Part of: Risk Management

Risk Management for Retail Portfolios

Practical position sizing, stop-loss strategies, correlation awareness, and drawdown limits for retail investors managing their own money.

Marcus Chen4 min read

Marcus Chen4 min readRisk Management Is Not Optional

Most retail investors spend 90% of their time on stock selection and 10% on risk management. Professional fund managers invert that ratio. Even a portfolio of excellent stock picks can get destroyed by poor risk management. One outsized position that drops 60% can wipe out years of steady gains.

Risk management is not about avoiding losses. It is about ensuring no single loss, or correlated set of losses, can permanently impair your ability to keep investing.

Position Sizing: The First Line of Defense

The single most impactful risk decision you make is how much of your portfolio to put in any one stock. There is no universally correct answer, but there are guardrails that have held up across decades of market data.

The 5% rule. No single position should exceed 5% of your portfolio at cost. For a $100,000 portfolio, that means no individual stock gets more than $5,000 of new capital. If a position grows beyond 5% through appreciation, that is different, but adding fresh capital above 5% is asking for trouble.

The 20% sector cap. Even if each individual position is sized at 3-4%, holding eight tech stocks still means 25-30% of your portfolio moves with the same macro factors. Cap sector exposure at 20% to avoid hidden concentration.

Scale with conviction. Not every idea deserves equal capital. A stock where you have deep fundamental research, a clear catalyst, and favorable valuation might warrant 4-5%. A speculative position where you are still building your thesis should be 1-2%. Alphactor's conviction scoring can help calibrate this: a higher conviction score reflects stronger alignment across multiple signals, which supports a larger allocation.

Stop Losses: When and How

Stop losses are controversial. Critics argue they get triggered by normal volatility and lock in losses right before a recovery. They have a point. But the alternative, holding a losing position indefinitely with no exit plan, is worse.

A practical approach:

Use trailing stops for momentum positions. If you bought a stock for its uptrend, a 15-20% trailing stop protects gains while giving the position room to breathe. The trailing stop rises as the stock rises and only triggers on a meaningful reversal.

Use fundamental stops for value positions. If you bought a stock because it traded at 12x earnings with strong free cash flow, your stop is a thesis violation, not a price level: earnings deteriorate, free cash flow turns negative, management changes strategy. Check quarterly, not daily.

Accept that some stops will be wrong. A stock that hits your stop and then recovers is the cost of insurance. Over a career, the positions where stops save you from a 50%+ decline more than compensate for the false triggers.

Correlation: The Hidden Risk

Diversification only works if your positions actually move independently. Owning 15 stocks that all react the same way to interest rate changes is not diversification; it is a leveraged bet on rates.

Common hidden correlations to watch for:

- Rate sensitivity. REITs, utilities, high-growth tech, and homebuilders all react strongly to interest rate expectations. Owning all four amplifies rate risk rather than hedging it.

- Commodity exposure. An airline and a chemical company both depend on oil prices. Unrelated businesses, correlated cost structures.

- Customer concentration. If three holdings derive significant revenue from the same customer (Apple, the U.S. government), you have supply chain correlation.

