Part of: Fundamental Analysis

Not All Revenue Growth Is Created Equal

Why the source and sustainability of revenue growth matters more than the headline number, and how to distinguish organic growth from accounting illusions.

Sarah Patel4 min read

Sarah Patel4 min readThe Headline Number Lies

A company reports 25% revenue growth. The stock rallies. Analysts upgrade their price targets. But buried in the footnotes, you discover that 20% of the growth came from a single acquisition completed six months ago. Strip that out, and organic growth was 5%.

This happens constantly. Revenue growth is the most celebrated metric in growth investing, and it is also one of the most easily inflated. Not all growth is created equal, and treating it as a monolithic number is one of the most common analytical mistakes in equity research.

Organic vs. Acquired Growth

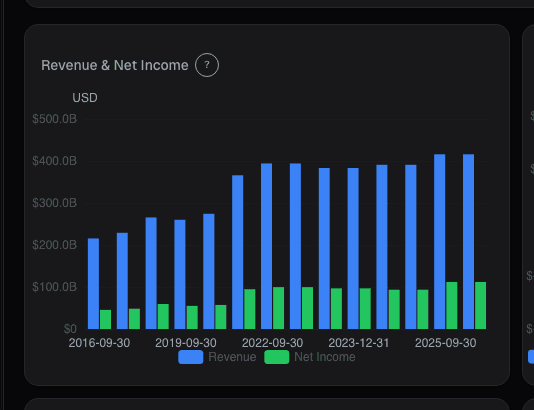

The first and most important distinction is between organic growth (generated internally through more customers, higher prices, or new products) and acquired growth (added by purchasing other companies).

