Part of: Risk Management

A 30% Drawdown Requires a 43% Gain to Recover

A 30% drawdown requires a 43% gain to recover. The asymmetric math explained, with sizing rules to prevent one bad trade from permanently impairing the account.

Marcus Chen4 min read

Marcus Chen4 min readThe Math Nobody Wants to Hear

Losses and gains are not symmetrical. A 10% loss requires an 11.1% gain to break even. That seems manageable. But the relationship is exponential, not linear, and it gets ugly fast.

Here is the table that should be taped to every trader's monitor:

- 10% loss requires 11.1% gain to recover

- 20% loss requires 25% gain to recover

- 30% loss requires 42.9% gain to recover

- 40% loss requires 66.7% gain to recover

- 50% loss requires 100% gain to recover

- 60% loss requires 150% gain to recover

- 75% loss requires 300% gain to recover

That last one is not theoretical. Cathie Wood's ARKK fund dropped roughly 75% from its February 2021 peak. To get back to its all-time high, it would need to quadruple from those lows. Years later, investors are still waiting.

Why This Breaks People

The math is bad enough. The psychology makes it worse.

When you are sitting on a 30% drawdown, you need a 43% gain just to get back to where you started. Not to profit. Just to get to zero. That changes how you think, and rarely for the better.

Most people respond to deep drawdowns in one of three ways:

Paralysis. You stop opening your brokerage app. Positions drift. Stop losses you meant to set never get placed. The drawdown deepens because you cannot face it. I watched a fund analyst in 2018 refuse to update his P&L spreadsheet for six weeks because he "already knew it was bad." By the time he looked, a 15% drawdown had become 28%.

Desperation. You start swinging for the fences. If you need 43% to recover, suddenly that speculative biotech with a binary catalyst looks like the only way back. You concentrate into your highest-risk ideas precisely when you can least afford more risk. This is revenge trading's more calculated cousin, and it is just as lethal.

Capitulation. You sell everything at the bottom because the pain of further loss outweighs the possibility of recovery. This is what professionals call "selling the hole," and it is the single most expensive mistake retail investors make. During March 2020, retail investors pulled $326 billion from equity funds right before one of the fastest recoveries in market history.

The Real Cost Is Time

Even if you have the skill to generate above-average returns, the time cost of recovery from deep drawdowns is brutal.

Assume you are a good trader generating 15% annualized returns, which puts you well above average. After a 50% drawdown, you need a 100% gain to recover. At 15% annual returns, that takes roughly five years. Five years of solid performance just to get back to where you were on one bad afternoon in March.

This is why hedge funds obsess over drawdown metrics. The Sharpe ratio tells you about risk-adjusted returns. Maximum drawdown tells you how close you came to dying. Investors who lived through 2008 care far more about the second number.

Prevention Beats Recovery Every Time

The implication of asymmetric drawdown math is straightforward: preventing large losses matters more than capturing large gains. A portfolio that returns 12% annually with a maximum drawdown of 15% will massively outperform a portfolio that returns 18% annually with a maximum drawdown of 45% over any meaningful time horizon. The first portfolio compounds. The second one keeps getting knocked back to the starting line.

Practical steps to keep drawdowns survivable:

Set portfolio-level drawdown limits before you need them. Write down what happens at 10%, 15%, and 20% drawdowns. At 10%, tighten stops and stop adding new positions. At 15%, reduce exposure by a third. At 20%, go to half cash and reassess everything. Alphactor's trade alerts let you set these thresholds and get notified before you hit them, which matters because you will not be thinking clearly when the number is red.

Size positions so a total wipeout in any one stock cannot create a portfolio-level crisis. If your maximum position is 5%, even a total loss in that stock only creates a 5% portfolio drawdown. Recoverable. Manageable. Not fun, but not fatal.

Diversify across drivers, not just tickers. Five tech stocks is one bet, not five. If all your positions respond to the same macro factor, a drawdown in one is a drawdown in all.

