Part of: Risk Management

The 5 Position Sizing Mistakes That Blow Up Accounts

Position sizing errors kill more accounts than bad stock picks. Here are the five most common mistakes and how to avoid each one.

Marcus Chen4 min read

Marcus Chen4 min readWhy Sizing Kills More Accounts Than Picking

You can be wrong on the stock and survive. You cannot be wrong on the size and survive. A 3% position that drops 50% costs you 1.5% of your portfolio. Painful, not fatal. A 25% position that drops 50% costs you 12.5%. That is the kind of hole most people never climb out of.

In ten years of watching portfolios implode, the cause was almost never "they picked the wrong stock." It was almost always "they put too much in the wrong stock." The five mistakes below account for the vast majority of sizing-related blowups I have seen.

Mistake 1: Equal Weighting Everything

The logic sounds reasonable: if you do not know which stocks will outperform, give them all the same weight. Buy ten stocks, put 10% in each. Simple and fair.

The problem is that equal weighting ignores the fact that different stocks carry radically different levels of risk. A 10% position in a utility company with a beta of 0.6 and 12% annual volatility is a completely different bet than a 10% position in a pre-revenue biotech with 80% annual volatility. The second position contributes roughly six times more risk to your portfolio than the first, despite the identical dollar allocation.

Equal weighting is not neutral. It overweights risk in your most volatile positions. Risk-weight instead: higher-volatility stocks get smaller allocations so each position contributes roughly the same amount of risk. You can use Alphactor backtesting to compare how equal-weighted versus volatility-adjusted portfolios performed historically.

Mistake 2: Sizing Up After Wins

This one is insidious because it feels like confidence. You have had three winners in a row. Your account is up 15% this quarter. You feel sharp. So you increase your position sizes because you have "earned" the right to take more risk.

This is how drawdowns become catastrophic. The wins that made you confident were partly skill and partly luck, and you cannot tell which is which in real time. If your next trade was always going to lose, the only question is how much, and you just made the answer "a lot."

Professional risk managers do the opposite. When the P&L is running hot, they look for reasons to reduce size, because elevated confidence correlates with elevated risk-taking. Keep position sizes consistent with your rules regardless of recent performance.

Mistake 3: Ignoring Correlation When Sizing

You carefully limit each position to 4% of your portfolio. You hold 12 stocks. No single name can hurt you. Except five of those stocks are cloud software companies that trade in lockstep. Your "12 positions at 4% each" is really "one 20% bet on cloud software and 7 other positions."

Individual position limits are necessary but insufficient. You must also size for correlated exposure. If three positions have a 0.8 correlation with each other, their combined risk is closer to one large position than three independent ones.

The practical fix: after sizing individual positions, add up the exposure in each correlated cluster. If the combined weight of highly correlated positions exceeds what you would put in a single name, trim until it does not. Stock comparison lets you see how correlated clusters behave under adverse scenarios, showing you the true risk of your concentrated exposures before the market reveals it the hard way.

Mistake 4: Averaging Down Without a Plan

Averaging down, buying more of a losing position to lower your average cost, is not inherently wrong. Some of the best investors do it. The difference is that they plan it in advance and cap the total exposure.

The mistake is unplanned averaging down, where you keep adding because you "believe in the thesis" and the lower price looks attractive. By the third or fourth add, what started as a 3% position is now 10%, your thesis may be wrong, and you are too deep to think clearly.

If you average down, decide before the first purchase how many times you will add, at what intervals, and what the maximum total position will be. A common framework: plan for three tranches. Initial position at 2%. First add at 2% if the stock drops 15% and the thesis is intact. Second add at 1.5% if it drops another 15%. Maximum total: 5.5%. If it drops further, no more adds. No exceptions.

Mistake 5: No Position Size Limit at All

This is the most basic mistake and the most deadly. You find a stock you love. The fundamentals are perfect, the valuation is compelling, the catalyst is clear. So you put 30% of your portfolio in it. Maybe 40%. You have "high conviction."

High conviction and correct are not the same thing. Bill Ackman had extremely high conviction in Valeant Pharmaceuticals. He was one of the smartest investors in the world, with a research team that spent thousands of hours on the thesis. His concentrated position lost roughly $4 billion.

The point is not that conviction is wrong. The point is that the relationship between conviction and correctness is weaker than it feels. You should never, under any circumstances, put so much in a single position that being wrong on that one name threatens your ability to continue investing. For most retail investors, that means a hard cap of 5-7% per position, regardless of conviction level.