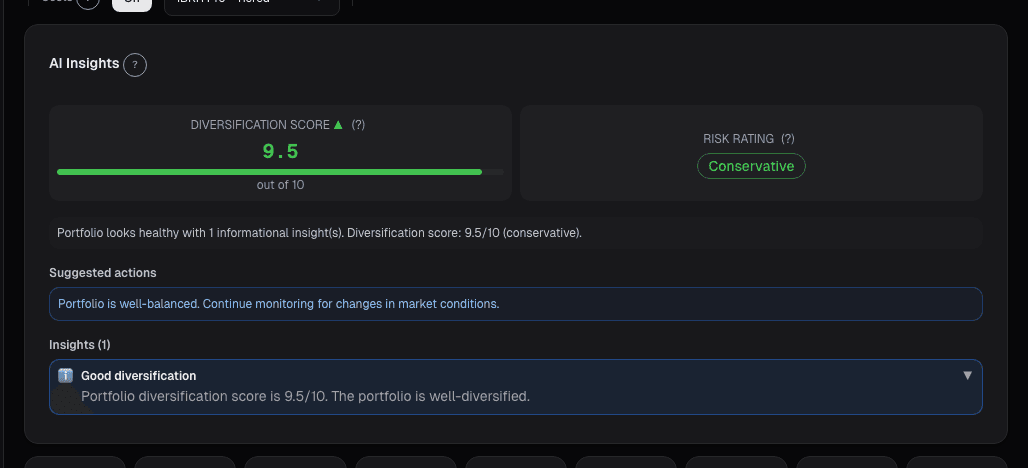

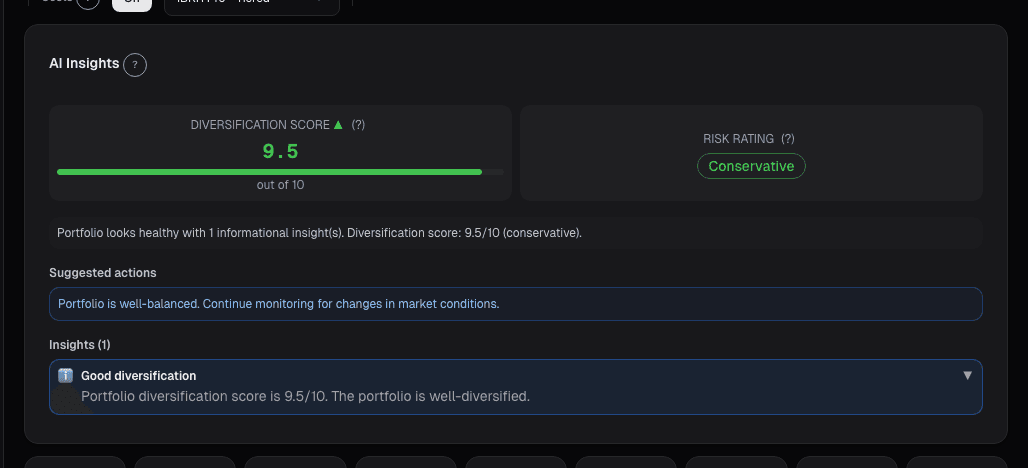

Check your portfolio's actual correlation on the portfolio dashboard, not just its sector labels.

Drawdown Limits: Knowing When to Step Back

A drawdown limit is a pre-committed rule: if your portfolio declines by X% from its peak, you reduce exposure. This is not about predicting the market. It is about protecting your capital and your psychology.

A reasonable framework for retail portfolios:

- 10% drawdown: Review all positions. Tighten stops. No new buys unless they replace existing positions.

- 15% drawdown: Reduce overall equity exposure by 20-30%. Raise cash. Shift to highest-conviction positions only.

- 20% drawdown: Move to 50% cash. Reassess your thesis on every remaining position.

These numbers are not sacred. Adjust them to your risk tolerance and time horizon. But write them down before you need them. Making drawdown rules while the market is falling is like writing a fire escape plan while the building is burning.

Putting It Together

Risk management is a system, not a single tool. Position sizing controls the maximum damage from any one mistake. Stop losses (price-based or fundamental) enforce discipline on exits. Correlation analysis prevents hidden concentration. Drawdown limits protect against systemic losses.

None of this is exciting. Nobody brags about their position sizing at a dinner party. But the investors who compound wealth over decades are almost always the ones who took risk management seriously from the start.