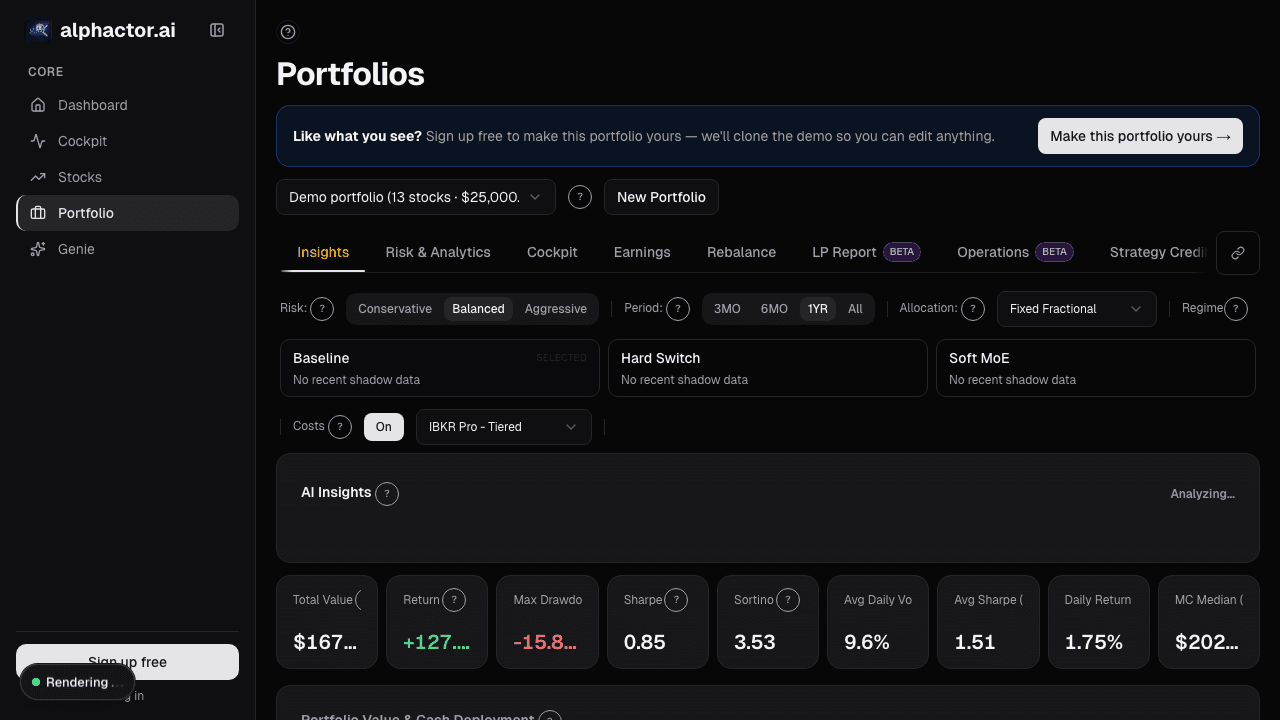

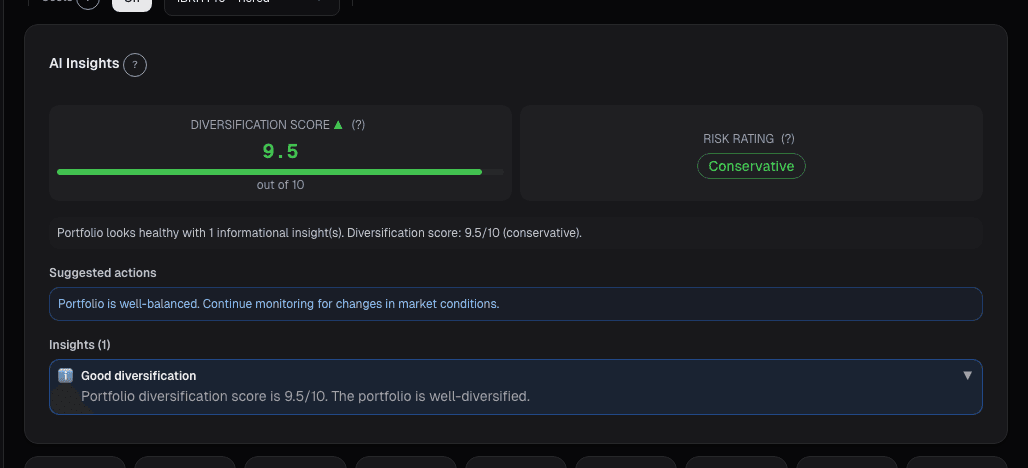

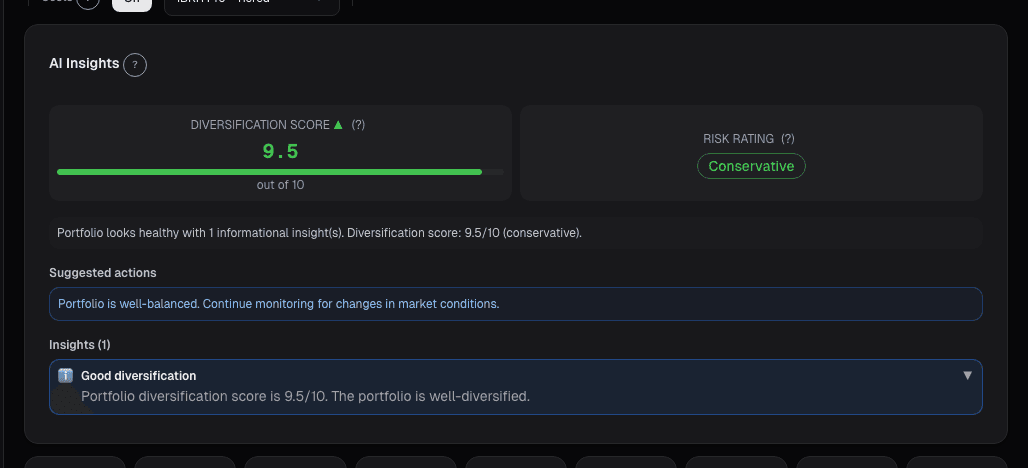

Track your rolling maximum drawdown, not just your returns. Returns tell you what you made. Maximum drawdown tells you what you almost lost. The second number is more predictive of whether you will survive the next decade of markets. Your portfolio dashboard shows rolling drawdown alongside returns so both numbers stay visible.

The Point

Drawdown math is not fair. A 50% loss and a 50% gain are not the same thing, and treating them as equivalent is one of the most expensive cognitive errors in investing. The traders who last are not the ones who hit the biggest winners. They are the ones who never dig a hole so deep that even years of good performance cannot climb out of it.

Build your system around not losing big. The gains will take care of themselves.

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Related reading

Knowing Your Emotional Triggers Isn't Soft: It's Edge

Emotional self-awareness is not a personality exercise. It is a concrete trading advantage that reduces costly mistakes and protects capital.

Why Maximum Drawdown Is More Important Than Annual Return

Maximum drawdown reveals what your portfolio almost did to you. Here is why it matters more than the number everyone brags about.

Portfolio Earnings: Calendar, Exposure

Earnings risk is about the whole book into the week, not each position. When 40% of NAV reports in one week, and 60% of that is in a single sector, you're…

Factor Exposure

Factor exposures are bets whether or not you chose them. Decomposition surfaces unintentional tilts before a rotation exposes them as underperformance.

Revenge Trading: How One Bad Day Becomes a Bad Month

Revenge trading is the single fastest way to turn a manageable loss into a catastrophic one. Here is how it works and how to break the cycle.

Keeping a Trading Journal

A trading journal is the cheapest, most effective tool for improving performance. Here is what to track, how to review it, and why most people quit too soon.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free