critical accounting estimates alone

- Cross-filing references: click a disclosed acquisition in the 10-K to see the 8-K filed when it happened

Three practices that multiply research leverage

Start with the risk-factors diff on every 10-K. Newly added risk factors are disproportionately informative. They're drafted by legal counsel who is personally liable if they fail to disclose a material risk that later blows up, and legal counsel is aggressively cautious. A newly added risk factor is lawyers saying "we're worried enough about this specific thing that we need to put it on paper." The risk factors that come *off* the list are usually less informative (company eliminated a risk, or believes it's no longer material), but additions are almost always worth a careful read.

Scan the critical-accounting-estimates section on every 10-Q. Changes in inventory reserves, revenue recognition timing, bad-debt provisions, or tax provisions can move reported earnings by 10-20% without changing the underlying business at all. Critical accounting estimates are the footnotes where these changes get disclosed. Reading this section every quarter catches "quality of earnings" shifts that aren't obvious from the headline EPS number. A 5 percentage point change in the revenue-recognition assumption can be the difference between a beat and a miss.

Read the departing-executive's letter in CFO-transition 8-Ks carefully. When a CFO leaves, the 8-K usually includes a statement from the departing executive. The tone and specificity are diagnostic: routine "pursuing other opportunities" language is often noise, but explicit grievances or unusually terse statements can signal real conflict that the company is trying to manage. Cross-reference with any insider filings the departing executive makes in the following months.

Example: the risk-factor that predicted the customer loss

The new risk factor from Q4 2022, reproduced in summary:

| Section | Change |

|---|---|

| Risk factors | +1 new (customer concentration) |

| Critical accounting | No material changes |

| MD&A | Minor tone shift on outlook |

| Segment disclosure | No change |

The specific added risk factor text discussed that a single customer represented 14% of revenue, that the master service agreement was up for renewal within 12 months, that there was no guarantee of renewal at current volume or price, and that loss of the customer could materially impact revenue and profitability. The language was detailed and specific, not boilerplate. Every sell-side note I read in the following month mentioned the customer by name but treated the relationship as secure; none quoted or paraphrased the new risk factor. Eight months later the renewal result played out exactly as the risk factor had warned. The disclosure had been hiding in plain sight for three-quarters of a year.

What the card can miss

- Off-balance-sheet arrangements. Some exposures (SPVs, operating leases pre-ASC 842) appear only in obscure footnotes or not at all.

- Unrecorded contingencies. Pending litigation that hasn't been accrued may be mentioned but not quantified.

- Non-public management color. Filings are public documents; earnings-call color, management access, and private conversations aren't in them.

- Competitive context. Filings disclose the company's view; competitors' filings are separate and often illuminate the same situation differently.

- Footnote reference webs. One paragraph may reference three other footnotes; following the web manually is tedious even with good search.

Common mistakes

- Reading only the AI summary. The summary is a starting point; the value is in the source.

- Skipping risk factors because they look boilerplate. Most are boilerplate; new ones are not.

- Ignoring 10-Q updates. 10-Ks are deeper, but 10-Qs are where mid-year changes first surface.

- Not diffing. Reading every word of a 10-K is infeasible; diffing against prior year is the feasible workflow.

- Relying on filings alone. Filings plus earnings calls plus management access is the complete picture.

Where it fits

SEC Filings is the primary-source backbone of the fundamentals page. Pair with Accruals Quality for the earnings-quality read on what's in those filings, Insider Transactions for the Form 4 side, and Institutional Holders for the 13F side.

FAQ

How fresh is the data?

Filings appear in the card within hours of SEC submission. EDGAR is the authoritative source; the card mirrors it.

Does the diff cover every filing type?

10-K and 10-Q specifically. 8-Ks are event-specific and don't have a meaningful diff; proxies have optional diffing against prior-year proxy.

How accurate is the AI summary?

Generally good on big-picture changes; can miss subtle legal-language shifts. Spot-check against the source for material conclusions.

Can I subscribe to filings for a ticker?

Yes, filing alerts notify on new 10-K/10-Q/8-K/DEF 14A within minutes of filing.

What about foreign filers?

20-F is the foreign-equivalent 10-K; the card supports it with similar diff capability.

Related reading

- Accruals Quality, Earnings Manipulation

- Altman Z, Bankruptcy Risk

- Balance Sheet Capital Structure

- Cashflow Waterfall, Operating to Free

Open the SEC Filings card → /app/stocks/AAPL/fundamentals

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Accruals Quality: How to Spot Earnings That Aren't Real

Accruals measure the gap between reported earnings and actual cash. Widening accruals is one of the most reliable red flags in financial analysis, Sloan's…

Altman Z-Score: A Bankruptcy Predictor That Still Works

Edward Altman's 1968 discriminant model predicts bankruptcy within two years about 72% of the time at its distress threshold.

Balance Sheet Deep Dive

Balance sheet changes lead income statements by 2-6 quarters. Net debt, receivables days, and goodwill are the lines that move stocks first.

Price-to-Book Value: Useful for Banks, Misleading for Tech

Price-to-book works for banks and asset-heavy industrials but misleads for software. Here is how to apply it correctly by sector and when to skip it.

Cashflow Waterfall: From Operating Cash to Free Cash

Operating cash flow is cleaner than net income but still not distributable cash. The waterfall makes every deduction visible, SBC, working capital, capex …

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free