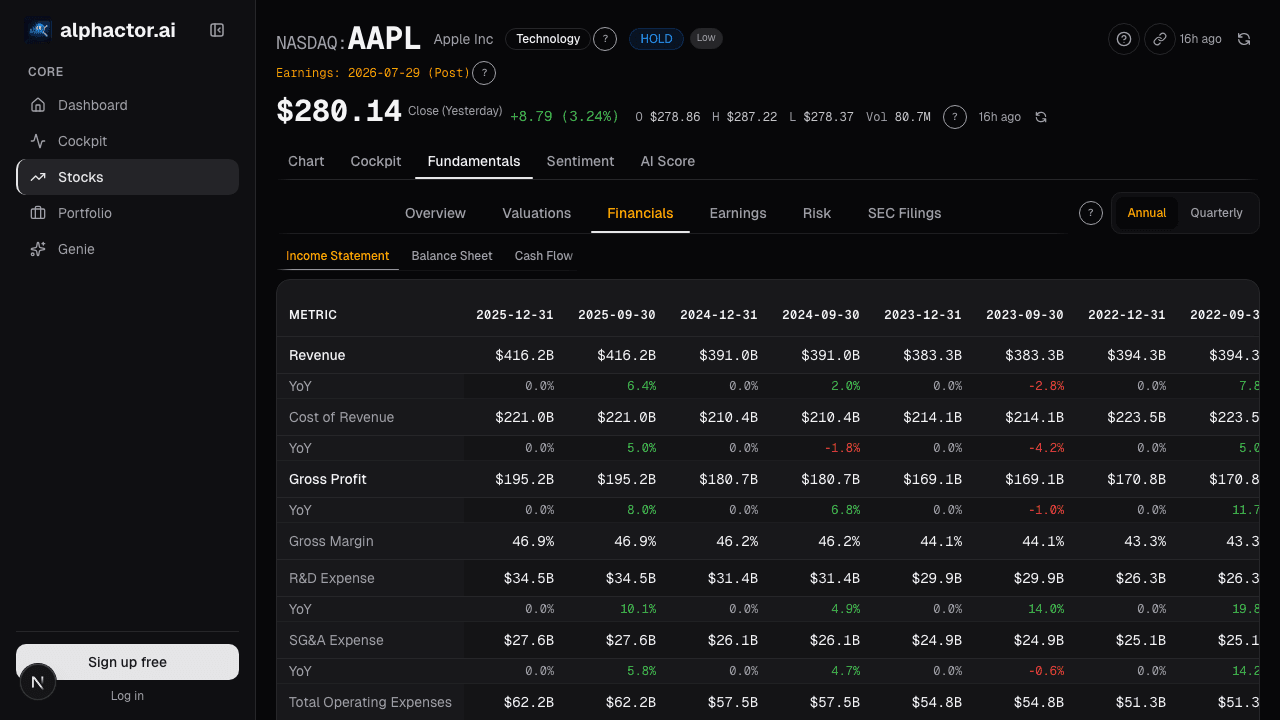

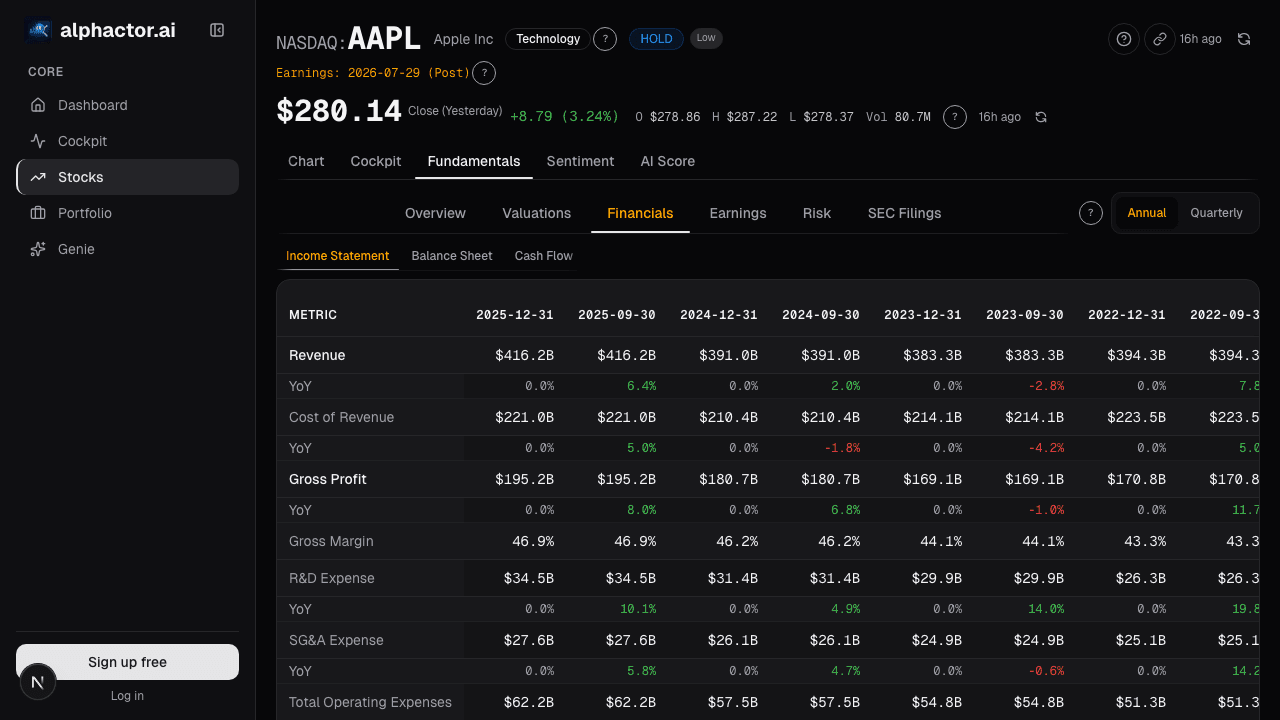

Organic growth is almost always more valuable because it demonstrates that the existing business is gaining traction. It typically comes at higher margins since there are no integration costs, goodwill premiums, or restructuring charges. Companies that consistently grow organically at 8-12% are rare and deserve premium valuations.

Acquired growth tells a different story. It can create value when the acquirer pays a reasonable price and achieves genuine synergies. But empirical research consistently shows that most acquisitions destroy shareholder value. The acquiring company pays a premium, takes on integration risk, and often overstates synergy projections. Verizon's $4.4 billion write-down on its Yahoo acquisition and AT&T's reversal of the Time Warner deal are cautionary examples at scale.