The Common Thread

All five mistakes share a root cause: letting the expected outcome of a trade determine its size, instead of letting the worst-case outcome determine its size. Size for what happens when you are wrong. The winners take care of themselves.

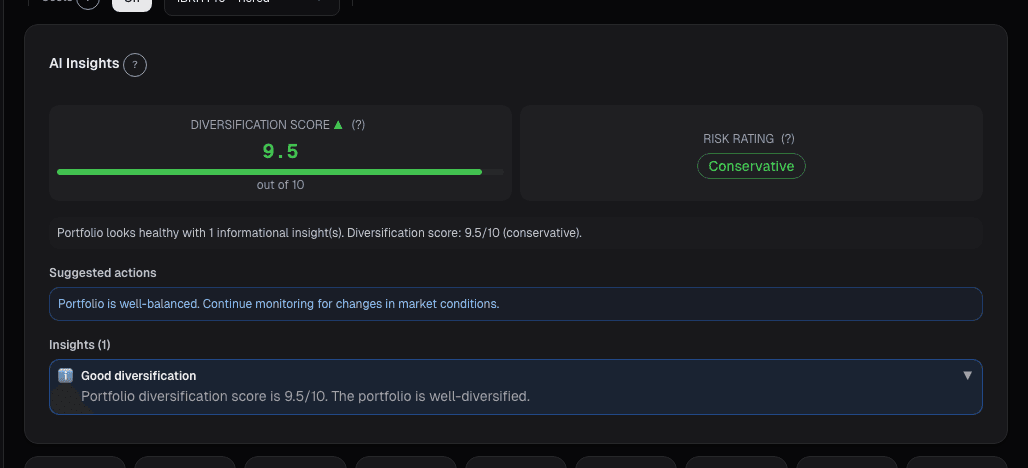

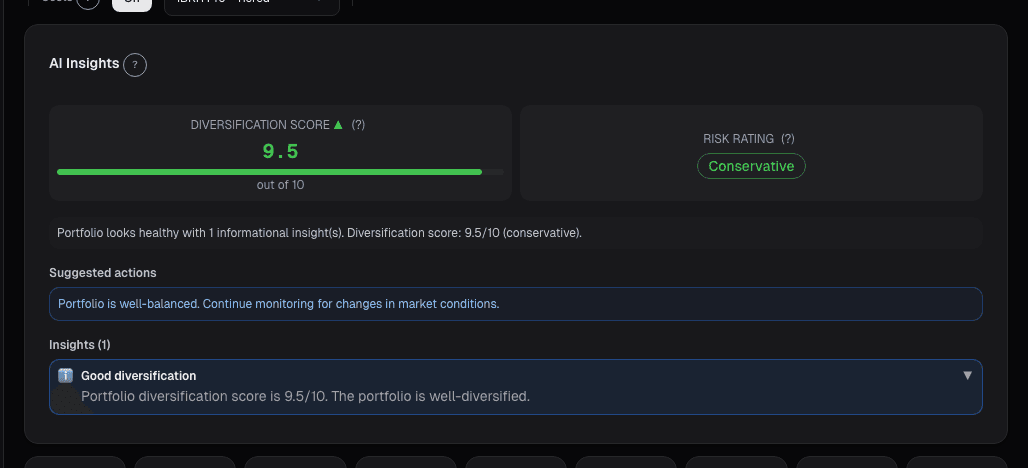

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

ATR for Position Sizing

How Average True Range normalizes risk across stocks, sets intelligent stop losses, and determines position size based on volatility, not gut feeling.

Half-Kelly Position Sizing

Half-Kelly gives about three-quarters of full Kelly growth while cutting drawdown by roughly 50%, making a theoretically optimal bet practically executable.

Portfolio Earnings: Calendar, Exposure

Earnings risk is about the whole book into the week, not each position. When 40% of NAV reports in one week, and 60% of that is in a single sector, you're…

Factor Exposure

Factor exposures are bets whether or not you chose them. Decomposition surfaces unintentional tilts before a rotation exposes them as underperformance.

FX Exposure: The Currency Risk Hiding in Your USD Portfolio

You bought US stocks in dollars, so you have no FX risk, right? Wrong. US large-cap multinationals earn 40-60% of revenue abroad.

A Position Sizing Framework That Won't Keep You Up at Night

A practical position sizing approach built on simplified Kelly criterion, risk-per-trade limits, and portfolio-level allocation guardrails.

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free