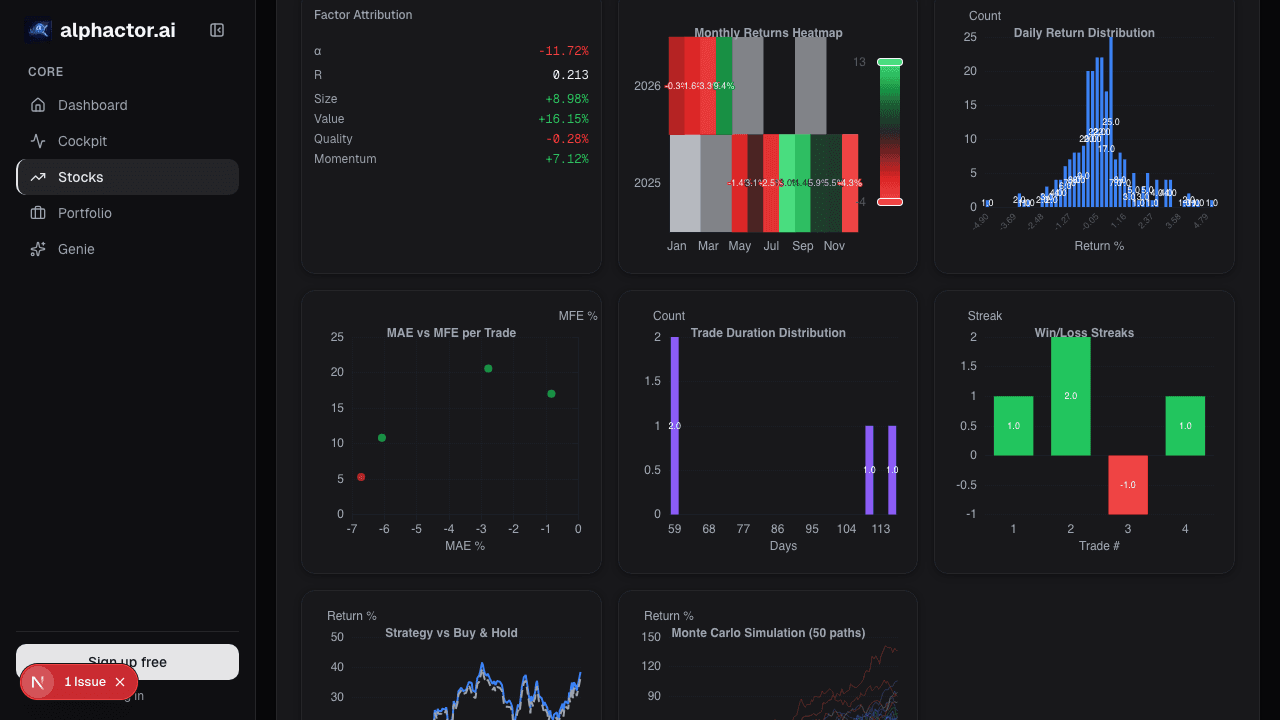

See it in the app

Live dashboard views that match this post. Each tile deep-links to the exact card.

Stocks mentioned

Related reading

Divergence Trading: The Signal That Saved My Account

How RSI divergence helped me catch a major market top, plus a practical guide to regular and hidden divergences with confirmation techniques.

Dual Momentum: Beating Buy-and-Hold for 40 Years

Gary Antonacci's dual momentum strategy combines absolute and relative momentum to deliver equity-like returns with bond-like drawdowns. Here are the numbers.

Factor Investing in Plain English

Value, momentum, quality, size, and volatility: the five major investment factors explained without jargon, with practical applications for retail portfolios.

Market Regimes: Why One Strategy Can't Do Both

How to identify market regimes using volatility, breadth, and trend data, and why adapting your strategy to the current environment separates consistent…

Sector Rotation Using Momentum: A Rules-Based Approach

A systematic sector rotation strategy using relative momentum on the 11 SPDR sector ETFs, with backtest results and walk-forward validation from 2000 to 2024.

Pairs Trading for Retail Investors: Simpler Than You Think

A practical guide to pairs trading using cointegration, with a worked example on XOM/CVX and backtest results showing how market-neutral strategies reduce…

Ready to try alphactor.ai?

Validate your trading strategies with statistical credibility testing. Start free.

Get Started Free