When evaluating revenue growth, always check whether the company completed acquisitions during the period. Alphactor's fundamentals view tracks organic growth rates where data is available, giving you a cleaner view of underlying momentum.

Pricing vs. Volume

Revenue growth also decomposes into price and volume. A company growing revenue 10% because it raised prices 10% on a flat customer base is in a fundamentally different position than one growing 10% by adding customers at stable prices.

Pricing-driven growth is powerful in the short term because it drops straight to the bottom line with no incremental costs. But it has limits. Customers eventually push back, competitors undercut, or regulators intervene. Netflix's price increases worked for years, but subscriber growth eventually stalled in mature markets as competitors proliferated.

Volume-driven growth is more sustainable but often comes with higher costs, since serving more customers requires more infrastructure, employees, or inventory. The best businesses achieve both simultaneously: growing the customer base while also increasing revenue per customer through upselling, cross-selling, or natural price escalation.

Recurring vs. One-Time Revenue

A dollar of recurring subscription revenue is worth far more than a dollar of one-time transactional revenue. The SaaS industry figured this out years ago, which is why investors pay 15-25x revenue for subscription software businesses and 1-3x revenue for project-based services firms.

Recurring revenue provides visibility. A company entering a quarter with 90% of its revenue already locked in through existing contracts can plan, invest, and forecast with confidence. A company that starts each quarter from zero and must win every deal fresh faces a completely different risk profile.

When evaluating revenue growth, look at the mix. Is the growing revenue recurring or one-time? What is the net revenue retention rate, the percentage of revenue retained from existing customers year over year? Best-in-class SaaS companies like Snowflake and CrowdStrike have historically posted net retention rates above 120%, meaning existing customers spend 20% more each year before any new customer acquisition.

Geographic and Customer Concentration

Twenty percent revenue growth driven by a single large contract is riskier than 15% growth spread across thousands of customers. Customer concentration creates fragility: losing one major account can wipe out years of progress.

Similarly, growth concentrated in a single geography may face currency risk, regulatory changes, or market saturation. Companies expanding into new regions while maintaining growth in existing markets are building more durable franchises.

The Quality Checklist

When a company reports strong revenue growth, run through these questions before getting excited:

Is it organic? Strip out acquisitions and currency effects to find the core growth rate.

Is it profitable? Revenue growth that comes with expanding losses may be buying customers at unsustainable prices. Check if gross margins are stable or improving alongside the growth.

Is it recurring? Higher recurring revenue mix means more predictable future performance and higher business quality.

Is it diversified? Growth spread across customers, products, and geographies is more durable than growth concentrated in one area.

Is it decelerating? The rate of change matters. A company growing 30% that is now growing 20% might still look strong in absolute terms, but the deceleration trend often continues.

Alphactor's fundamentals view displays revenue growth alongside margin trends and customer metrics where available, making it easier to assess growth quality rather than just growth quantity. The stock comparison feature helps contextualize whether a company's growth rate is leading or lagging its industry.

The market eventually prices growth correctly. Unsustainable growth gets repriced lower, sometimes violently. Sustainable organic growth gets rewarded over time. Learning to tell the difference early is one of the highest-value skills in stock analysis.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Accruals Quality: How to Spot Earnings That Aren't Real

Accruals measure the gap between reported earnings and actual cash. Widening accruals is one of the most reliable red flags in financial analysis, Sloan's…

Altman Z-Score: A Bankruptcy Predictor That Still Works

Edward Altman's 1968 discriminant model predicts bankruptcy within two years about 72% of the time at its distress threshold.

Government Contracts

Federal obligations are public within days via USAspending and typically flow to the issuer 2–4 quarters before appearing in a 10-Q.

PEG Ratio: A Growth-Adjusted P/E, Less Naive Than It Looks

Naive PEG ignores growth quality and buyback distortions. The fix: use 3-5 year organic EPS CAGR and compare only within a profit-consistent peer group.

Price-to-Sales for Growth Stocks

How to use price-to-sales ratio to value high-growth companies that are not yet profitable, and the traps that make this metric dangerous.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free